When Beyond Meat (BYND +3.48%) had its initial public offering (IPO) in May 2019, it was the best-performing IPO by a major U.S. company in nearly two decades, with the stock surging 163% from $25 to $65.75 on its first day. The stock went on to reach nearly $235 in July 2019, but now it's down over 99%.

Beyond Meat's rise and fall is one of the more dramatic ones we've seen in quite some time, but does that mean all hope is lost? Well, let's see.

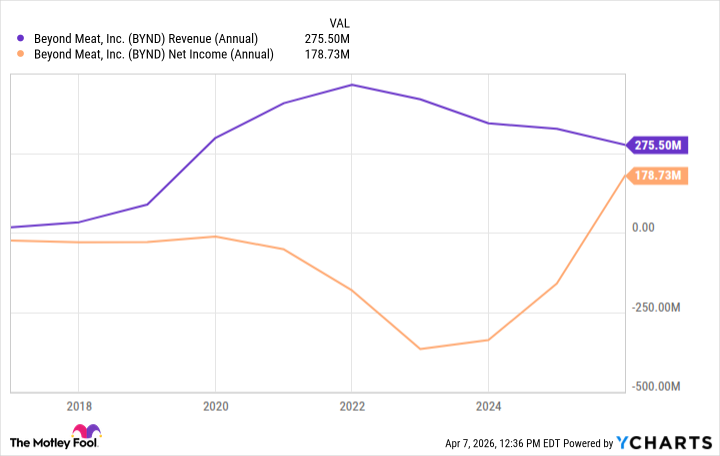

Image source: The Motley Fool.

A strategic debt restructuring

In 2025, Beyond Meat made $275.5 million in revenue, down 15.6% from 2024. This decline isn't ideal, but the most noteworthy part of Beyond Meat's earnings report was its net income.

Beyond Meat's net income was $219.9 million, a much better figure than the $160.3 million it lost in 2024. The problem, though, is when you look deeper and see how this turnaround happened. It's because Beyond Meat restructured its debt in a way that added a $548.7 million net income gain.

Without this debt restructuring, it would have reported a $328.8 million loss. The true loss attributed to shareholders for the year was $178.8 million.

BYND Revenue (Annual) data by YCharts

Buying itself some time

Beyond Meat made this move to keep its doors open. It had a debt bill of over $1.1 billion approaching in 2027, which it doesn't have the money to pay. Without the restructuring, bankruptcy was seemingly inevitable. Now, the company has until 2030 to square away the debt.

This restructuring comes at a cost, though. The new debt has a 7% interest rate, and Beyond Meat issued around 316 million new shares to the debtholders. The former means delaying the debt makes it more expensive; the latter means current shareholders' shares become more diluted and less valuable.

NASDAQ: BYND

Key Data Points

Can Beyond Meat recover?

While plant-based meat had a lot of momentum when it first became popular, many consumers have since jumped ship, and Beyond Meat simply isn't selling as much product as it used to. In its most recent quarter, the company's product volume dropped by 22.4%, continuing an unfortunate trend.

If Beyond Meat has any chance of changing the trajectory of its company, it's going to have to hope that its new protein drinks (Beyond Immerse) somehow become a cultural hit and consumers change their minds on plant-based meat. And considering the short runway Beyond Meat has, it needs to happen fast.

It bought itself some more time with its debt restructuring, but that could be delaying the inevitable. Buying the stock now is way more of a gamble than an actual investment.