If you like discounted stocks, there's a good chance Adobe (ADBE +1.82%) has caught your eye. Shares of the software company are down more than 60% from their early 2024 peak, dragging their trailing-12-month price-to-earnings ratio down to just under 14. That's as cheap as the stock's been since 2009, amid the economic turbulence stemming from the subprime mortgage meltdown.

Cheap stocks, however, aren't necessarily stocks worth buying; as the old cliché reminds us, cheap stocks are cheap for a reason. And this raises the question: Which side of the fence is Adobe on?

All the rage...

The stock's steep run-up from 2012 through 2021 makes enough sense. That's when the company first began offering cloud-based access to a suite of business-oriented image and design apps called Creative Cloud. Shortly after that, Adobe debuted what it calls Experience Manager, giving businesses the cloud-based ability to customize an individual's experience with a website as well as gather valuable data about that customer. Both were well received.

NASDAQ: ADBE

Key Data Points

Things began changing in 2022, though. While few would have guessed it possible at the time, the late-2022 launch of ChatGPT set off an artificial intelligence (AI) arms race that's since brought a stunning number of software and visual design tools to the software space. Many of them don't require any computer-coding knowledge, either. Since they can get something similar somewhere else, often at a lower cost (if not for free), businesses often no longer need what Adobe brings to the table.

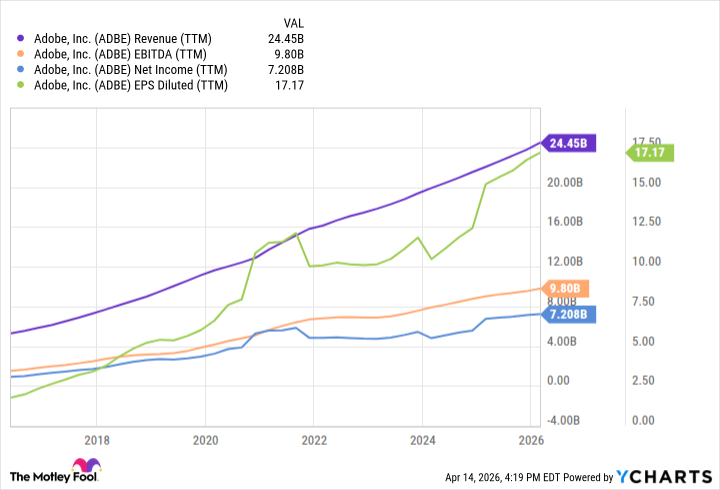

That's the presumption anyway, although the numbers don't yet confirm it. Adobe's revenue and profit growth is still proceeding at the same pace it's been moving for the past decade. Investors are waiting for -- even counting on -- the other shoe to drop. It just hasn't yet. The bearish assumption behind this stock's continued weakness, however, still holds water.

ADBE Revenue (TTM) data by YCharts

...until it wasn't

Adobe seemingly remains unfazed by the advent of affordable alternatives to its tools -- so far. Just bear in mind that many of these options are relatively new, with some kinks yet to be worked out.

A recent study done by Canada's University of Waterloo, for instance, indicates only about three-fourths of auto-generated computer code was correct as well as secure, jibing with findings from CodeRabbit last year. That's far more mistakes than human programmers tend to make. And, as AI coding gets better, these mistakes are getting tougher to find. Enterprise customers can't afford to take this degree of risk.

Image source: Getty Images.

Just take a step back and look three to five years down the road. Like any other new technology, artificial intelligence will get better. It will eventually get good enough, in fact, to provide solutions that Adobe can't compete with in terms of price as well as functionality. Maybe one or the other. But not both.

Take it at face value

So, no -- Adobe stock isn't a buy here simply because it's cheap. Although the company isn't doomed, it is one of the more vulnerable future casualties of the advent of AI. There are too many other, better opportunities out there to bother with this one.