Up less than 50% over the past five years, Amazon (AMZN -0.14%) stock has been a laggard compared to its tech giant brethren over the past few years. While the stock has gained some momentum this month, its overall performance over the past few years has been largely disappointing. However, its relatively stagnant stock price could mean that this is a once-in-a-decade bargain.

Let's look at four valuation numbers and see what they say about the stock's potential.

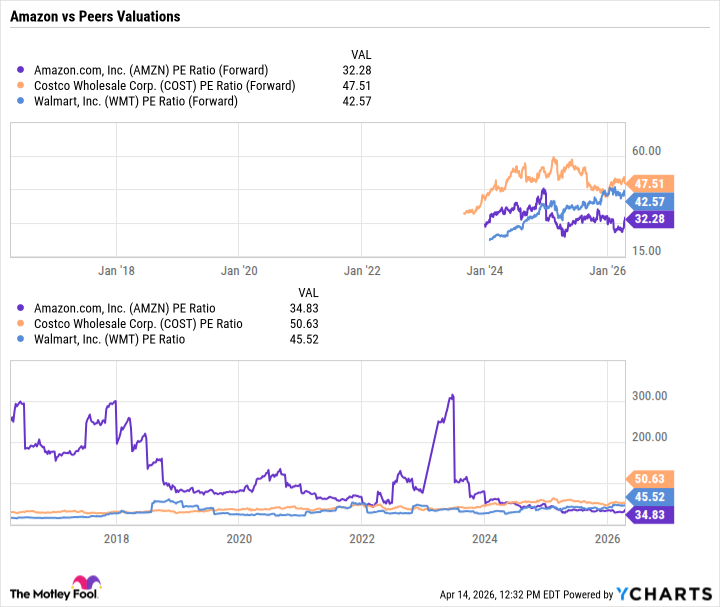

Image source: The Motley Fool.

No. 1: 32x

Amazon's current forward price-to-earnings (P/E) ratio is 32. That's well above the 24 forward P/E that it dropped to at one point last year, but it is still at a historically low level. The company's trailing P/E has also been trending lower much of the past decade and is at one of its lowest levels.

Data by YCharts.

Even more striking, though, is the valuation gap between Amazon and its brick-and-mortar peers Walmart and Costco Wholesale. Amazon had long traded at a premium in the retail space, but now it finds itself trading at a big discount, despite its retail operations still growing revenue and profits more quickly.

No. 2: 24%

Amazon Web Services (AWS) grew its revenue 24% year over year last quarter. It was the fastest pace of growth for its cloud computing segment in more than three years.

However, this is likely just the start of revenue growth acceleration for the segment. Amazon built a huge facility for artificial intelligence (AI) partner Anthropic that went online in Q4, while the company is pouring money into AI infrastructure to try to keep up with demand for its cloud services.

No. 3: $20 billion

Amazon's chip business has a current revenue run rate of $ 20 billion, and it's growing at triple-digit rates. Meanwhile, the company said that when including internal use, it's closer to a $50 billion business. Amazon's use for internal operations helps both save on capital expenditure (capex) costs as well as inference expenses, which help improve its operating margins.

This is an underappreciated part of Amazon's business that is growing quickly. Also, not to be overlooked, in addition to its popular Trainium AI chips, the company also has its own central processing units (CPUs), which appear to be the next AI bottleneck, given the rise of agentic AI.

No. 4: 9%

Amazon's North American operating margin was 9% in Q4, which was up from 8% a year ago. E-commerce is a high-sales, low-operating-margin business, so when you see a nice improvement in operating margins, it translates into big profit gains. That's why in Q4, Amazon saw a 24% jump in North American operating income on a 10% increase in sales.

This operating leverage is being led by advancements in robotics and AI, which are just making the business more efficient. It is also benefiting from strong growth in its high-gross-margin sponsor ad business.

NASDAQ: AMZN

Key Data Points

Amazon is a great buy

The once-in-a-decade time to buy Amazon was likely during last year's dip, but now is still a great time to buy the stock, and the numbers back it up. Amazon stock is still historically and relatively cheap, while its cloud revenue growth is accelerating and it's seeing strong operating leverage in its e-commerce operations.