Over the past five years, Green Thumb Industries (GTBIF +2.28%) has lost significant market value, with its shares dropping over 70%. Like most of its peers, it has faced a range of challenges, including the sector's tough-to-navigate regulatory environment. However, Green Thumb Industries' financial results look better than those of most of its competitors. Can the company bounce back as it tries to capitalize on the growing cannabis market? Let's find out where the company might be in five years.

Image source: Getty Images.

The effect of recent regulatory changes

Green Thumb Industries is one of the leading multistate operators (MSOs), with 113 stores across 14 U.S. states, and a vast portfolio of brands and products from dried cannabis flower to edibles and cannabis-infused beverages. The company is betting that the regulatory landscape will change significantly in its favor over time, unlocking the estimated $100 billion potential of the cannabis market.

Last year, President Trump signed an executive order that led to the reclassification of marijuana to a Schedule 3 substance, which means banking services will now be easier for Green Thumb Industries to access. It will also allow the company to deduct normal business expenses (something pot growers couldn't do before the reclassification). Over the next five years, Green Thumb Industries should benefit from this. The company will likely post stronger operating margins and profits as a result of these changes.

Banking on more progress

There is a possibility that cannabis will become legal at the federal level by early next decade, though we can't be sure. How would that affect the business? On the one hand, it would open up a world of opportunities. Besides the potential increased demand for cannabis-based products, interstate commerce might be allowed. Under current laws, pot growers cannot ship cannabis across state lines, which often forces them to control everything from cultivation to retail in every state where they do business.

Legalization would solve that issue and likely lead to lower costs for MSOs, all else being equal. It would also grant Green Thumb Industries access to more traditional financial services, including the right to be listed on major U.S. stock market indexes. With increased funding, a larger market, and reduced expenses, some might think this would be a dream come true for Green Thumb Industries.

OTC: GTBIF

Key Data Points

However, legalization might be a double-edged sword for Green Thumb Industries. Part of the company's strategy that has made it so successful compared to its peers has been its focus on limited-license states, which has given it a slight competitive edge. This advantage might disappear if marijuana were legalized at the federal level. Further, Green Thumb Industries' disciplined approach has been successful in an industry where competitors pursued a growth-at-all-costs strategy despite limited access to financing.

That eventually caught up to them. But if cannabis were legalized by the highest legal authority in the country, that would likely attract larger companies in adjacent, highly regulated consumer goods markets -- such as tobacco -- with plenty of cash and the means to pursue an aggressive strategy. This could undermine Green Thumb Industries' more conservative approach.

Exercise caution

Green Thumb Industries is, without question, one of the more attractive stocks in the cannabis industry. It is one of the rare ones that generates a profit.

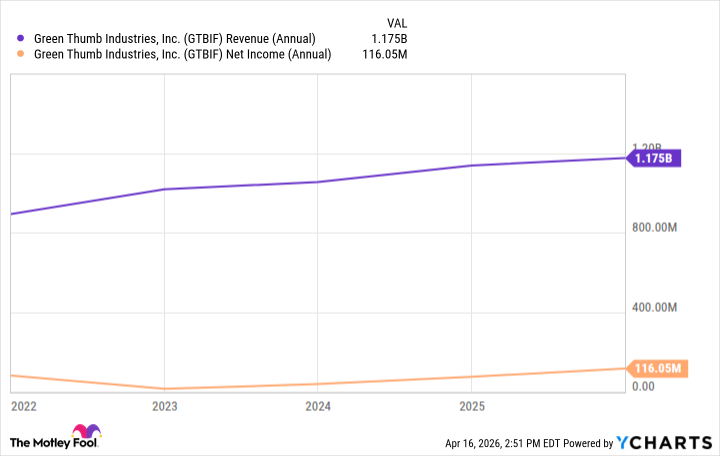

GTBIF Revenue (Annual) data by YCharts

However, the company's medium-term outlook is highly uncertain, partly due to the sector's complex landscape. Even if federal legalization happens -- and putting aside the added competition it would invite -- lawmakers might still impose restrictions that would make it difficult for Green Thumb Industries and its peers to succeed. That's what happened in Canada. So, what does that mean for investors considering Green Thumb Industries? My view is that over the next five years, Green Thumb Industries will deliver decent financial results, but will also continue to face regulatory challenges beyond its control.

The stock carries above-average risk as a result, as it may continue moving south, as it has since 2021. But for investors with a high tolerance for risk, there aren't many better cannabis stocks to consider investing in.