Electric vehicles (EV) are becoming more compelling each passing day thanks to advancements in battery performance, improving charging infrastructure, and more competition, which means more consumer options and more affordable pricing. Those are all driving factors of an EV market that's expected to more than triple in value, from $1.6 trillion in 2025 to over $6.5 trillion by 2030, as global adoption accelerates. While a rising tide lifts all boats, as they say, Rivian (RIVN +4.32%) investors have reason to believe they backed the right young EV maker -- and it's as clear as day in one critical graph.

Investing 101

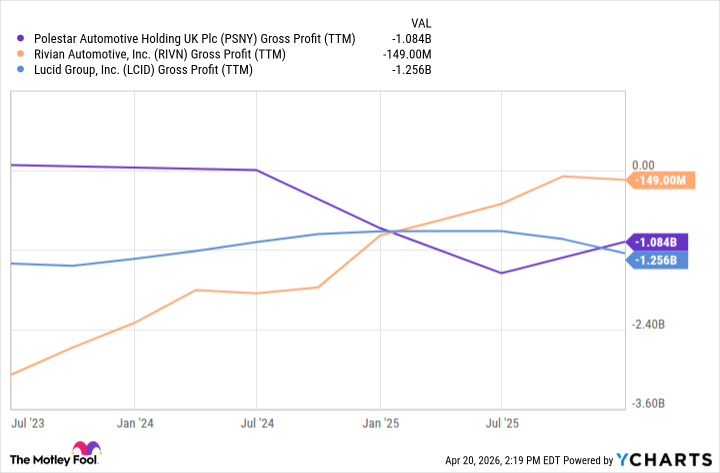

Gross profit is one of the simplest metrics in investing, but also one of the most valuable for investors to gauge how effectively a company is converting materials into finished goods. It's also a key indicator for effective pricing, and a high or growing gross profit indicates stronger financial health -- a key metric for attracting investors.

Supported by Rivian's cost engineering team, the company significantly reduced material and production costs for its R1 platform. Rivian surprised some by achieving its first positive quarterly gross profit during the fourth quarter of 2024, and surprised fewer people when it posted its first full-year gross profit for 2025. The reversal was stark: For the full-year 2024, Rivian posted a consolidated gross loss of $1.2 billion, which flipped impressively to a $144 million gross profit for full-year 2025.

NASDAQ: RIVN

Key Data Points

In addition to cost-cutting, Rivian improved its per-vehicle economics through software and services growth -- you can thank the Volkswagen joint venture for this -- as well as rising average transaction prices (ATPs) driven by second-generation R1 models hitting the roads. Rivian's full-year gross profit was a great signal itself, but that's especially true when you compare it to young EV maker rivals such as Lucid (LCID -0.29%) and Polestar (PSNY +2.63%).

PSNY Gross Profit (TTM) data by YCharts

Here's the kicker

The good news is Rivian's progress was driven by its R1 vehicles, and the recently launched R2 will further drive its progress and gross profits. In fact, Rivian's R2 platform strategically simplifies vehicle architecture and manufacturing to achieve a 45% reduction in material costs compared to the second-generation R1 platform. The key point here is that the reduction wasn't a cherry-picked statistic compared to the first R1 that rolled out of Rivian's plant.

Image source: Rivian.

I won't dive into the details, but here are a couple of examples to understand the lengths Rivian went to while driving improvements. The R2 uses a zonal electrical architecture and consolidated electronic control units, which eliminated 2.3 miles of wiring per vehicle. Rivian also eliminated thousands of individual welds and fasteners, which reduced manufacturing time and vehicle weight by roughly 2,000 lbs.

While the global transition to EVs is still in the early innings, one of the most critical metrics for luring investors, and thus driving its stock higher, is gross profit. Rivian simply doesn't get enough credit for racing ahead of similar rivals, but that could change as the R2 helps improve scale and makes its improvement more noticeable.