Chip designers like Nvidia and Broadcom get a lot of the headlines regarding their huge artificial intelligence (AI) business, but Taiwan Semiconductor Manufacturing (TSM +5.29%) is also a great pick in this industry. Taiwan Semiconductor (TSMC for short) is the primary logic chip fabricator, and the majority of tech devices use its products.

There aren't many stocks that are better picks than TSMC, and because it's staying neutral in the AI race, you don't have to worry about picking a winner -- it's a near-guarantee to be successful. I think this makes it a top buy in the market, and it just proved again why it's one of the best.

Image source: Taiwan Semiconductor Manufacturing Company.

TSMC continues to see huge growth

Management hasn't been shy about discussing the results it expects artificial intelligence (AI) to deliver. During its fourth-quarter conference call, it forecast a compound annual growth rate (CAGR) from its AI business in the mid to high 50% range for the period starting in 2024 and ending in 2029. That's huge over a long time frame, and first-quarter results backed that projection up.

Revenue growth was 41% year over year, and the forecast for 2026 total revenue growth was revised to be above the 30% figure previously provided. That's strong and impressive for TSMC, but it shouldn't come as a surprise to anyone following the industry because of how prevalent its chips are and how great the demand for AI computing has been.

NYSE: TSM

Key Data Points

Rapid growth from TSMC also bodes well for other AI businesses reporting earnings during the first quarter, and investors should expect strong quarters from Nvidia and Broadcom.

Still, I think TSMC is a great investment in its own right. Its attractiveness is that you're owning the primary chip manufacturer, which means it will benefit from the rising tide of AI spending, rather than requiring you to select one winner. That makes it a suitable choice versus others.

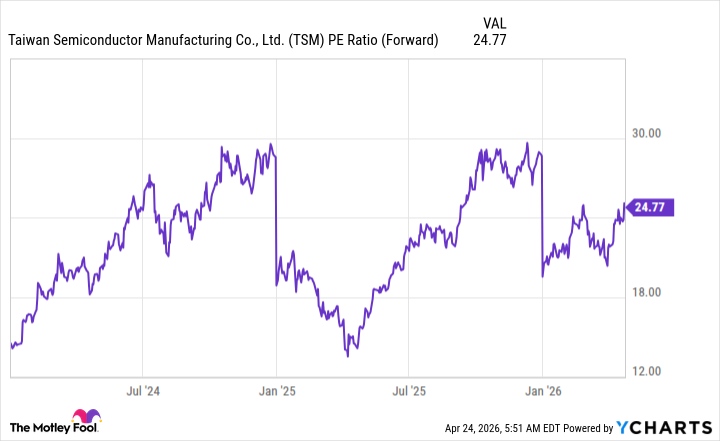

It's not the cheapest stock at 25 times forward earnings, but considering its industry dominance, exposure to huge growth, and strong track record of execution, I think it's a price worth paying.

TSM PE Ratio (Forward) data by YCharts; PE = price to earnings.

Few stocks have as few questions surrounding the health of the business as Taiwan Semiconductor, making it an excellent buy-and-hold for years to come.