Nvidia and Broadcom are among the top players in the artificial intelligence (AI) infrastructure ecosystem, designing chips that handle critical workloads related to model training and inference in data centers.

Not surprisingly, shares of both companies have jumped impressively over the past year. While Nvidia stock has shot up 95% over this period, Broadcom has clocked stronger gains of 117%. However, both AI stalwarts have been comprehensively beaten by another company that's benefiting from the huge investments in AI data centers: Vertiv (VRT -2.84%).

Shares of the company, which sells critical digital infrastructure solutions such as power management, thermal management, and server racks and enclosures used in data centers, have jumped by a whopping 270% over the past year. The increase of almost 4x in Vertiv's stock price has been driven by improving growth rates and solid prospects.

The good news is that Vertiv's rally is likely far from over. Its latest results suggest the company's growth rate should continue accelerating, translating into more upside for investors. Let's see why this AI stock hasn't run out of steam yet.

Image source: The Motley Fool.

Vertiv's solutions are in solid demand from AI data centers

AI data centers require much more electricity to run than traditional data centers, driven by the powerful chips they house to handle training and inference workloads. These chips also generate a lot of heat. Vertiv's products allow AI data centers to run smoothly. It offers uninterruptible power supply (UPS) systems, liquid-cooling solutions, thermal control and monitoring, and server racks, among other solutions.

NYSE: VRT

Key Data Points

In fact, Vertiv is a part of the Nvidia Partner Network, collaborating with the chip giant to develop solutions that will help reduce heat generation in Nvidia's AI factories. Vertiv also claims that its modular prefabricated solutions can help reduce the deployment times of AI data centers by up to 50% compared to traditional solutions.

So, it is easy to see why customers have been flocking toward the company's offerings. The company released its first-quarter results on April 22. Revenue increased 30% year over year to $2.65 billion, while adjusted earnings increased by an even more impressive 83%. The numbers clearly show that Vertiv isn't just experiencing healthy product demand but is also seeing solid margin improvement, driven by improved pricing and productivity gains.

What's more, Vertiv raised its full-year guidance. It now expects to deliver a 51% increase in adjusted earnings per share in 2026 to $6.35 per share. It was earlier anticipating $6.02 in earnings per share at the midpoint. The revenue guidance has also been raised to $13.75 billion, a 34% increase over the prior year.

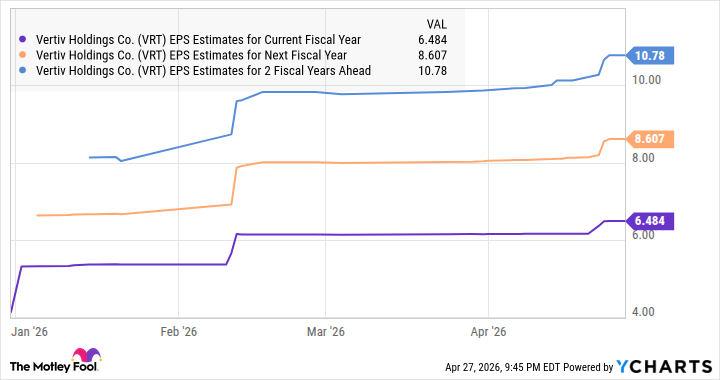

The improved guidance explains why analysts are now expecting a larger earnings jump going forward.

VRT EPS Estimates for Current Fiscal Year data by YCharts

But is Vertiv stock worth buying anymore?

Investors may be wondering whether it makes sense to invest in this tech stock after its multibagger gains over the past year. However, the strong growth potential of the AI data center market suggests that the company may be at the beginning of a terrific growth curve.

The data center cooling market, for instance, is anticipated to grow by almost 5x between 2025 and 2033, generating $128 billion in revenue in 2033. Meanwhile, demand for data center power solutions could increase from $23 billion last year to $72 billion in 2033 at a compound annual growth rate of almost 16%.

Vertiv is growing faster than these markets, suggesting it may be capturing a larger share of this space. As a result, Vertiv can sustain the eye-popping earnings growth it is clocking, making this an ideal bet for investors looking to buy a growth stock.

Of course, Vertiv is trading at an expensive 52 times forward price-to-earnings (P/E) ratio, but it can justify that valuation by outperforming consensus estimates and maintaining solid earnings growth. Assuming its earnings indeed jump to $10.78 per share in 2028 (as seen in the chart) and it trades at 43 times earnings (in line with the U.S. tech sector's average earnings multiple, which is lower than its forward P/E), the stock could jump to $463.

That's a potential jump of 44% from current levels, which means that it isn't too late for investors to buy this high-flying stock.