Nvidia's (NVDA +1.30%) start to 2026 wasn't great, but it has been an absolute rocketship since the calendar flipped to April. Since then, Nvidia's stock is up 13%, but I think that's just the beginning.

Nvidia has a lot going for it, and I think its rally could easily extend throughout the rest of the year. So, if you've missed out on Nvidia's recent run, don't worry, there's more where that came from. I've got three reasons why Nvidia's run is just getting started, and spoiler, it could last well into 2027 and beyond.

Image source: Getty Images.

1. 2026 is another major year for computing equipment

Nvidia makes graphics processing units (GPUs), which are the most popular computing units for training and running artificial intelligence models. Nvidia's GPUs are by far and away the most popular option, and this has shown up in its impressive growth rate.

Investors also know that Nvidia will have a huge growth year this year based on what its major clients are saying. At the start of 2026, the big four AI hyperscalers gave guidance for about $650 billion in combined capital expenditures this year. While not all of that goes directly to Nvidia, a large chunk of it does. With this being a major increase from 2025 levels, it's pretty obvious that Nvidia should have a stellar 2026.

NASDAQ: NVDA

Key Data Points

Management already told investors that they should expect even faster revenue growth in 2026 than in 2025, as its Q1 guidance is 77% versus the 73% growth delivered in Q4. As Nvidia reports throughout the year, it should help justify the stock price rally and will enable the run to continue.

2. 2027 and beyond will still be a strong time for Nvidia

One thing pundits may point out about Nvidia's stock is that most of 2026's growth has already been priced into Nvidia's stock. That's a fair argument, but we're already starting to hear rumblings about 2027 spending.

One example is Alphabet. It's planning on $175 billion to $185 billion in capital expenditures this year. However, management recently told investors that they expect their capital expenditures to "significantly increase" compared to 2026 values. Alphabet likely isn't alone in this guidance. While others may not have told investors what to expect, they're likely already planning out their 2027 costs, and they are unlikely to break from this trend.

As a result, Nvidia investors may start pricing 2027 growth into their projections, which could lead to the stock rallying. It's anyone's guess as to where AI spending will head. Still, Nvidia has also informed investors that it projects global annual data center capital expenditures to rise to $3 trillion to $4 trillion by 2030. It's unlikely that 2026 or 2027 is the end of Nvidia's momentum, making that another point in Nvidia's favor as a long-term investment.

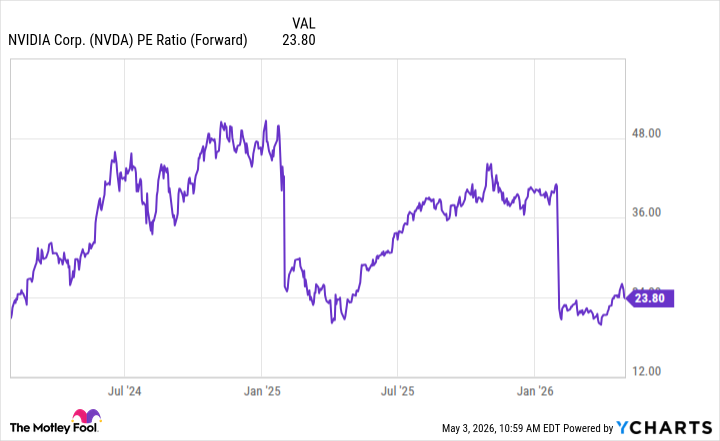

3. Nvidia isn't all that expensive of a stock

Somewhere along the way, Nvidia gained a reputation for being an "expensive" stock. While that may have been momentarily true if you were solely using a trailing earnings metric, that's not the best way to assess Nvidia. Nvidia is best assessed by using a forward-looking metric. From this standpoint, Nvidia looks fairly priced.

NVDA PE Ratio (Forward) data by YCharts

At about 24 times forward earnings, it isn't that expensive, especially when you consider that the S&P 500 trades for 21.8 times forward earnings. Nvidia is reasonably priced and has multiple years' worth of rapid growth left to go. That bodes well for an investment outlook. The market has this same information and is just now catching on, which should cause this recent rally to continue.