Micron Technology has been one of the hottest stocks on the market this year. Shares of the memory specialist have surged an incredible 90% in 2026 so far, driven by surging demand for memory chips used in artificial intelligence (AI) data centers.

However, Seagate Technology (STX -1.45%) has overshadowed the red-hot rally in Micron stock, posting outstanding gains of 164% this year. Seagate is another important player in the AI infrastructure ecosystem, manufacturing data storage solutions, including hard disk drives (HDDs) and solid-state drives (SSDs).

The company's storage products are used in a variety of applications, ranging from computers to portable storage devices to data centers. However, AI data centers have become the largest consumers of HDDs and SSDs lately, as they need to store large amounts of data for training AI models and running inference applications.

The AI data center-fueled demand has been the biggest catalyst for Seagate stock, leading to tremendous growth in revenue and earnings. Let's take a closer look at the company's latest quarterly report and check why this AI stock is built for more upside.

Image source: Getty Images

Seagate's outstanding results and guidance point toward better times

Seagate released its fiscal 2026 third-quarter results (for the three months ended April 3) on April 28. The company crushed expectations, and the guidance was also well above consensus estimates.

Revenue jumped 44% year over year to $3.11 billion. The company's earnings, however, shot up by 116% year over year, driven by a huge improvement in its operating margin. Seagate capitalized on rising prices of storage products it sells. The overwhelming demand for digital storage solutions means that cloud computing companies and hyperscalers need to act quickly to secure their share of the available supply.

This has put Seagate in a solid position to command premium pricing. In fact, Seagate notes that it has already struck supply agreements with "nearly all major cloud and hyperscale customers" for its high-capacity storage products for calendar 2027. Even better, Seagate has started negotiating supply contracts for calendar 2028 and beyond.

NASDAQ: STX

Key Data Points

With data centers producing 80% of Seagate's revenue last quarter, the long-term supply agreements that the company is putting in place with customers suggest that its phenomenal growth is sustainable. Moreover, management's comments on the latest earnings call suggest it could continue to raise prices on new contracts it signs to capitalize on the shortage of HDDs and SSDs, which could persist until the end of the decade as AI server shipments increase.

The size of the AI server market could increase by almost sixfold between 2024 and 2030, according to a third-party report. These servers will require more data storage. Not surprisingly, Fortune Business Insights estimates that the global data storage market could grow from $300 billion in 2026 to almost $985 billion in 2034 to support the large datasets needed for generative AI applications.

All this suggests that Seagate is well placed to capitalize on a secular growth opportunity that could last for years. Moreover, a closer look at Seagate's guidance makes it clear that the earnings surge that it is witnessing could continue in the foreseeable future.

Seagate expects adjusted earnings of $5 per share in the current quarter at the midpoint of its guidance range. That's nearly double the year-ago period's earnings of $2.59 per share. However, Seagate has the potential to outperform that expectation given the favorable demand-supply dynamics it enjoys.

But what about the valuation?

Seagate shares are trading at 69 times trailing earnings right now. That's expensive compared to the tech-focused Nasdaq-100 index's earnings multiple of 34. However, that premium is justified by the market-beating earnings growth that Seagate is clocking.

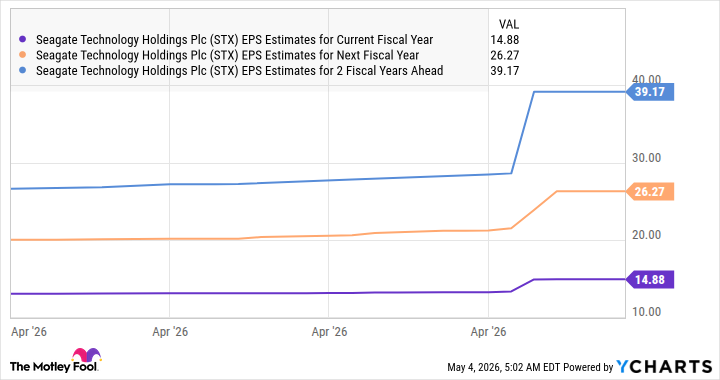

The stock has a price/earnings-to-growth ratio (PEG ratio) of 0.5, according to Yahoo! Finance. This metric is calculated by dividing a company's trailing earnings multiple by its projected annual earnings growth over the next five years. A reading below 1 indicates that a stock is undervalued given the earnings growth it could deliver. Also, analysts have boosted their earnings growth expectations from Seagate following its latest report.

STX EPS Estimates for Current Fiscal Year data by YCharts

Assuming its earnings indeed reach $39.17 after a couple of fiscal years, and it trades at 34 times earnings at that time (in line with the Nasdaq-100 index's average earnings multiple), this tech stock could reach $1,332. That's a potential gain of 77% from current levels, suggesting that investors can still buy Seagate following its stunning surge, as it has the potential to deliver more gains.