In case you haven't noticed, Bloom Energy (BE +9.18%) stock has been on an absolute tear. And by that I mean an incredibly ascendant 1,459% gain since last May.

Put differently: If you had invested $10,000 in Bloom Energy last year, you would be sitting on a decent fortune of about $167,160 today.

NYSE: BE

Key Data Points

This stock has gotten so hot lately, it could be going to the moon -- and I mean that literally.

Bloom's core technology (fuel cells) is being tested at NASA's labs, where it's considered a viable system for storing electricity on the moon. The basic technology sounds like science fiction, but it's actually straightforward chemistry: Hydrogen and oxygen combine to produce electricity, heat, and water, and then electricity can split that water back into hydrogen and water for later use. It's a closed-loop system that could be crucial not just for lunar exploration but perhaps also for a mission to Mars.

Back on Earth, however, Bloom has momentum in another groundbreaking technology -- artificial intelligence (AI). And it's this part, more than space, that may make investors regret not owning at least a little portion of Bloom stock in the upcoming 12 months.

Why a small Bloom Energy stake may be worth the risk

Bloom is a clean energy company producing solid oxide fuel cell systems (or Bloom Energy Servers) for on-site power generation. These "Bloom boxes" convert fuel, like natural gas, into electricity through an electrochemical process without combustion. Its core function is to enable customers to generate their own reliable power with lower emissions than the traditional grid.

Image source: Bloom Energy.

Bloom makes money by selling and installing these energy servers, plus offering ongoing maintenance and fuel management. As you imagine, these Bloom boxes are perfectly suited for AI data centers, which explains how Bloom has managed to partner with several major companies in this industry. Oracle, CoreWeave, Equinix, and Brookfield Asset Management are just a few names from its gilded client list.

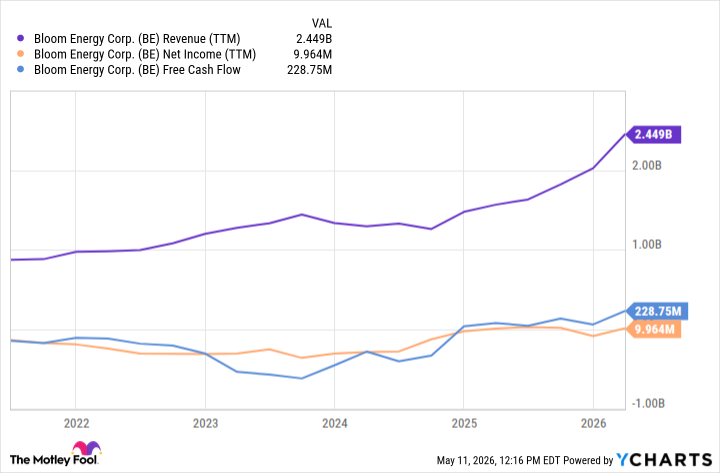

The difference between Bloom and other energy companies vying for AI clients is so simple it's almost easy to miss: Bloom actually has a product to sell. Unlike, say, Oklo or Nano Nuclear Energy, which are still stuck in a regulatory process to commercialize their energy products, Bloom has sold its servers. It's also significantly profitable, with revenue exploding from the massive demand for power from AI data centers.

Data by YCharts

The reason you may regret not owning some Bloom Energy over the next 12 months is simply this: AI data centers are taking over the world, and they need more power than the grid can supply. Indeed, according to Bloomberg, as much as 23 gigawatts (GW) of data center capacity is currently under construction, with 17 GW of that in the Americas.

And with Bloom offering faster deployment than nuclear or other clean energy technologies, a lot of that demand could end up flowing directly to its fuel-cell systems.

Of course, valuation is a concern. Trading at about 128 times forward earnings and 28 times sales, Bloom is no longer an undiscovered energy play on AI infrastructure. That's why I would keep an initial position small for now or build one gradually through dollar-cost averaging. Bloom will have plenty of room to grow if demand keeps accelerating, but at this valuation, even a good business can punish investors if expectations run ahead of fundamentals.