UnitedHealth Group's (UNH 1.89%) stock performance this year is a microcosm of the roller-coaster ride its business has been on over the past few years. From the beginning of the year through March 27, UnitedHealth's stock price dropped from $336 to $259. Since then, it has soared by more than 47% to around $381 as of market open on May 11.

UnitedHealth's stock is intriguing because the company is vital to the healthcare and financial systems in this country, but the business is undoubtedly in a transition period. So, should you buy, hold, or sell right now? Let's take a look.

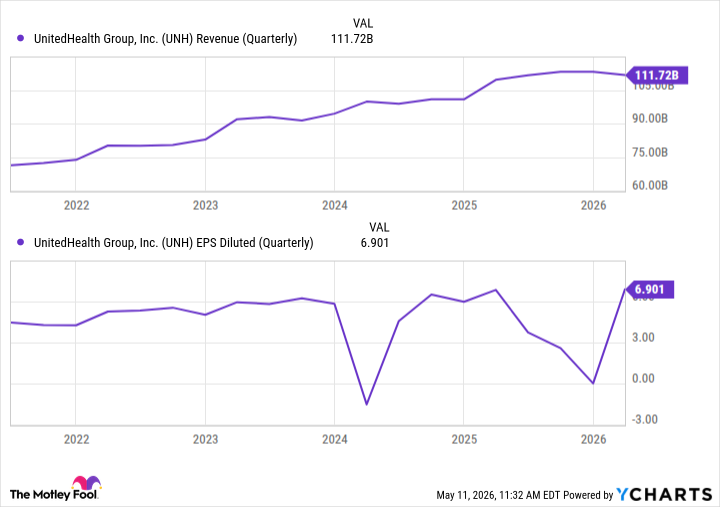

Image source: The Motley Fool.

An encouraging quarter to build on

UnitedHealth is the country's largest healthcare company by revenue, providing both insurance (UnitedHealthcare) and care (Optum). The massive, vertically integrated company benefits from two important sides of the healthcare coin, though many argue it's too large.

After dealing with leadership shakeups, rising costs, and restructuring, UnitedHealth's first-quarter performance was a reassuring sign that the company was beginning to turn the corner after a less-than-ideal 2025. Its Q1 revenue increased by 2% year over year to $111.7 billion; earnings per share (EPS) and adjusted EPS were above expectations at $6.90 and $7.23, respectively. UnitedHealthcare's operating margins increased from 6.2% to 6.6%.

These results might not appear all that impressive, but many investors know UnitedHealth's turnaround won't happen overnight, and they just wanted to see some progress. These results do suggest improvement.

Data by YCharts.

Medicare Advantage is weighing on its margins

Medicare Advantage is a supplemental addition to the government's healthcare program. And although it's connected to the main Medicare program, companies like UnitedHealth have some choice on where and whether they offer the supplemental plans. The government pays UnitedHealth for the services it provides, but in recent years, payment rates haven't kept pace with rising program costs, weighing on UnitedHealth's margins.

To address the payment and payout disconnect, UnitedHealth cut its Medicare Advantage membership by 1.3 million people in 2026. That isn't good news for the members who were let go, but it was a move UnitedHealth had to make to begin improving its margin and ensure it can sustain the program for the long term.

UnitedHealth's Medical Care Ratio (MCR) -- how much of its collected premiums it pays out to cover medical claims -- was 83.9% in Q1. This was a noticeable drop from the 88.9% ratio in the previous quarter.

NYSE: UNH

Key Data Points

Is UnitedHealth a buy, hold, or sell?

If you're a long-term investor, UnitedHealth's stock is a buy at these current prices. The company has a few regulatory hurdles in front of it -- including an antitrust investigation -- but those aren't new developments, and the issues have likely been priced into the stock.

At worst, for investors who have no interest in waiting out a turnaround story, UnitedHealth's stock is a hold because of its attractive dividend. Its current yield is around 2.3%, higher than you'd receive from an S&P 500 ETF and some popular dividend ETFs.

The upside to UnitedHealth's stock warrants taking a chance on it at its current valuation.