E.l.f. Beauty (ELF +3.56%) stock has been a huge disappointment to investors over the past few years. Despite strong growth and a solid brand that's capturing market share, the stock has struggled amid macroeconomic headwinds, including tariffs and oil-related issues.

The stock is down 27% year to date. E.l.f. reports earnings on May 20. Is now the time to buy?

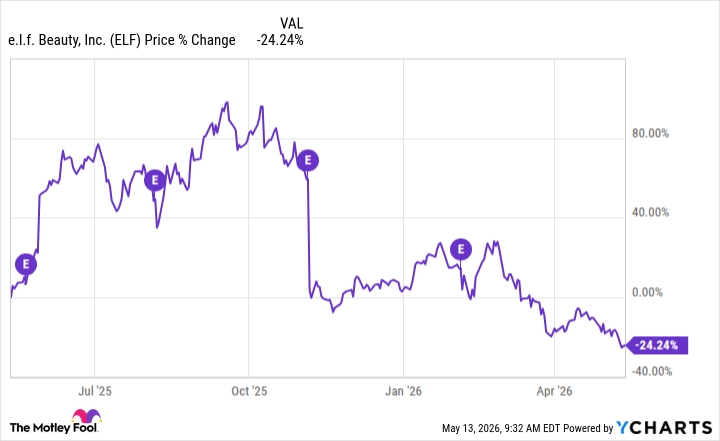

Image source: E.l.f. Beauty.

Shaking up mass beauty

E.l.f. is a relatively new player in mass beauty, especially compared with legacy names that, in some cases, have been in operation for more than a century. It has quickly climbed to the top of the industry by offering better-quality products at a fraction of the price, espousing a value-driven platform, and going all-in on digital and social media from the start.

This approach has led to incredible growth and popularity, and it's one of six publicly traded U.S. consumer companies that have reported at least 20% growth for 28 quarters straight.

E.l.f. continues to gain market share despite inflation, with 8 percentage points more over the past five years, while the top 10 cosmetics brands have lost 0.3 percentage points over the same period. It's the most-purchased brand for Gen Z, Gen Alpha, and millennials, and its Power Grip Primer is the top-selling product in color cosmetics.

Against the backdrop of economic pressure, it recently acquired celebrity Hailey Bieber's Rhode cosmetics, which has become the No. 1 brand at Sephora U.S. It recently had a record-breaking launch at Sephora U.K., and it will be launching across Europe starting in September.

What Wall Street wants

Top-line growth has been strong, but the company has been less consistent with profitability, since it's highly exposed to costs from tariffs and oil price hikes. In the 2026 fiscal third quarter (ended Dec. 31, 2025), revenue was up 38% year over year, and earnings per share (EPS) rose from $0.30 to $0.65. Management raised guidance after the report and is expecting revenue to increase about 22% for the full year and EPS of $3.07 at the midpoint, up from $1.92 last year. That's on par with Wall Street's expectations for revenue, a 22.7% increase, and slightly below Wall Street's expectations for EPS of $3.10.

E.l.f. tends to beat on EPS, but in the past four earnings reports, the stock jumped twice and fell twice.

E.l.f. is dealing with a lot of flux right now, and that volatility could continue. It could be an excellent long-term pick, and while it could jump on an earnings beat next week, there could be more pressure in the short term.