Artificial intelligence (AI) stocks are dominating Wall Street's attention right now because of their blistering returns. Suppliers of AI chips and components have been performing particularly well, with shares of memory specialist Micron Technology soaring tenfold over the past year alone.

However, that fervor for one market segment has left many high-quality stocks in other industries underappreciated, which might be a big opportunity for patient investors. Netflix (NFLX 0.04%), for instance, operates the world's largest streaming platform for movies and television shows. That business produces a reliable recurring revenue stream and an incredible amount of free cash flow -- yet its stock is still down 34% from its record high.

The stock is currently trading at an attractive valuation, so here's why now might be a great time to take a long-term position.

Image source: The Motley Fool.

Advertising is Netflix's next big growth engine

Netflix's business model used to be quite simple: Extract small monthly subscription fees from tens of millions of members, and invest those cash flows into creating and licensing an ever-growing number of high-quality movies and television shows, which, in turn, will attract still more members. But now that its subscriber base has reached an enormous 325 million, it's getting harder for the company to expand its audience, so it's finding other ways to generate growth.

In late 2022, Netflix launched a new ad-supported subscription tier. At just $8.99 per month, it's much cheaper than the company's standard ($19.99 per month) and premium ($26.99 per month) tiers, so it appeals to more budget-conscious consumers. It continues to prove popular, accounting for 60% of all new signups during the first quarter of 2026 in countries where it's available.

Unlike the company's standard and premium members, each of its ad-tier members grows more valuable to Netflix over time because it can gradually charge businesses more money for its advertising slots. This is especially true for ads aired during its exclusive live programming, which is why the company has invested aggressively in the rights to National Football League (NFL) and Major League Baseball (MLB) games, boxing matches, World Wrestling Entertainment (WWE) events, and more.

Netflix ended the first quarter with 4,000 advertising partners, up a whopping 70% from the prior-year period. Advertising revenue more than doubled last year, and management's latest guidance suggests it will double again in 2026 to $3 billion. That's still a thin slice of the pie relative to the company's overall expected revenue of $51 billion, but based on the ad segment's growth rate, it won't be long before it makes up a more significant part of the top line.

NASDAQ: NFLX

Key Data Points

Netflix stock is trading at an attractive valuation

Netflix is highly profitable, giving it an advantage over most of its competitors in the streaming industry because it can spend more aggressively on its content slate, which further cements its dominance.

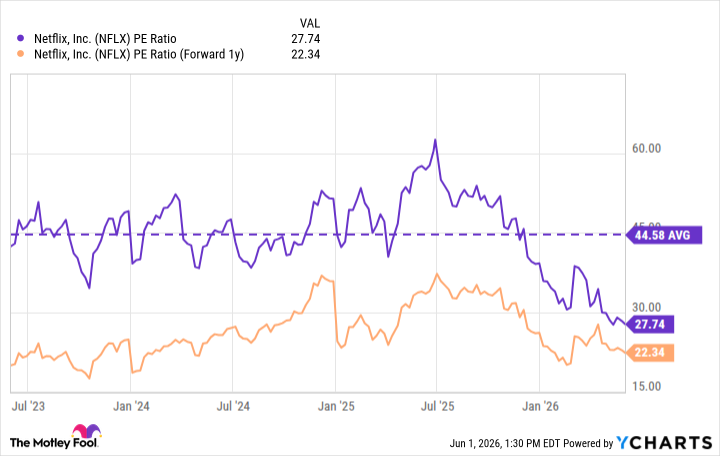

In the first quarter, Netflix's earnings grew at a brisk 86% to $1.23 per share. The company has delivered earnings of $3.10 per share over the last four quarters, placing its stock at a price-to-earnings (P/E) ratio of 27.7. That is far below its three-year average of 44.5, and it also makes Netflix cheaper than the technology-heavy Nasdaq-100 index, which trades at a P/E ratio of 35.2.

But it gets better. Based on analysts' consensus earnings estimate for 2027, Netflix stock is trading at a forward P/E ratio of just 22.3.

NFLX PE Ratio data by YCharts.

That suggests Netflix stock will have to climb by 23% before the end of next year just to maintain its current P/E ratio, but it would have to soar by 57% to match the P/E of the Nasdaq-100. The latter scenario is perfectly realistic, given that Netflix's P/E was above 30 for almost the entire last three years.

But there could be significantly more upside over the long term. Last year, The Wall Street Journal got access to an internal memo to Netflix staff outlining management's goal to double the company's revenue and triple its profits by 2030. In January of this year, co-CEO Greg Peters said he still felt good about those targets.

If Netflix does triple its earnings over the next few years, investors would see an equivalent increase in its stock price even if its P/E ratio remained at the relatively subdued level it is today. With all that in mind, it might be a good idea to step away from the AI-related exuberance for a moment to consider this opportunity, which is grounded in tangible fundamentals.