Canopy Growth (CGC +4.07%) has had a terrible go of it in the past five years. Despite the cannabis industry experiencing regulatory progress in Canada and elsewhere, the company's financial results have been subpar at best, while it has lost significant market value. Could Canopy Growth bounce back? The pot grower recently made an acquisition it hopes will be the spark it needs to turn things around. Let's find out whether there are brighter days ahead for Canopy Growth following this acquisition.

Image source: Getty Images.

Expanding its reach

On March 16, Canopy Growth completed the acquisition of MTL Cannabis, a Canadian company. MTL's portfolio of products and brands included pre-rolls, vape cartridges, dried flower, and more. It also operates in Quebec, the second-largest cannabis market in Canada, where Canopy Growth will now have a stronger presence thanks to the acquisition. According to Canopy Growth, this move makes it the leading medical cannabis company in the country by revenue. However, it wasn't a cheap transaction for Canopy Growth. The total equity value of the deal was about $125 million, but Canopy Growth paid for the transaction in a mix of cash and stock and chose to issue new shares to do so.

NASDAQ: CGC

Key Data Points

Not worth the trouble

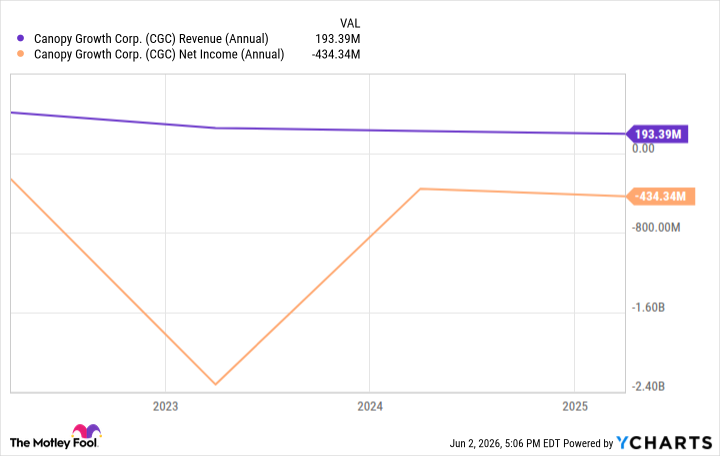

Canopy Growth has not performed well over the past few years due to challenges in its home country. Even though cannabis is legal in Canada, there remains substantial regulatory oversight that has slowed the market's progress. That's not to mention the oversupply issues stemming from significant competition in Canada. The result has been slow sales growth (at best) and consistent red ink on the bottom line.

CGC Revenue (Annual) data by YCharts

Canopy Growth's buyout of MTL Cannabis isn't the first time it has tried to improve its financial results and market position through an acquisition, but past attempts have had little success. In my view, this one will be no different. Meanwhile, Canopy Growth's issuance of new shares to fund this transaction further dilutes existing shareholders. Perhaps it would be worth it if we could reasonably expect that Canopy Growth's financial results would meaningfully improve as a result.

But beyond an immediate spike in top-line growth from the acquisition, the business's underlying fundamentals might not change much. Further, Canopy Growth is facing other issues. The company recently announced that it had identified accounting errors in several of its past financial statements and now intends to refile. While management stated that this would not affect key metrics such as revenue, gross margins, and net income or losses, it's not a good look, especially for a company struggling on multiple fronts.

So, what's the verdict? Canopy Growth is operating in a challenging-to-navigate industry with uncertain prospects, generates poor financial results, and is forced to significantly dilute existing shareholders for an acquisition that may not move the needle nearly as much as it hopes, given the challenges in Canada. For all those reasons (and more), it's best to avoid this stock.