Nvidia CEO Jensen Huang drew a lot of attention last week at a tech conference in Taiwan when he called Marvell Technology (MRVL +3.88%) the next trillion-dollar company. But I think Advanced Micro Devices (AMD -1.21%) is more likely to reach that milestone first.

Rising revenue and improving margins are signs of AMD's major catalysts, which are attractive tailwinds for long-term investors. Here are some other reasons why AMD has the advantage.

Image source: Getty Images.

AMD is a lot closer to a $1 trillion market cap than Marvell Technology

AMD has been one of the hottest artificial intelligence (AI) stocks lately, with its share price spiking more than 130% year to date. That puts its stock performance ahead of other AI chipmakers, like Nvidia and Broadcom. Marvell has outperformed AMD year to date with a major assist from Huang, but looking at both companies' market caps reveals that AMD is much closer.

The GPU chipmaker has a market cap above $850 billion, while Marvell Technology still has a total valuation below $300 billion. Marvell Technology stock must more than triple from current levels to reach $1 trillion, while AMD doesn't even need to go up by 20%.

AMD also has the fundamental growth to support a rally to a $1 trillion market cap. Revenue grew by 38% year over year, and net profits surged by 95% year over year. Meaningful sales growth, combined with rising profit margins, has been a common formula for AI stocks that go on to outperform the S&P 500 over vast stretches.

NASDAQ: AMD

Key Data Points

AMD's largest revenue segment is also its main growth compounder

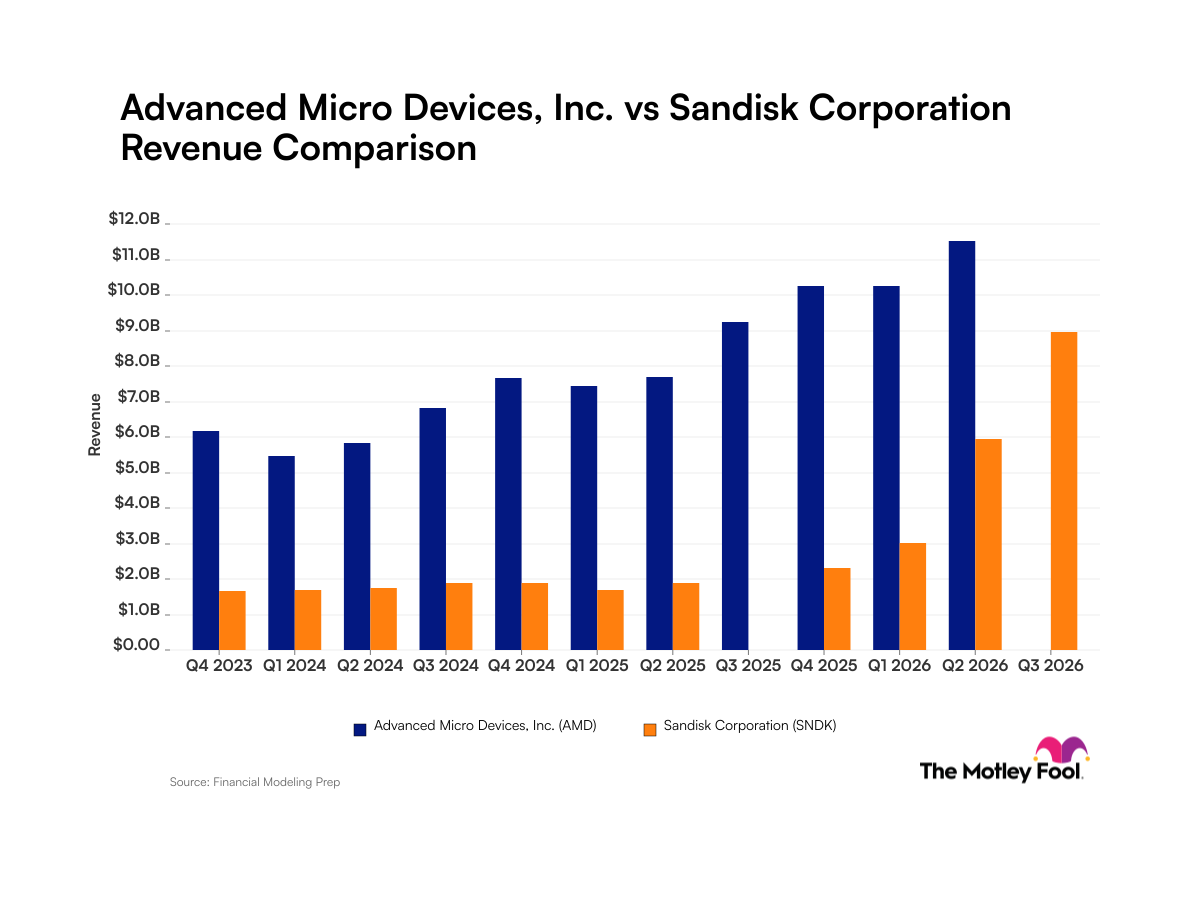

AMD reports three revenue segments that add up to its $10.2 billion in total Q1 revenue. Taking a closer look at each of those parts of AMD's business hints at accelerated revenue growth, which can fuel even more gains for the growth stock.

Embedded segment revenue came in at $873 million, up 6% year over year. That's a tiny slice of the business that doesn't contribute much to total revenue. The Client and Gaming segment brought in $3.6 billion, up 23% year over year. That segment is a bigger contributor and has a higher growth rate than the laggard Embedded segment.

However, data center revenue has been the main story for multiple years, since that centers around AMD's role in the AI build-out. AMD generated $5.8 billion from this part of the business, representing 57% year-over-year growth. That's the major growth engine that can translate into higher revenue growth rates moving forward.

The $5.8 billion figure represented 56.6% of total Q1 revenue. Since it's outgrowing the two other segments by wide margins, data center revenue should make up a larger portion of AMD's future revenue. Under that scenario, AMD's overall revenue growth rate should accelerate beyond the 38% year-over-year figure it reported in Q1.

Any positive developments around AMD's revenue growth rates can send the stock rallying, and it won't take much for AMD to reach a $1 trillion market cap if you combine solid results with a broader bullish trend. Marvell Technology may still be a few years away, but AMD can realistically become a $1 trillion company within a few months.