Broadcom (AVGO +0.37%) was one of the hottest stocks of 2026 before it reported Q2 earnings. It was up nearly 40% before selling off sharply. However, the stock is still up 18% for the year, which is still quite impressive for a six-month return.

One of the primary reasons for Broadcom's sell-off was that it didn't significantly raise its 2027 guidance. That's just an absurd reaction for the market, and it has created a great buying opportunity.

Image source: The Motley Fool.

Broadcom's custom AI chip business is gaining momentum

Broadcom does a lot of different things as a company, but what's most exciting for investors is its ASICs -- application-specific integrated circuits. These are chips that are designed with one purpose in mind and excel at it. ASICs have been used for a long time, and they're gaining momentum in the AI industry. Broadcom partners with an AI hyperscaler to design an ASIC, and then those companies buy them exclusively from Broadcom. These custom AI chips often outperform GPU-based training in terms of cost, making them even more popular than ever.

NASDAQ: AVGO

Key Data Points

Broadcom has four key clients: Alphabet, Meta Platforms, OpenAI, and Anthropic. These four clients will help boost its AI semiconductor revenue to more than $100 billion by 2027. That's a massive goal, as Broadcom's current trailing-12-month revenue is $75 billion, and most of that is from non-AI sources.

Broadcom is starting a massive, multi-year growth trajectory, yet the market is disappointed that it wasn't more. That's a silly reason to sell a stock, and long-term investors should take advantage of the sell-off and begin loading up on shares.

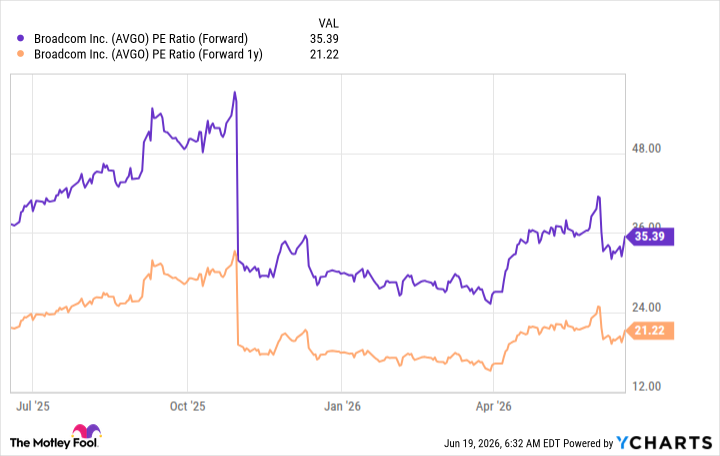

From a valuation perspective, Broadcom does look expensive at 35 times forward earnings. However, 2027 was the year of major growth, and based on 2027's earnings estimate, we get a 21x multiple.

AVGO PE Ratio (Forward) data by YCharts

That's still not cheap, but if Broadcom's custom AI chip business really starts to take market share from GPUs, it could lead to even further growth in 2028 and beyond as the AI build-out is expected to last through at least 2030, and maybe beyond. That leaves plenty of years for Broadcom's business to continue growing, and I think it makes for a great long-term investment, especially after the recent sell-off.