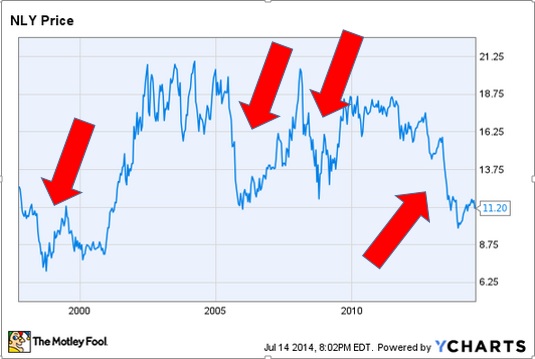

Annaly Capital Management (NLY +1.19%) has put in an impressive 529% total return since its inception in October 1997. However, those returns have been far from consistent. There have been several years in which Annaly's stock price has plummeted more than 30%.

For investors looking to avoid huge price swings, create more consistent cash flows, and sleep a little easier at night, it's as simple as also buying Wells Fargo (WFC 1.04%).

Isn't that just diversifying?

Having another holding does limit your portfolio's exposure to Annaly. But we're not talking about buying a huge basket of stocks -- just one.

Why Wells Fargo? Over the past 17 years, Annaly's strongest periods of growth have been Wells Fargo's weakest, and vice versa.

Total return

| Company | October 1997 to 2002 | 2002 to 2006 | 2006 to 2010 | 2010 to today |

|---|---|---|---|---|

| Annaly | 134% | 2% | 108% | 16% |

| Wells Fargo | 48% | 65% | (2%) | 107% |

| Evenly invested in both | 91% | 34% | 53% | 62% |

Source: Yahoo! Finance. Adjusted historical prices.

Why it works

Annaly and Wells Fargo perform the best in very different environments.

The best environment for Wells Fargo -- or any bank, for that matter -- is a strong or growing economy, which means more loans for credit cards, cars, homes, buildings, you name it. Also, since large assets -- such as homes and buildings -- appreciate in value during boom times, borrowers are less likely to default.

That's exactly what we've seen over the past five years, as Wells Fargo's net charge-off ratio -- the amount of loans defaulting as a percentage of average loans -- is a remarkable 0.35%. According to CLSA analyst Mike Mayo, that's the lowest the company's ratio has been in "modern history."

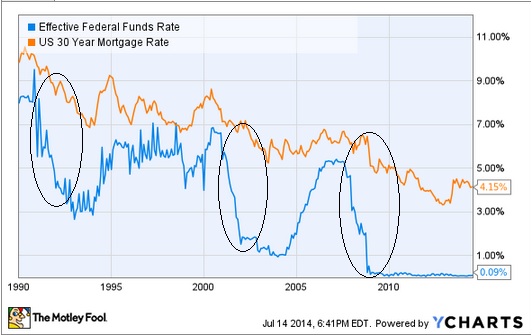

Banks also do well in a rising interest-rate environment. Since their main source of funding is deposits -- which have consistently low interest rates -- any increase in prevailing rates allows banks to lend at higher rates, ultimately increasing their net interest margin, or the difference between borrowing costs and asset yields.

mREITs, on the other hand, preform best in exactly the opposite environment. In fact, Annaly's best periods of growth have come during recessions.

To slow the economy, perhaps in the face of a market bubble or soaring inflation, the Federal Reserve will sharply increase the federal funds rate -- short-term interest rates, in other words. Once the environment has calmed, interest rates are lowered to reignite economic growth. Since long-term rates don't immediately follow, we end up with an enormous spread between long- and short-term rates:

That's the perfect investing environment for Annaly.

Calling my bluff

For those not convinced, I have a suspicion why:

- Past results don't always predict the future.

- Why Wells Fargo and not some other bank?

I can't predict the future, but I do believe in market cycles -- meaning that the economy will expand and contract over time. In fact, interest rates have risen and fallen in a similar fashion to what you see on the preceding chart every few years for the past 45 years.

I also believe that attempting to time those cycles is a mistake, and for that reason -- if you're looking for more stable returns -- it makes sense to hold businesses that perform well in different environments.

Second, while in theory this could work with any bank, why invest in just any bank? If you're going to buy a business, I would much rather hold one that's well respected, mission driven, customer focused, and led by strong management, as well as one that has a history of conservative lending and a proven track record of creating shareholder returns. Not to mention that the company pays a solid 2.6% dividend.

Ultimately, for investors who want to generate dividend income from a higher-yielding stock like Annaly but would also like to avoid some of the volatility, I believe investing in Wells Fargo will prove to be a simple and effective strategy.