Apple (AAPL +4.88%) will announce plans for its cash hoard next month, according to Howard Ward, chief investment officer at investment firm Gamco. But if this rumor proves true, the most important question remains unanswered: How will Apple return cash to shareholders? Would the company be wise to take ace investor Warren Buffett's advice, and repurchase more shares?

Share buyback programs enhance shareholder value

Share buybacks offer corporations a tax-free way to build shareholder value by buying back their own shares and, in turn, increasing shareholders' ownership percentage per share.

Buffett has been known to criticize companies for buying back their shares, but it's never because he thinks share repurchase programs are inherently bad. Instead, he criticizes companies for overpaying for their own stock.

As Buffett outlined in the 2011 Berkshire Hathaway (NYSE: BRK-A) (NYSE: BRK-B) letter to shareholders, he "favor[s] repurchases when two conditions are met: first, a company has ample funds to take care of the operational and liquidity needs of its business; second, its stock is selling at a material discount to the company's intrinsic business value, conservatively calculated."

When a company buys back its own shares, they should be "purchased below intrinsic value," Buffett explains. Price is everything: "The first law of capital allocation -- whether the money is slated for acquisitions or share repurchases -- is that what is smart at one price is dumb at another."

With $137 billion in cash and investments, Apple has plenty of excess cash. As far as the second condition, Buffett signaled a go-ahead in his March 4 appearance on CNBC, when he commented on Apple's cash hoard, "But if you could buy dollar bills for 80 cents, it's a very good thing to do."

Comparatively cheap and ripe for a buyback

Even if Buffett thinks Apple is cheap, Berkshire didn't disclose any positions in Apple in the its Feb. 14 13-F filing with the Securities and Exchange Commission. His comments, nevertheless, are encouraging to Apple shareholders.

Investors don't need to look far for proof that Apple is cheap. Based solely on fundamentals, Apple appears cheaper than nearly every company in the S&P 500.

Even Berkshire has made investments in both IBM (IBM +1.14%) and Intel (INTC 5.61%) in recent years, despite Buffett's famed aversion to tech stocks. Though Berkshire sold the Intel shares less than a year later for a 25% gain, its investment in semiconductor technologies shows that even Berkshire is sometimes willing to put its money behind highly concentrated technology blue chips when the price is right. In fact, IBM remains Berkshire Hathaway's third-largest public holding.

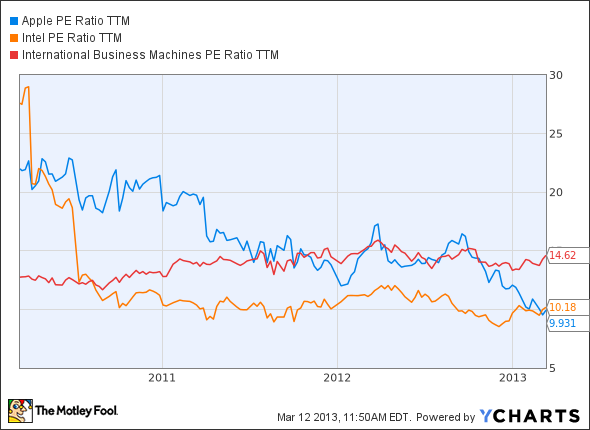

When measured by P/E, Apple now trades in line with Intel, and at a significant discount to IBM.

AAPL P/E Ratio TTM data by YCharts.

Apple was trading at a premium to IBM as recently as August 2012. But over the last six months, Apple has lost about 40% of its value as investors have grown concerned with declining margins and increased competition.

But a quick overview of Apple, Intel, and IBM's respective markets reveals far greater growth opportunities for Apple than for both Intel and IBM. Intel and IBM have three-year revenue growth rate averages of 12.8% and 1.6%, respectively. Compare this to Apple's three-year average revenue growth rate of 51.9%.

Even more telling, analysts estimate Intel's and IBM's revenues to increase by a paltry 1.4% and 1.7%, respectively, during the fiscal year ending December 2013. Meanwhile, they forecast Apple's revenue to increase 16.7% during the company's fiscal year ending September 2013.

Last but not least, the bulk of Apple's profits is positioned squarely in the center of an anticipated smartphone and tablet explosion. A report from ABI Research predicts smartphone sales to grow by 44% -- and tablet sales to grow by 125%! -- in 2013.

Apple's a prime candidate for a share buyback

No wonder Buffett encouraged Apple to scoop up its own shares. A purchase near Apple's super-conservative 52-week low would meet both of Buffett's requirements for a well-executed buyback.

Could a more aggressive share repurchase program result from the "active discussions about returning additional cash to shareholders" Apple referred to in its Feb. 7 statement? Maybe.

But no matter what Apple does with its cash, the company trades at such a conservative valuation that almost any method of returning cash to shareholders would likely impact shares positively.