As the sun sets on another earnings season, renewable energy investors will be looking toward Trina Solar (NYSE: TSL), the Chinese PV manufacturer, that is set to report on November 19.

1) The shipping news

Last week, Trina Solar updated guidance for the third quarter, estimating that solar module shipments will now be between 750 MW to 780 MW; this is an increase from the previous guidance of 650 MW to 680 MW. As a result, during its earnings conference call, Trina is expected to update its previous module shipment guidance of 2.3 GW to 2.4 GW for the full year.

Incidentally, this revision does not reflect shipments which will begin in the fourth quarter for a recently agreed upon deal with Sempra U.S. Gas and Power. According to the agreement, Trina Solar will provide Sempra with 345 MW (over 1.1 million PV modules) for the Copper Mountain Solar 3 Project in Boulder City, Nevada. The project is expected to be completed in Q1 2015, and it is the largest supply contract for a Chinese PV manufacturer in the U.S. market.

In addition to the volume of solar module shipments, investors should pay attention to how successful the company has been in its efforts to diversify its sales revenue based on geographical region. Concentrating its efforts less in Europe, Trina hopes to continue its presence in Japan, which it sees as a high margin and developing market; moreover, the company is attempting to continue expansion into new growth markets like India, Latin America, and the Middle East.

2) A smooth operator?

Updated module shipment information wasn't the only subject of the revised guidance. The company now expects overall gross margins to fall between 14.5% and 15.5% instead of the previous guidance of low double-digit margins. In terms of operating margins, the company did not provide any guidance; nonetheless, it will be interesting to see if operating margins continue to improve as they have for the past year. In the second quarter, Trina incurred an operating loss of $23.9 million -- an improvement over the $48.1 million loss in the first quarter.

|

Metric |

Q3 2013 (Guidance) |

Q2 2013 |

Q1 2013 |

Q3 2012 |

|---|---|---|---|---|

|

Gross Margin |

14.5%-15.5% |

11.6% |

1.7% |

0.8% |

|

Operating Margin |

N/A |

(5.4%) |

(15.4%) |

(25.5%) |

3) Drowning in debt or just treading water?

Concerns regarding debt seem to be inextricably linked to any discussion regarding Chinese PV manufacturers. It's easy to understand why. Suntech Power, once one of the largest Chinese PV manufacturers, recently declared bankruptcy, and LDK Solar recently arranged for an extension on the payment of overdue interest payments totaling $13 million.

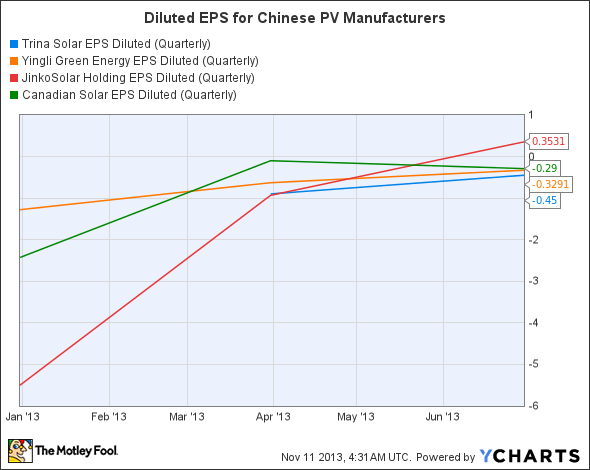

Reaffirming its commitment to remaining in good financial health, Trina Solar, over the summer, finished paying off the last of $138 million in senior convertible notes which it had issued in July 2008 . Oftentimes, it can be confusing and frustrating trying to sort though the Tier One manufacturers. Yingli Green Energy (NYSE: YGE), JinkoSolar (JKS +1.78%), and Canadian Solar (CSIQ +7.58%) are just a few of the bigger names vying for supremacy in the space. Among these, Trina is at the bottom when it comes to earnings per share.

TSL EPS Diluted (Quarterly) data by YCharts

But, remember Suntech Power? In December 2007, it was trading at $85 per share; most recently, it closed at $0.53 per share. So, let's put those earnings in perspective and look at how effectively these companies can manage debt.

TSL Debt to Equity Ratio (Quarterly) data by YCharts