Wells Fargo (WFC +0.48%) is often thought of in the same way as the best student in a class of misfits. The thought of investing in any so-called megabank can make people sick to their stomachs -- but this bank has three things going for it that make it worthy of your consideration.

1. Phenomenal performance

As the country and banking industry emerge from the financial crisis, many banks are still dealing with the headaches and damages that resulted from the burst of the housing bubble. Yet Wells Fargo has navigated the recovery well and has proved that its safer business operations helped insulate it against the troubles that befell competitors like Bank of America (BAC +0.82%), JPMorgan Chase (JPM +0.09%), and Citigroup (C +0.42%).

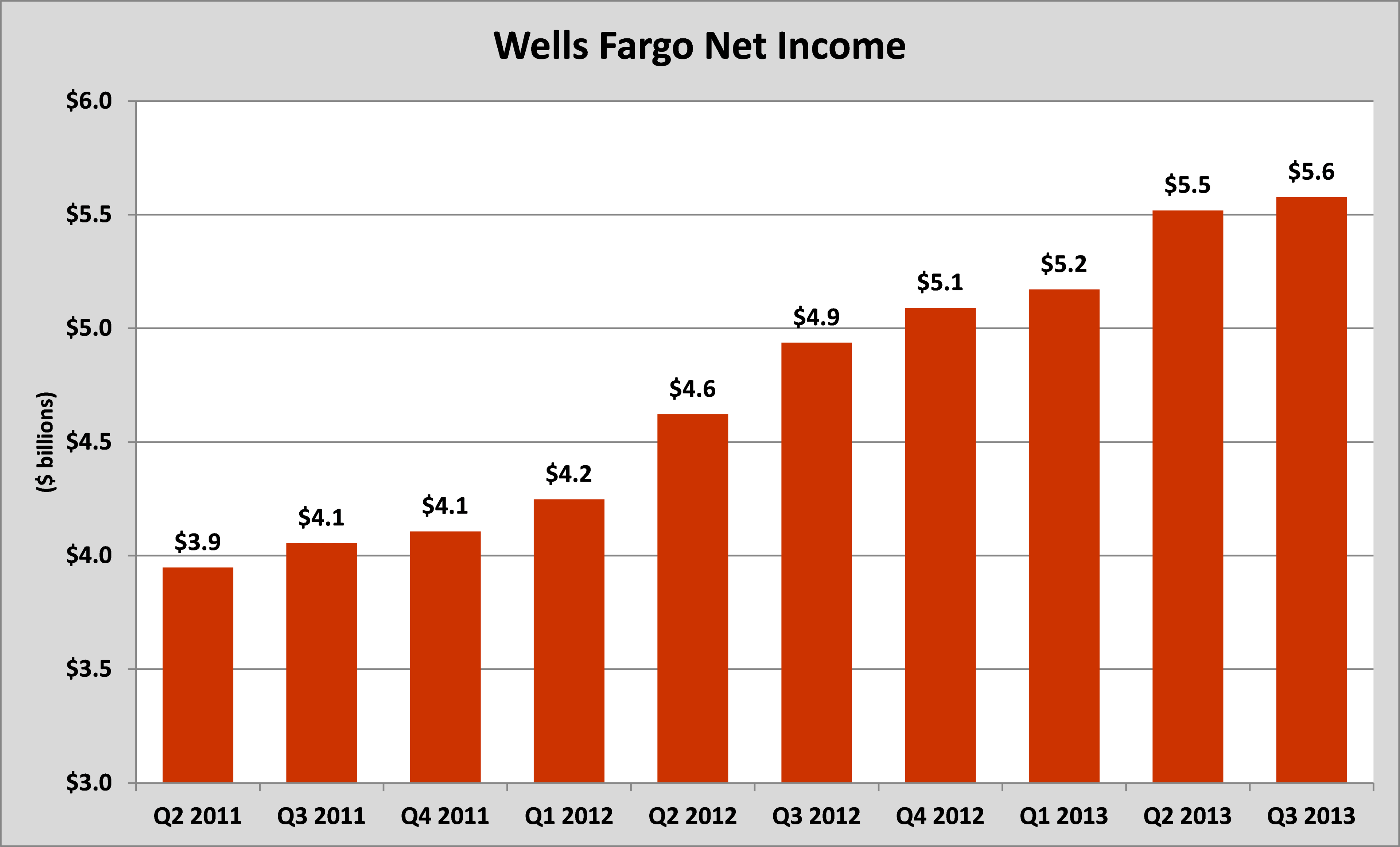

Consider that Wells Fargo has posted 10 straight quarters of record net income, as shown in the chart below:

Source: Company investor relations.

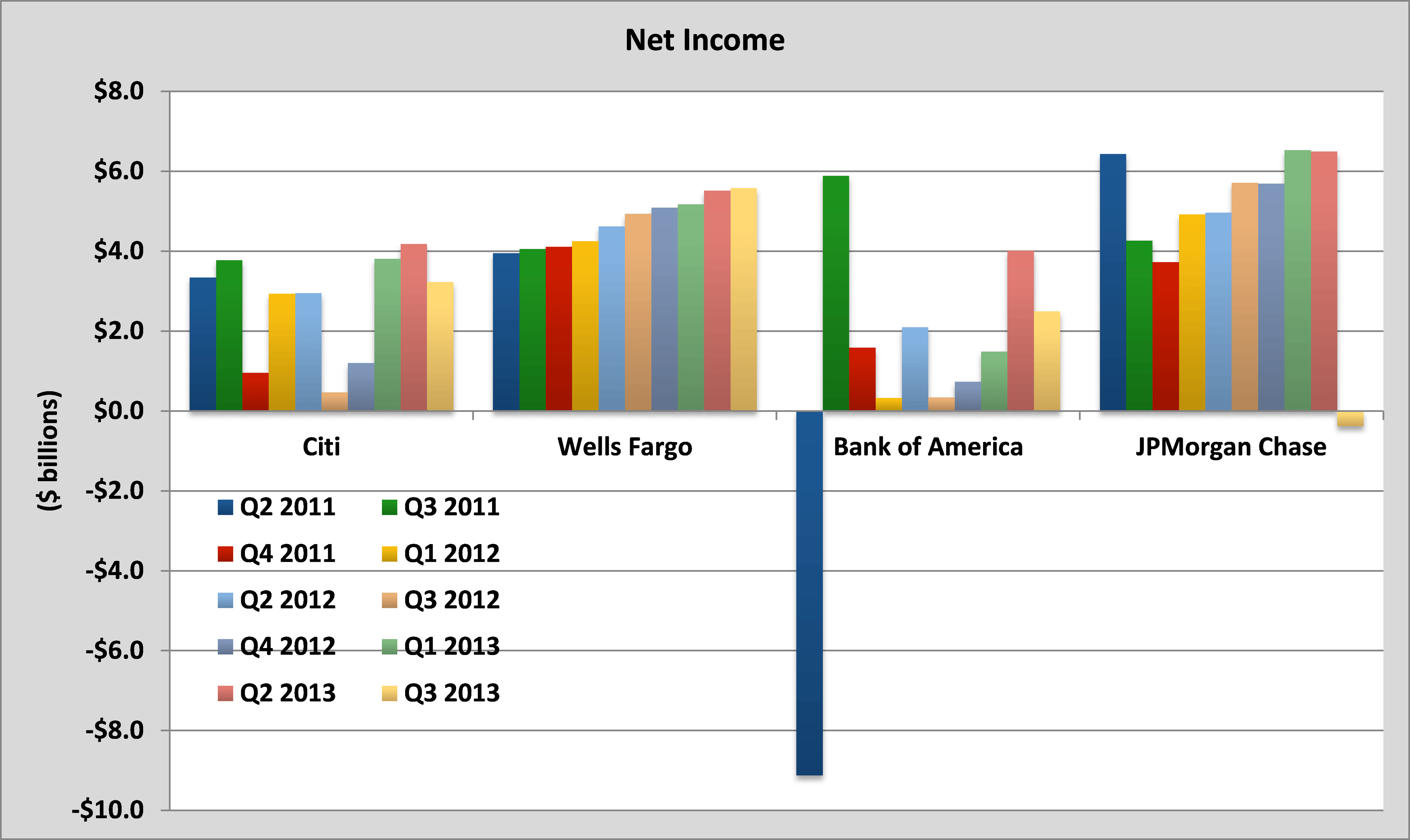

But when you compare its performance to that of its previously mentioned peers, you'll see the net income at its peer's quarter to quarter looks more like a roller coaster than a staircase:

Source: Company earnings releases.

As you can see, Wells Fargo has been able to deliver continual steady results, while peers like Bank of America, JPMorgan Chase, and Citigroup have been marked by extreme peaks and valleys. Certainly, roller coasters can be a fun thing on a Saturday, but when it describes the performance of a company, it isn't a good thing.

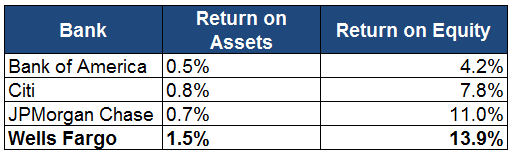

Yet it isn't simply the growing net income that is noteworthy, but it is also Wells Fargo's continued ability to generate above average levels of returns on a relative basis that is also impressive. Through the first nine months of 2013, see how its performance stacks up against fellow competitors:

Source: Company investor relations.

As you can see, Wells Fargo is best in class when it comes to delivering stable streams of income in the most efficient and effective ways possible.

2. Compelling growth opportunities

While Wells Fargo has continually delivered strong performance in the past, the natural question to consider next is how well is it going to do that in the future. Here, Wells Fargo also delivers compelling results, and it has avenues for growth in a number of different businesses.

First, its credit card business has seen the number of customers who have a checking account with Wells Fargo and a credit card grow from 28.1% to 36% from the third quarter of 2011 to the third quarter of 2013. The bank has also watched its new accounts through the first nine months of the year grow from 2.1 million in 2011 to 3.1 million this year, which represents an average annual growth of 22%.

Considering the bank has a strong, loyal deposit base, the fact that it is able to continually add new accounts and grow the share of its existing customers with a Wells Fargo card is assuredly a good thing. When you also consider that more than 64% of its clients don't have a card with the bank, there is certainly ample room for growth ahead.

While Wells Fargo is certainly a consumer business first and foremost, it too has seen impressive growth in its advisory investment banking fees with its commercial and corporate clients. Year to date, it has watched its investment banking fees grow by an astounding 52% relative to last year.

Although these two businesses only accounted for 12% of Wells Fargo's total noninterest income through the first nine months of 2013, the fact that such impressive growth has been made and potentially lies ahead means there may still be a long growth runway ahead in these areas.

3. Attractive price

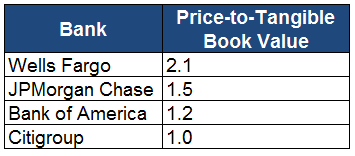

When it comes to banks, an ever important metric when it comes to gauging one bank's price relative to another is not its price-to-earnings ratio, but instead its price-to-tangible book value. This is an incredibly useful metric because it essentially filters through all the noise on a bank's balance sheet and measures what sort of premium investors are willing to pay for the actual equity available at a bank.

As you can see in the chart below, unsurprisingly, Wells Fargo has one of the highest price-to-tangible book value ratios relative to its peers:

Source: YCharts.

The natural question becomes, how is something that roughly twice as expensive as its peers be considered still being available at an attractive price? If you look at the data since 2000 about where Wells Fargo historically traded at when it comes to this metric, you'll see that it is still well below what we had typically seen:

Of course, that chart is rather choppy as a result of acquisitions and other onetime blips -- but, all in all, you can see that things are still well below historical averages. When you consider that prior to the financial crisis it was below 4.0 only for a brief period of time and it now trades at 2.1, even though it is expensive relative to its peers, the bank is still trading at a bargain.

When you take a company that delivers consistent results, has ample room for growth, and trades at an attractive price relative to historical standards, you undoubtedly have one worth considering as an investment.