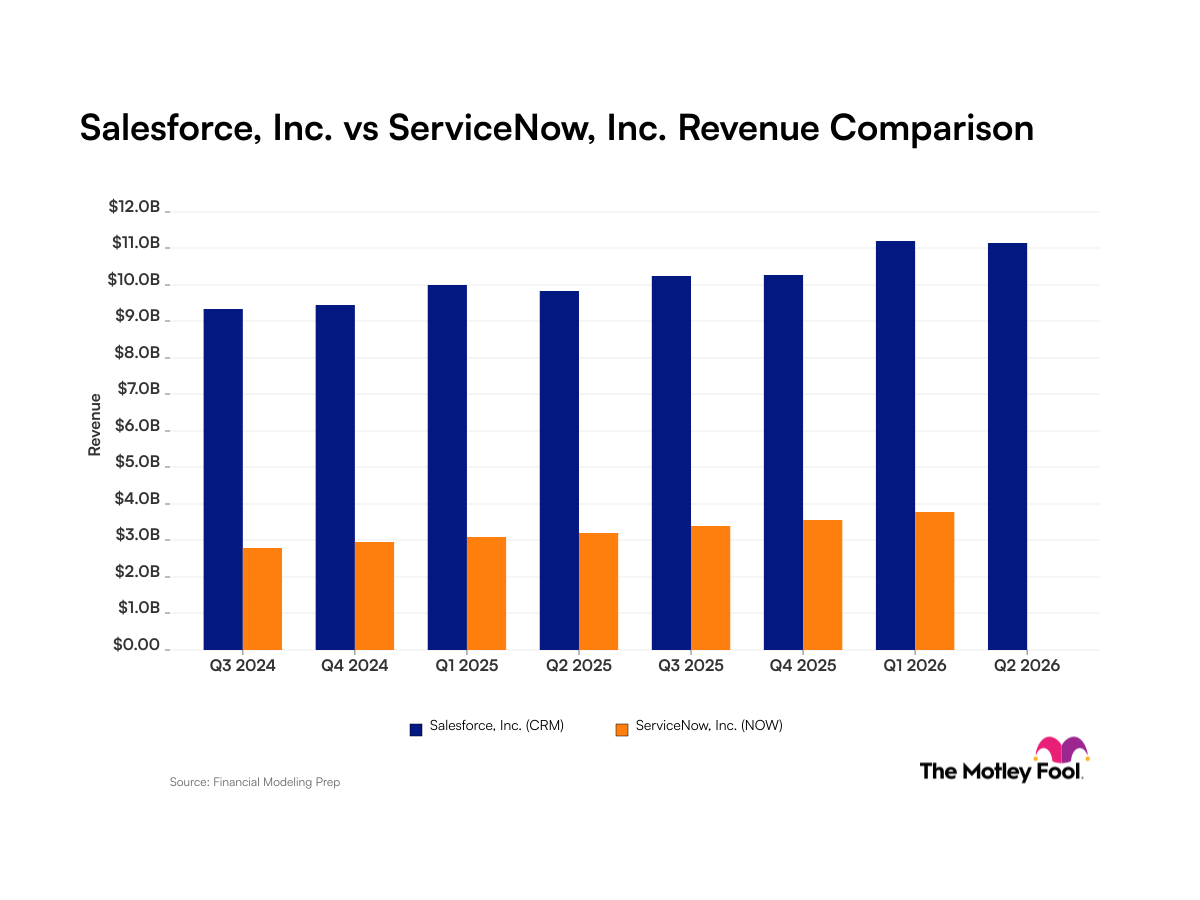

Last Friday Salesforce.com (CRM 2.45%) dropped 6% after reporting fourth-quarter earnings the night before, and followed that with another 1.5% drop to start off the week. This might seem counterintuitive to those who saw headlines of beats on both top and bottom lines, combined with a $100 million increase for fiscal 2015 full-year revenue guidance. Let's dig a little deeper into the most recent earnings release to see if we can find some answers.

Were expectations simply too high?

Putting aside some of the more concerning financial details that we'll examine later, the simplest explanation may be the best one: Salesforce rallied strongly into earnings, rising 20% between the start of 2014 and the earnings release, and expectations were running high, spurred on by broker reports of a potential "blow-out" quarter. In the face of such hyperbolic language, the beat seems relatively modest, and perhaps the sell-off was nothing more than a slight reversion to the mean of a market that has been essentially flat on the year.

So should you consider this pullback a buying opportunity? Maybe not once you look at several other important financial metrics.

Operating leverage is going the wrong way

The continued earnings deleveraging certainly should be cause for concern. Even using management's preferred "Non-GAAP" metrics, Salesforce is continuing to spend more to earn less. Non-GAAP operating profit margins declined to 6.9% in Q4, and 8.9% for the full year, down from 12.9% and 11.7% for the previous Q4 and full year, respectively. While investors typically aren't concerned about profitability at smaller, fast-growth companies with plenty of opportunity in front of them, it's hard to make that argument for a company that is a market leader in its category, and is already doing over $4 billion in annual revenue.

By the time you reach that size, you'd like to be seeing increasing returns to scale, not the opposite. When you look at actual GAAP accounting (which you probably should) things look like they are going to continue to get even worse. For fiscal '15, the company's own guidance calls for EPS to decline further into losses even as revenue grows to over $5.2 billion.

Organic growth appears to be slowing

Digging deeper into the numbers also reveals some concerns that even the top-line might not be growing as fast as it initially appears. Due to the nature of accounting for Salesforce's subscription-based product, revenue is actually a more backwards looking metric than it would be for a standard company. Accordingly, analysts like to look at total "bookings" which is revenue, plus the change in deferred revenue on the balance sheet.

The idea is that this provides better insight into how much new business was actually signed during quarter, before it flows through to revenue on the income statement. On this front, the headline number of a 37% increase is somewhat deceiving. Once you factor out the benefit the company gained from its recent ExactTarget acquisition, plus the impact of their continued effort to switch more customers to annual rather than quarterly contracts, the "organic" growth of the company's core business comes in at a more pedestrian 25%.

The search for a new CFO

Lastly, there was the announcement that CFO Graham Smith will be retiring in March 2015. Wall Street's ears always perk up on news of a key executive leaving, and some may even make the more sinister assumption that he's trying to get out before the house of cards collapses, but my personal opinion is that any serious negative reaction on this front could be overblown. If nothing else, the fact that this announcement is coming a year in advance of his actual departure should allay concerns of imminent doom.

Foolish takeaway

Overreaction to the CFO departure aside, the overall financial picture at Salesforce.com, combined with its super premium valuation warrants caution. If you're looking for extreme growth consider smaller companies that are earlier on in their growth trajectory. For companies that have already established themselves as a market leader, a business model with proven profitability may be a better bet.