Wells Fargo (WFC 1.15%) will kick off earnings season for the banking sector this week, and there are three things investors need to keep an eye on when the bank reports its results from the first quarter.

1. What it thinks of its own stock price

The biggest news in the banking world during the first quarter came when the Federal Reserve announced the results of its stress tests. Unsurprisingly, Wells Fargo passed with flying colors, whereas Citigroup (C 1.38%) was denied its plan to buyback $6.4 billion worth of its common stock. The results from Bank of America (BAC 0.80%) certainly left something to be desired, too, but it was met with the good news that it could raise its dividend from $0.01 per quarter to $0.05 per quarter, and buyback $4 billion worth of its common stock.

Yet, what didn't receive an appropriate amout of coverage regarding the announcement from Wells Fargo was the staggering $17.5 billion value of its buyback request. In addition, it had another $3.5 billion already approved from an existing buyback plan, meaning it has more than $21 billion available to repurchase its own shares.

Source: S&P CapIQ

With all that in mind, it will be important to monitor how and when Wells Fargo uses that money. If the bank keeps a tight grip on those funds and isn't active in repurchasing its own stock with such a big budget, it may give investors reason to pause. On the other hand, if it aggressively buys back more of its shares, it could serve as another reason to think that, even despite its expensive valuation -- as shown in the chart to the right -- relative to both Citigroup and Bank of America, it's worthy of an investment consideration.

2. How it seeks growth

When discussing the results from Wells Fargo in 2013, CEO John Stumpf concluded his prepared remarks by noting:

During the year ahead, we will continue to build on our commitment to our customers and to our shareholders, and invest in our businesses to generate growth for decades to come. Our earnings power and capital strength have never been stronger. We believe we are well positioned for 2014, and we are optimistic about the many opportunities ahead for continued growth.

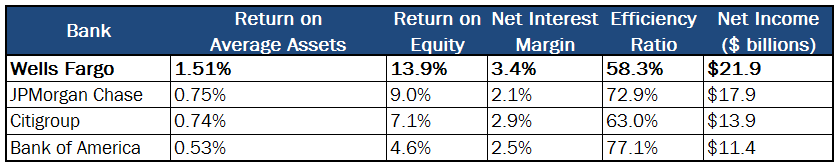

For a bank that continually outpaces peers in every profitability metric -- the reason for its high valuation mentioned earlier -- the suggestion that further expansion and growth is ahead of it is a compelling consideration.

Source: Company Investor Relations.

It will be important to see exactly where Wells Fargo seeks growth. Will it look to continue to expand its credit card and wealth management units? Will it broaden its horizon to another business altogether? Or will it perhaps simply seek to build deeper and more expansive -- and, ultimately, more profitable -- relationships with its existing customers and clients?

Many believe growth is ahead of Wells Fargo; but the question becomes, where is the growth coming from?

3. Can it maintain its industry-leading grip?

Many people are aware that Wells Fargo is the dominant bank in the mortgage market, but it also holds the top position in commercial real estate, middle market and small business lending, and automotive loans.

The previously mentioned growth prospects are certainly appealing and worth watching, but Wells Fargo has done a remarkable job at delivering returns to shareholders through success in its core operations. As a result, it will be critical to see how well it's doing in these areas to get a true picture of its success moving forward.

From the outside, it appears Wells Fargo has had another quarter where it continued to hold its position as one of the best banks in America; but, as with everything, it's truly what's on the inside that counts.