TRW Automotive Holdings (NYSE: TRW) shares have performed amazingly well since 2009, shooting from around $4 to more than $85 currently, which translates to gains in excess of 2,100%. The shares gained 57% in 2013.

Interestingly, the shares still look surprisingly cheap even after tucking in the impressive gains. TRW's forward P/E ratio of 11 is well below the readings of its two industry peers in the automotive parts supply business Delphi Motors (DLPH +0.00%) and Eaton (ETN +0.20%).

Tier 1 Status

TRW has been spending heavily to expand its supply capacity. The company spent $735 million last year to improve its plants, and plans to spend a further $730-$750 million this year to ramp up its capacity even further.

The auto parts supplier is now a Tier 1 auto parts supplier, and supplies parts to Ford, General Motors, Volkswagen, and Chrysler. Last year, Volkswagen was TRW's biggest customer accounting for 24.7% of its sales, Ford was second with 18.5% of the company's sales, while GM and Chrysler accounted for 10.1% and 9.9% of sales, respectively.

TRW Automotive's revenue grew 6% in fiscal 2013 to $17.4 billion, and 5% in the first-quarter of 2014 to $4.4 billion. The company's U.S. sales have grown 25% since 2011, from $4.0 billion to $5.0 billion last year. The healthy U.S. economy has increased sales of pickup trucks and SUVs, which are more profitable for both auto parts suppliers and vehicle manufacturers.

China sales have also improved considerably over the period, rising from $1.7 billion to $2.8 billion, a 65% growth. The North American market remains TRW Automotive's most important market accounting for almost 30% of the company's sales, while China accounts for 16% of sales. Good growth in these markets has helped offset Eurozone weaknesses, where sales have slumped. The company's European sales have dropped since 2011 from $2.6 to $2.2 billion.

TRW Automotive is Oakmark Select Funds' top holding. Oakmark is a deep-value fund that invests in undervalued stocks. Mr. Bill Nygren, Oakmark's manager, told Barron's recently that he expects the stock to move up to a valuation multiple of 15 similar to Delphi's and Eaton's. This would imply a share price of $150, 76% higher than the current price.

Oakmark Select 1 Top 10 Holdings

|

Company |

% of Portfolio |

Additions in the last quarter |

|---|---|---|

|

TRW Automotive |

7.89% |

+ |

|

TE Connectivity |

6.5% | |

|

Bank of America |

6.11% | |

|

Capital One Financial |

5.53% | |

|

Apache |

5.4% | + |

|

Medtronics |

5.2% | |

|

DirecTV |

5% | |

|

American International Group |

4.89% | + |

|

MasterCard |

4.89% | |

|

JPMorgan Chase |

4.8% |

Source: Morning Star

Delphi Auto's strong EPS growth

Delphi Motors manufactures vehicle components, and provides electrical and electronic power-train solutions for commercial vehicles. The company has demonstrated a pattern of positive EPS growth over the past one year. Delphi's EPS grew 17% in the first-quarter of 2013, and 18.2% in the first-quarter of fiscal 2014. The shares have gained 39% over the past twelve months.

Q2 2014 and Full Year 2014 Outlook

Delphi's second-quarter and full year 2014 financial guidance is as follows:

|

(in millions, except per share amounts) |

Q2 |

Previous |

Current |

|---|---|---|---|

|

Revenue |

$4,375-$4,475 |

$17,200-$17,600 |

$17,200-$17,600 |

|

Adjusted Operating Income |

$525-$550 |

$1,950-$2,050 |

$1,975-$2,050 |

|

Adjusted Operating Income Margin |

12%-12.3% |

11.3%-11.6% |

11.5%-11.6% |

|

Adjusted Earnings Per Share |

$1.27-$1.35 |

$4.70-$4.95 |

$4.80-$5.00 |

|

Cash Flow Before Financing |

$1,100 |

$1,100 | |

|

Capital Expenditures |

$800 |

$800 | |

|

Depreciation and Amortization |

$600 |

$600 | |

|

Adjusted Effective Tax Rate |

18% |

18% | |

|

Share Count-Diluted |

309 |

306 |

Source: Delphi Motors

The mid-point EPS growth for the full year represents an 11% growth.

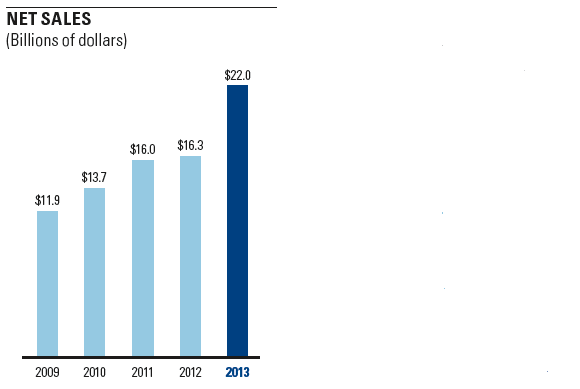

Eaton revenue grows following Cooper acquisition

Eaton derives about half of its revenue from the U.S., and another 25% comes from developed international markets. The rest comes from emerging markets. Growth seemed to have stagnated from 2011 due to weak demand in the company's end markets. But, Eaton saw its topline expand 35% in fiscal 2013 after it completed the acquisition of Cooper for $13 billion in 2012.

Source: Eaton's 2013 Annual Report

Eaton's shares yield 2.7%. The payout ratio clocks in at 42%, implying that there is still ample room for growth.

Bottom line

Global demand for new vehicles has been growing steadily, and this has translated to more business for auto parts manufacturers. TRW Automotive's increased production capacity will lead to higher revenue growth for the company in the coming years. The shares look quite cheap and are a good buy.