The further away we get from the abysmal first quarter, the less likely it seems to be repeated. This morning, Automatic Data Processing (ADP +1.37%) released its private-payroll update for June, providing another round of economic data in support of the idea that first-quarter GDP was a weather-wracked outlier.

The report shows addition of 281,000 private-sector jobs last month on a seasonally adjusted basis, boosting the three-month average for job growth back up over 200,000 -- for only the fourth time in the past year -- and returning that average to levels not seen in more than a year. The latest ADP figures also blow the doors off of most economists' expectations, and show that more jobs were created in June than had been created in any one month for nearly two and a half years.

Source: Automatic Data Processing.

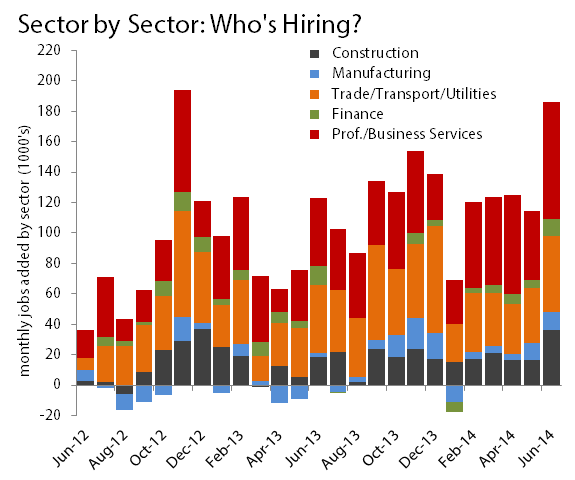

More construction jobs (36,000) were created in June than had been created in any one month -- except December 2012 -- since 2006. This resulted in the second-fastest rate of month-over-month growth in construction jobs since ADP began tracking jobs numbers in 2001. White-collar work also enjoyed its largest one-month job surge (77,000) since early 2012:

Source: Automatic Data Processing.

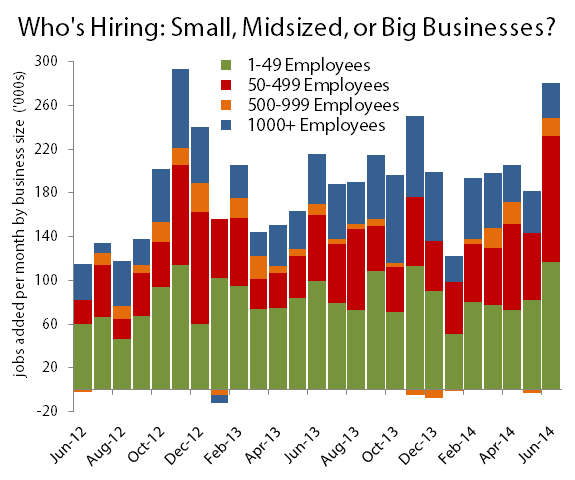

ADP found that midsized businesses, which employ between 50 and 499 people, added 115,000 new jobs in June, which is the highest rate of midsize-business job growth since 2007.

Source: Automatic Data Processing.

In many regards, this jobs report confirms what a large number of economists believe: the American economy is rebounding rapidly from a lousy winter. Despite this good news, major indices were largely unchanged -- the Dow Jones Industrial Average (^DJI +1.01%) finished at 16,976 points to record a 20-point gain for the day, an improvement of 0.12% over yesterday's record close (and thus a new all-time high close in its own right) but not enough to move past a largely meaningless 17,000-point barrier. Without a 1.1% gain from IBM (IBM +1.47%), its second heaviest-weighted component, the Dow would probably have finished in the red even though 16 other components closed in positive territory today.

Analysts and market-watchers are increasingly learning to ignore the ADP jobs update in favor of the Bureau of Labor Statistics' official monthly report, which is scheduled to be released tomorrow. Last month, ADP came in far below expectations by reporting a mere 179,000 new jobs, which turned out to be well below the 217,000 new jobs -- enough to set a new employment record -- reported in BLS data a mere two days later. The gulf in ADP's jobs numbers from May to June, and the discrepancy between ADP's data and the government's figures, probably point toward a lower number of new jobs for June in tomorrow's BLS report.

MarketWatch's average of economist projections points to a gain of 215,000 new jobs in the June BLS update, while Dun & Bradstreet estimates we'll see 244,000 new jobs. This is more or less in line with the slow-and-steady progress the American economy has made over the past few years, and it's nothing to get excited about, which certainly explains why the Dow barely moved today. We'll see if things are really getting better on the job front soon enough.