Warren Buffet said, "Cash combined with courage in a time of crisis is priceless." These words go well with Caterpillar (CAT 2.04%), the global leader in heavy equipment manufacturing. Cat makes good use of its substantial financial reserves and keeps investors happy with steady dividend payments even during tough times. It's remained a reliable dividend-paying company for the last 20 years. Even the recent mining equipment business slump has not stalled its dividend hikes. For a cyclical company like Cat, how long could this be sustainable?

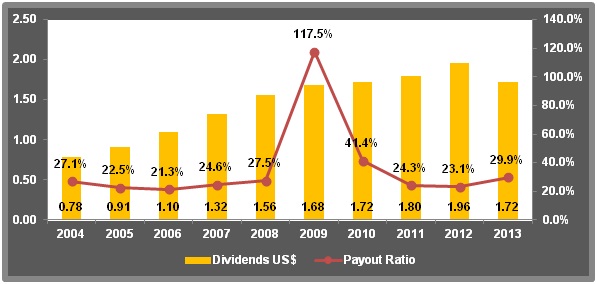

Dividend history

Cat has paid a cash dividend to its shareholders every single year since it was formed in 1925, and has regularly increased its dividend in the past 20 years. Since 1998, the company's dividend has increased by more than three times. Last month, the company increased its dividend by 17% or $0.10 to $0.70 per share. Exactly a year before, Cat had boosted its dividend by 15% or $0.08 to $0.60 per share. These are big jumps, but Cat's dividend payout ratio in the past 12 months has been a modest 39.4%. A very high payout ratio might have been risky in the current scenario.

Commenting on the recent hike, CEO Doug Oberhelman said, "This dividend increase demonstrates our financial strength and confidence in long-term prospects for the company. Despite business and economic uncertainties around the world, our balance sheet has remained strong – the strongest it's been in more than two decades – positioning us to perform through the cycles."

Chart made by author, Source: Data from Morningstar.

Better prepared to handle cyclicality

Cat's business is linked to the ups and downs of the world economy, which means that its P/E will continue to be volatile in the foreseeable future. Management is taking steps to ensure that profitability and shareholder returns during down cycles are protected to the greatest extent possible, however.

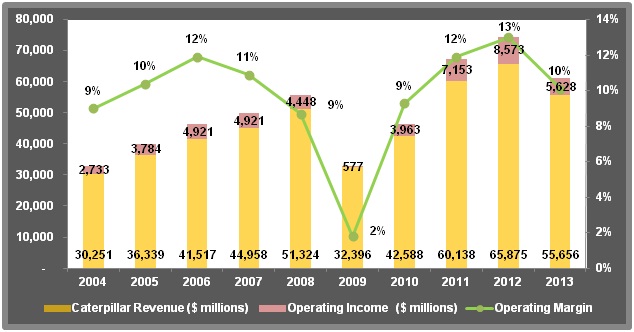

Chart made by author. Source: Data from Morningstar.

The chart above highlights the cyclicality of Cat's operations. Its revenue slumped in 2013 and 2009, but there's a difference between how the company handled it then, and how it's handling it now. When it was hit by the financial recession in 2009, the drop in its operating margin and operating income were more severe than what we saw in 2013. Then, the profound slump in the mining sector washed away $10 billion from the top line. Cat managed to keep an operating margin in excess of 10% in 2013 and ended the year with the third highest profits in its history.

The 2009 downturn was a lesson well learned, and Cat has been cutting costs, improving quality, and bettering its asset utilization. Here are some key management objectives:

- Grow profits at 15% CAGR, to be achieved by growing sales at 7%-9% CAGR and aiming for incremental margin

- Generate same quantum of profits with a lower asset base

- Take out $2 billion-$4 billion from the cost structure by 2018 through lean transformation

The company is also working with its dealers to improve their individual performance. Cat estimates that if the dealers reach even a median quartile performance then they could add an extra $9 billion to sales. If the dealers reach the topmost quartile, the potential doubles to $18 billion.

Earnings prospects and cash generation

Cat's earnings trend from 2004 to 2013 traces its sales pattern: earnings rose until 2008 before falling drastically in 2009, and again increased till 2012 before it fell in 2013. The fall was cushioned by the $1.2 billion cost savings that Cat achieved through lower research and administrative expenses coupled with a headcount reduction of 9,700. The savings were also reflected in the first quarter of 2014 as earnings improved 10% to $1.44 a share from $1.31 reported in the same quarter a year ago.

Analysts estimate that even if the mining industry does not regain momentum, the company's revenue could grow at 1% in fiscal 2014 and 5.9% in fiscal 2015 as construction equipment sales are expected to improve in North America and China. Bloomberg analysts are expecting Cat to earn $5.81 per share in 2014.

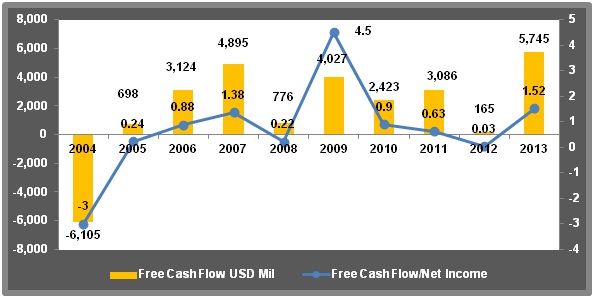

Chart made by author, Source: Data from Morningstar.

Cat's strength lies in its strong cash flow generation. The company has revved up its cash-to-cash cycle, and it's showing up in the numbers. It generated its best-ever free cash flow of $5.7 billion in 2013 -- a year of sales decline -- and ended the year with more than $6 billion in cash reserves.

Over the years, Cat has been able to convert most of its net income into free cash comfortably. The ratio nearly bottomed in 2012 when its capex skyrocketed to around 97% of operating income, but since then, Cat has scaled back capital spending. It was spending $8 billion a year on acquisitions between 2010 and 2012, which halved to $4 billion in 2013. Management has not provided an exact estimate for the next five years, but it has said that the company will have more than $4 billion in cash to spend on growth every year.

Chart made by author, Source: Data from Morningstar.

Foolish takeaway

Cat has taken some good measures to sustain profitability amid the cyclical ebbs and flows its markets are subjected to. It's generating solid cash flows and is not hesitating to distribute it among investors. Despite the current sales downturn, Cat's dividends look well protected.