In the second quarter, Discover Financial Services (DFS +0.00%) reported its earnings per share grew by 13%, to stand at $1.35, which set a record for the company. A dive into the numbers revealed that, while the second quarter produced a record, there was reason to think even better results were to come. Management gave its honest insight on the most recent quarter and what could be ahead; as it turns out, investors have even more reason to be optimistic.

1. The number of shares will continue to plummet

According to CFO, Mark Graf:

During the quarter, we repurchased $177 million of common shares. One of our top priorities is to drive shareholder value through effective capital management. To that end, we still plan to repurchase a total of $1.6 billion of common shares for the four-quarter period ending March 31, 2015, the same amount as our CCAR capital action submitted to the Fed.

During the last year, Discover has seen its common shares outstanding fall by roughly 5%, as it has spent roughly $1.2 billion on buybacks. Yet, based on Mark Graf's comment above, if $1.6 billion will be repurchased during the four-quarter period ending next March, the company's common shares will only continue to plummet. In this quarter -- which would mark the first of the four-quarter period ending in March -- just $177 million in shares were repurchased. Investors can expect another $1.4 billion to be spent, which will, in turn, significantly boost available earnings.

2. Strong growth has been a theme

When Nelms was asked about the ability of Discover to continually grow the loans Discover issues, he responded:

American Express is the only really large competitor that's growing close to our levels. And the other largest issuers are sort of plus or minus 2% ranges. So I'm not seeing an overall industry pickup to our levels of growth. So it looks -- the industry as a whole looks pretty flat. Maybe the industry has moved from minus 1% to plus 1% or something, but it's still darn near flat. And so I'm very pleased with our 6% growth with a flat industry.

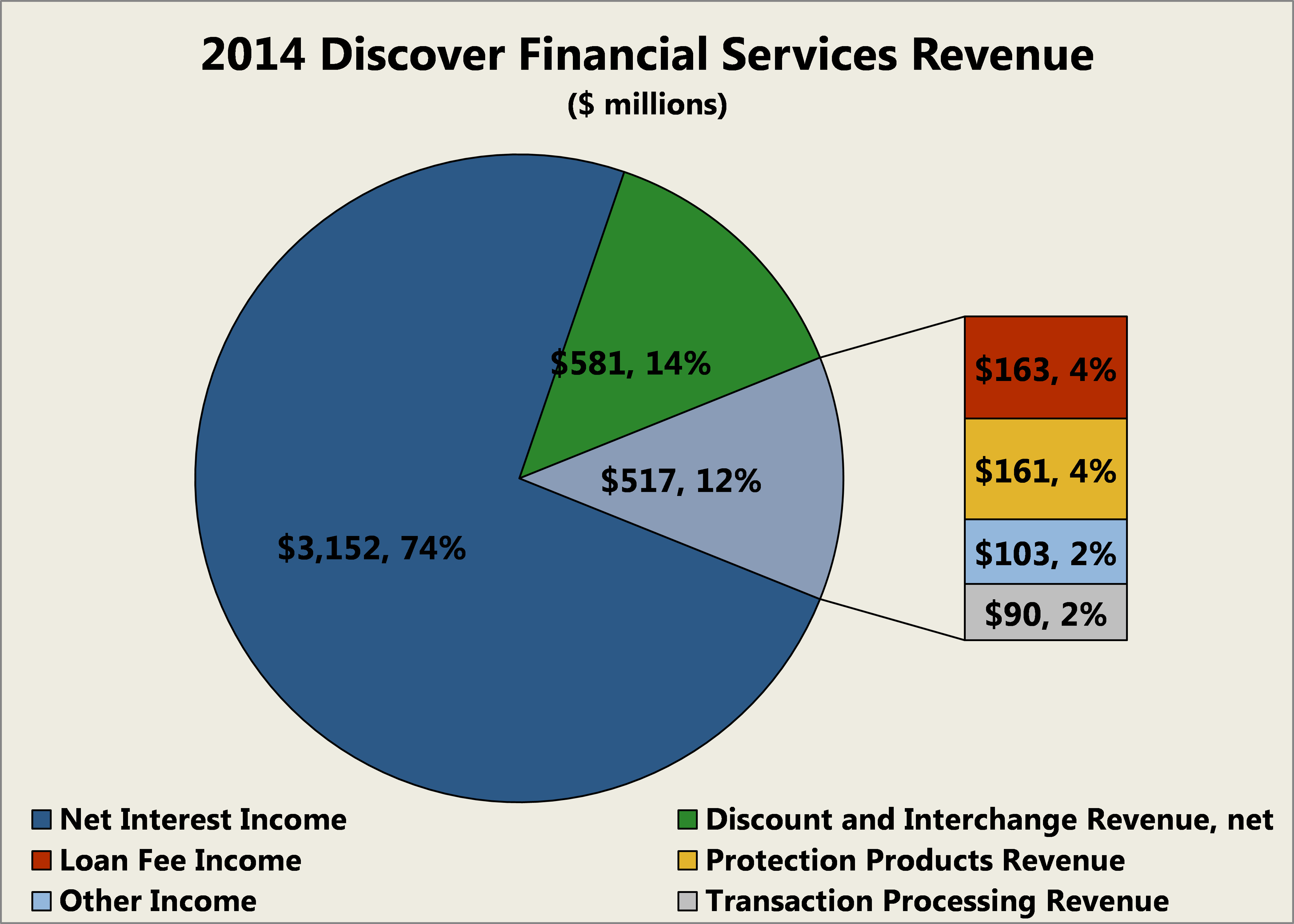

It's important to remember the principal ways banks like Discover make money is through net interest income, which is the difference between what is earned on loans versus what is paid out on deposits and other forms of borrowing. One of the key ways to boost this income is by issuing more loans. And while it may not seem like a company that principally issues credit cards is dependent on net interest income, consider that nearly 75% of the revenue Discover brings in is from this very thing:

Source: Company Investor Relations.

Knowing it is outpacing its peers in loan growth means it should deliver even better results as the years progress. In addition, knowing Discover has less than 15% of loans held by the Community Banking unit (which does include small business) of Wells Fargo (WFC +1.11%) -- $66 billion versus $505 billion -- we are shown how much possible growth may actually await the company.

3. Better relationships are being built

According to CEO David Nelms, "We are achieving increased wallet share with existing customers and adding loans from new accounts, as well."

It's critical to know that, not only is Discover growing its loans, but it's also enhancing the relationships it has with its existing customers. Because the reality is, countless banks have talked about the desire to increase their "wallet share" among their customers by cross-selling various products to them.

While it may not be an exact apples-to-apples comparison, Bank of America once revealed it would earn four times more money from a customer who simply had an account with the bank than one who considered Bank of America as his or her primary bank, and also borrowed money from it. These tighter-knit relationships will only be further opportunities for Discover to grow.

4. The relationships are lasting

CEO Nelms went on to add:

Shifting gears, Discover was recently named the winner of three Call Center Excellence Awards by the International Quality & Productivity Center for demonstrating superior thinking, creativity, and execution across the full spectrum of call center functions. I think this service excellence is one of the reasons why we have some of the lowest customer attrition in the industry.

With all that growth in mind, the natural question becomes, how exactly is Discover doing it? It turns out that one of the key ways is by providing excellent customer service. And, as a result of its award-winning customer service, its customers are committed to it just as much as it is committed to them, as its attrition rate -- the turnover among its customers -- is one of the lowest around.

5. It isn't just marketing

Lastly, according to Nelms:

[W]e've actually been able to focus as much on efficiency and effectiveness to outgrow the industry, not doing it by outspending the industry. And I think what you spend in marketing, maybe it's important, but what your product is, the service that backs it, the rewards program, how good you are at direct marketing, and of course we focus all of our efforts on direct.

At times of such substantial growth, investors can worry that part of the reason behind it stems from aggressive advertising, which may increase top-line results, but ultimately detract from the bottom-line ones. Yet, we must see that Discover is keenly aware of this, too. And its growth hasn't stemmed just from great commercials or good service, but an understanding it must also offer great products. Based on the tangible results we've already explored, it is clearly doing all three.

The Foolish bottom line

At times, conference calls discussing earnings can lack important pieces of insight on how a company is progressing. Yet, that wasn't the case with the most recent one from Discover. And while one conversation shouldn't shift an investment decision, there was very helpful insight that revealed how Discover posted such strong results.