America's energy boom is breaking records and making many investors fabulously rich. Pioneer Natural Resources CEO Scott Sheffield said he believes the best is yet to come, with a potential doubling of U.S. oil production, which has already soared 67% since 2008.

One of the best way for investors to cash in on the new black gold rush is with "pick and shovel" companies that provide necessary materials, components, or services to oil and gas companies. Oil service companies such as Schlumberger (SLB +1.10%) and Halliburton (HAL +0.79%) fit this mold, but investors may be confused as how to choose between these two industry superstars.

This article will explore whether an important investing metric might shed light on which of these companies makes the best investment right now and for the long term.

Return on equity

Return on equity, or ROE, is the measure of how efficiently a company can generate profits from money it receives from investors and is a great way to compare companies in the same industry.

Its basic formula is net income divided by shareholder equity.

According to S&P Capital IQ, the respective ROE for Schlumberger and Halliburton is 16% and 18%. While initially that might appear very similar, it's often worth breaking down this metric into its five components, to make sure that neither company's data is skewed to artificially strengthen ROE.

Return on equity is sometimes used to determine management bonuses, creating an incentive to inflate the metric. There are several ways to accomplish this. For example, by buying back shares, shareholder equity is reduced and ROE increased. Writing down assets is another strategy to accomplish the same goal. Similarly, management can use large amounts of leverage to grow net income, (at least initially) by piling on debt.

To help distinguish well-run companies from those that are unsustainably manipulating their ROEs, DuPont in the 1920s developed a five-factor model to break down ROE into its component parts. This is known as the DuPont Analysis, which I'll now apply to these two oil services titans.

Breaking it down

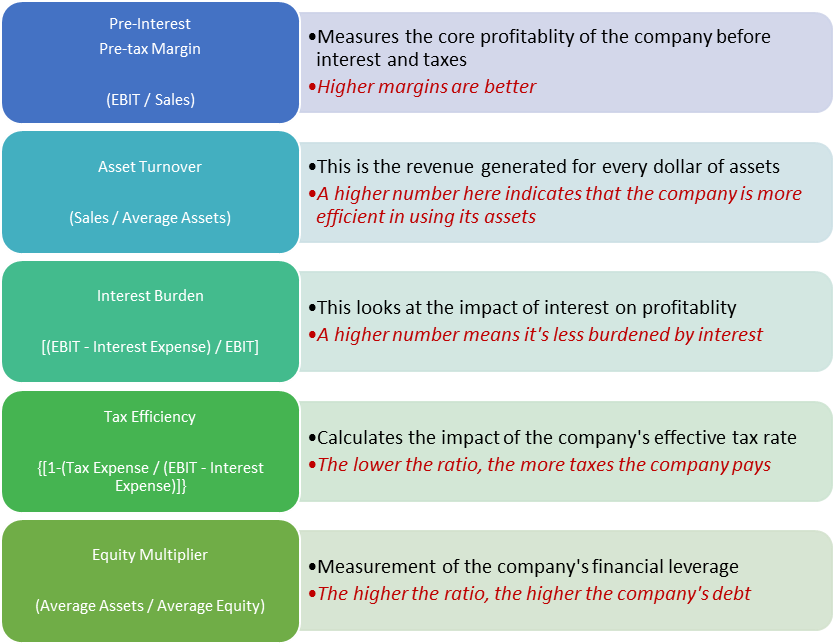

The five components of ROE are: pre-interest pre-tax profit margin, asset turnover, interest burden, tax efficiency, and leverage ratio, aka the equity multiplier.

While these terms might seem intimidating at first they are worth learning about to help better understand companies we invest in over the long-term.

Chart courtesy of Fool colleague Matt DiLallo.

How do Schlumberger and Halliburton compare?

| Company | Operating Margin | Asset Turnover | Interest Burden | Tax Efficiency | Leverage Ratio | ROE |

| Schlumberger | 19% | 0.71 | 0.96 | 0.7695 | 1.69 | 17% |

| Halliburton | 14% | 1.05 | 0.91 | 0.7261 | 1.93 | 19% |

| Industry Average | 12% | 10% |

Sources: S&P Capital IQ, Morningstar.

As we can see from the above table (which is based on financial data from the last 12 months) both companies have better operating margins than the industry as a whole. But Schlumberger is 36% more profitable in its operations than Halliburton and has a gross tax rate of just 23.05%, compared to 28.39% for Halliburton. Schlumberger also only loses 4% of its operating profit to interest, compared to 9% for Halliburton. This is largely because Halliburton is more leveraged with debt than Schlumberger, partially explaining why it has an ROE that's 11.8% higher.

What it means for you

This analysis shows that both Schlumberger and Halliburton are far superior at generating profits from investor cash than their industry peers, and neither is clearly superior to the other. Thus, investors should use other factors to decide between these two companies. There are three reasons why I think Schlumberger is a better buy today.

Why you should buy Schlumberger over Halliburton

| Company | Yield | Historical Operating PE | Current Operating PE | Projected 10 Year Annual EPS Growth Rate | Projected 10 Year Annual Dividend Growth Rate | Projected 10 Year Annual Total Return |

| Schlumberger | 1.50% | 28.6 | 20.4 | 18.50% | 17.52% | 19.02% |

| Halliburton | 0.90% | 19.7 | 18.1 | 22% | 14.17% | 15.07% |

| S&P 500 | 1.87% | 9.20% |

Sources: Fast Graphs, Yahoo! Finance.

Schlumberger is currently 29% undervalued relative to its 21-year average operating P/E ratio, compared to Halliburton's 8% undervaluation. In addition, Schlumberger is a better income stock. Not only does it sport a higher yield, but analysts predict its annual dividend growth over the next decade will surpass Halliburton's by 24%. This is likely to result in 27% better annual total returns.

Foolish takeaway

A DuPont ROE analysis shows no clear winner between Schlumberger and Halliburton. However, due to its higher yield, faster projected dividend growth rate, and larger historical undervaluation, I would recommend investors go with Schlumberger.