Dale Earnhardt Jr. and Drew Brees are two of the faces of the Wrangler brand. Source: VF Corp.

When a company qualifies as a Dividend Aristocrat -- meaning it has not only sustained a dividend for 25 consecutive years, but also increased it every year -- the compounding power of dividends is amazing. Let's take a closer look at the Dividend Aristocrat that is VF Corp (VFC -17.37%), the company behind some of the most popular fashion, sportswear, and outdoor apparel brands in the world.

Is it worthy of your investment dollars today? Let's take a closer look.

The power of the dividend

A quick glance at VF Corp's dividend yield -- currently only 1.5% -- is enough to send many income-seeking investors looking elsewhere. If you're looking for a minimum amount of income for today, this might not be the right stock for your needs. But for long-term investors looking for the long-term wealth-building power of a sustainable dividend, a look at VF Corp's history, its business, and the market-crushing returns it has generated over the past 30 years should keep you from dismissing it out of hand.

Here's how VF Corp stock has performed over the past 30 years, both with and without factoring in the dividend:

That's serious wealth-building power. As you can see, the dividend actually accounts for more than half of the value created over the past 30 years. The biggest driver? Consistent payouts, and regular increases.

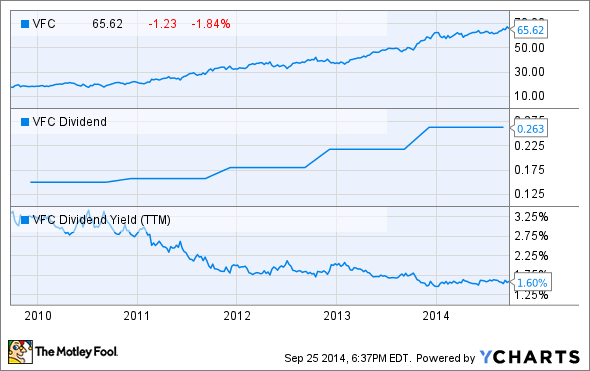

"Wait a minute," I can hear you saying. "I bet the dividend yield was much higher back then than it is today." Not so. VF Corp didn't start paying a dividend until 1985, and at that time, the yield was less than 2%:

VFC Dividend data by YCharts.

The current yield is low, but that's a product of the stock's price increase:

The dividend has increased a whopping 75% over the past five years, but the yield has been cut in half over the same period of time because the stock's price has gone up almost 280%. Before you let the big run-up on the stock scare you away, let's talk about VF Corp's business and the long-term prospects.

Accelerating growth

Too much focus on the stock price appreciation and dividend yield -- things based on what has already happened, doesn't matter if you can't make a solid business case for the future. VF Corp is more than 100 years old, so it's also easy to disregard it as a business that's past its prime. Digging into the core business and the growth potential show that's probably not the case.

Timberland (acquired in 2011) is a major growth driver. Source: VF Corp.

VF Corp is a collection of some of the most established brands in apparel and activewear, including Wrangler and Lee denim, 7 for All Mankind, Nautica, and Kipling. It also owns some of the most popular outdoor and action sports brands, like JanSport, The North Face, Vans, and Timberland. This diverse brand power has helped the company drive annual sales growth of more than 8% over the past five years, and annual earnings-per-share growth closer to 13%.

Timberland is a big part of the company's growth plans, and it is expected to add another $1.5 billion in sales -- more than 10% in top-line growth for VF Corp -- by 2019. That's about double Timberland's 2014 sales.

7 For All Mankind is another brand with staying power and fashion appeal. Source: VF Corp.

Direct to consumer sales is an important part of the company's growth as well. In 2013, this channel -- which includes both e-commerce and sales at the company's 1,200-plus retail and outlet stores -- generated $2.6 billion in revenue in 2013. By 2017, sales are expected to be $4.4 billion, with e-commerce the fastest-growing segment. While 75% of total sales will still be through traditional retail and wholesale partners, direct sales will be a key driver of higher gross margins and net income.

Returning value to shareholders

Management projects that earnings per share will grow at a 13% annual rate over the next five years. Furthermore, they remain committed to continuing to increase the dividend. Here's CEO Eric Wiseman (who has been with the company since 1995), from the second-quarter earnings call:

And actually from a dividend standpoint, in 2014, we'll expect to increase our dividend substantially once again, just as we have over the past couple of years. Likely by more than 20% just like we did last year, moving toward that ultimate goal of a 40% payout [ratio].

The payout ratio -- which measures the percentage of earnings paid in dividends -- is closer to 35% today, so there's certainly room to keep growing the dividend with earnings per share. The easy math is that the dividend will likely increase at around the 13% rate that EPS is expected to grow.

Is VF Corp a buy today?

I'm not going to argue that it's not a "pricey" stock. A price-to-earnings ratio of 23, and price-to-sales ratio of 2.3 are both above the company's historical multiples. Here's some "quick and dirty" math.

Assuming (risky, I know) that the company achieves its earnings goals by 2017, and that Mr. Market continues to pay a 23 P/E multiple, the stock would be worth around $103 per share in 2017. P/E multiple of 15 (a lowball valuation) would put the share price where it is today. Splitting the difference with a P/E of 18 -- probably closer to where it "should" be -- would give us a 2017 share price of $88, worth about 8% in annualized growth from today's share price.

These (rough) estimates don't include any value from the dividend. If management is able to increase it at 13% per year, the dividend will be almost 50% higher in 2017 than it is today.

One could also argue that today's VF Corp is a more focused and growth-oriented company than in the past. The value of its diverse brands, and the company's ability to grow sales of those brands both in the U.S. and internationally, is unparalleled today. The potential "normalization" of its valuation does add some risk, but this is a high-quality business with a relatively straightforward path to reaching its growth targets. Better to pay a premium for a great business than pay anything at all for a poor one.