Until last week, it had been three years since United Parcel Service (UPS +0.60%) last had an investor conference, and much had changed with its end-market conditions in the interim. At the recent conference, management updated UPS investors on its long-term outlook and on how it is adjusting to these changes. With this in mind, it's time to look at what is new with UPS and what it might mean to the shipping and logistics company's investors.

United Parcel Service's end-market trends

Before getting into details, here is a chart of UPS' trailing-four-quarters segmental income so Fools can see the relative importance of each business.

Source: United Parcel Service Presentations.

Since 2011, there have been three separate and somewhat unexpected changes in end markets for UPS and its main rival, FedEx.

-

Global growth -- and trade growth in particular -- didn't work out as strong as management had expected in 2011 (mainly affecting international packages).

-

Stronger relative growth in nonpreferred (i.e., slower and lower-yielding) deliveries such as ground-based business to consumer, or B2C, over preferred deliveries.

-

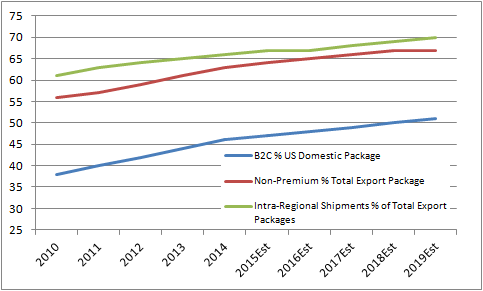

Stronger relative growth in e-commerce B2C deliveries, which tend to have lower yields and therefore pressure margins (mainly impacting U.S. domestic packages).

These three trends are expected to intensify in future years, as shown in the following chart of management's forecasts:

Source: United Parcel Service Presentations.

Clearly, management needed to address its responses to these developments, because there are fears UPS is facing structural pressures.

How United Parcel Service management is responding

First, the good news is that there are signs that global trade growth is set to quicken in the next few years -- this should aid growth in UPS' international segment. Moreover, intraregional shipments are forecast to grow faster than intercontinental shipments (see chart above); according to CFO Kurt Kuehn, this development could be favorable to the company's return on invested capital, or ROIC.

In his presentation, Kuehn said intraregional shipments only generate one-third of the per-package revenue that intercontinental generates. However, the capital required to deliver an intraregional package is one-eighth of the figure for an intercontinental parcel, and revenue per invested capital is $2.50 versus $1 for intercontinental packages. CEO David Abney added that UPS plans to invest $1 billion in expanding ground capacity in Europe through the next five years.

Second, ROIC considerations also figured in the discussion of growth in nonpremium packages relative to premium. Kuehn said nonpremium packages only yield 42% of premium, but its ground and UPS SurePost (a ground-based, economy, residential service that typically uses the U.S. Postal Service for final delivery) services respectively require five times and 10 times less capital than its premium Next Day Air delivery service.

Third, management highlighted its initiatives in generating operational improvements in its U.S. domestic package segment. Abney noted that only 40% of company drivers are currently using UPS ORION, a proprietary software system that optimizes driver delivery routes and is already cutting seven to eight miles off daily routes per driver. When it's fully implemented in 2017, Abney said he believes the system will generate $300 million to $400 million in combined cost reductions, making ORION key to UPS' forecast for operating profit in the U.S. domestic package segment to increase from $4.7 billion in 2014 to $7 billion-$7.6 billion in 2019.

In addition, management reiterated its expectation that a combination of planned price increases and the shift to dimensional-weight pricing for all U.S. packages would result in higher yields per package. Interested Fools can read more about UPS' pricing plans here. Incidentally, FedEx is making similar changes to its pricing.

United Parcel Service investor conference: The numbers

The expected result of these factors can be seen in the forecasts given at the conference, whereby each segment is expected to improve near- and long-term operating margin.

| Segment | Revenue Growth (%) 2015 | Operating Profit Growth (%) 2015 | Revenue Growth (%) 2015-2019 | Operating Profit Growth (%) 2015-2019 |

|---|---|---|---|---|

| U.S. Domestic | 5-6 | 9-11 | 5-6 | 8-10 |

| International | 6-7 | 9-11 | 6-9 | 9-12 |

| Supply Chain & Freight | 4-5 | 10-12 | 5-7 | 10-12 |

| Total | 5-6 | 9-11 | 5-7 | 8-11 |

Source: United Parcel Service Presentations.

UPS' ROIC forecast of 25%-30% for 2015-2019 demonstrates that its impressive recent record of capital efficiency is likely to continue. Furthermore, with capital expenditures forecast to be just 4.5%-5% of revenue in 2015-2019, compared to a range of about 5%-8% in the 10 years before the last recession, UPS is likely to continue to generate strong free cash flow in the future.

All told, this was a positive update on long-term prospects at UPS. Observant Fools will note that its forecast for 9%-13% earnings-per-share growth in 2015-2019 is lower than the 10%-15% projection from 2011. This is largely a consequence of the headwinds discussed in the first section of this article.

The key is to focus on where UPS is headed: A combination of high ROIC, relatively low capital expenditures, margin expansion, pricing initiatives, and productivity improvements makes the company attractive. I will turn to valuation matters in a future article, but it's a thumbs-up for the investor conference. Now the company needs to deliver.