2014 has been a brutal time for investors in offshore oil drillers like Transocean (RIG +0.26%), Seadrill (SDRL +0.00%), Ensco (ESV +0.00%), Noble (NE +0.00%), and Diamond Offshore (DO +0.00%).

Recently I explained why I think now is the time for long-term investors to snap up shares of these undervalued companies. However, it's important for investors to realize that despite these dramatic stock price declines there are still risks that could cause shares in offshore drillers to plunge even further. Let's take a look at what these risks are and how they could further impact these offshore drillers.

Dividend cuts

On Nov. 26, Seadrill shocked investors by suspending its generous dividend -- which had been yielding close to 20% -- for which the company is now facing a class action lawsuit. Other offshore drillers might not be too far behind.

| Company | Yield | EBITDA Payout Ratio |

| Transocean | 15.7% | 122% |

| Seadrill | 0% | na |

| Ensco | 9.6% | 44% |

| Noble | 8.5% | 16% |

| Diamond Offshore | 1.3% | 7% |

| Industry Average | 8.1% | |

| S&P 500 | 1.85% |

As this tables shows, Transocean's dividend is already verging on the unsustainable as the forward payout is larger than its earnings before interest, taxes, depreciation, and amortization, or EBITDA, the company reported in the last 12 months. Ensco and Noble's payouts seem much safer in comparison. Yet even these companies face steep contract cliffs over the next two years.

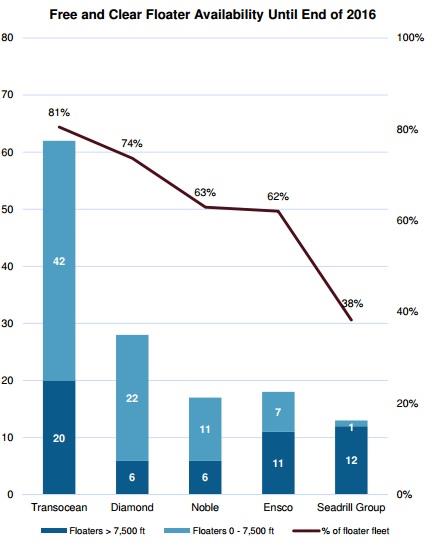

Specifically, 62% and 63% of their respective ultra-deepwater fleets -- the most profitable in the industry -- are currently uncontracted past 2015, as seen in the chart below. This means that, should oil prices remain low through 2016 and demand for offshore drilling falls even further, day rates might plunge even lower as a glut of rigs battle to find work. This in turn might force Ensco and Noble to cut or potentially suspend their dividends as well.

In addition, last quarter, Transocean was forced to write down $2.8 billion due to the declining value of its aging fleet which resulted in a $2.22 billion loss. Recently, Transocean announced it would scrap an additional seven of its aging lower-specification rigs, which will result in an additional $100 million to $140 million in write down losses this coming quarter.

Not only will this additional write down further weaken the company's dividend sustainability, but it might indicate that the company's previous plan to spin off several of its older North Sea rigs into a separate company, called Caledonia, may never be achievable. Transocean announced it was putting on hold the Caledonia IPO due to weak market conditions, but eventually hoped to monetize the rigs. The company's scrapping of 11 older rigs so far this year is a possible indication that market conditions have deteriorated to the point that these older, lower-specifications rigs, may prove to be worthless. If that turns out to be the case, then Transocean investors need to prepare for additional rig scrappings and write downs in future quarters, which might threaten the dividend all the more.

Large debt loads and rising interest rates

| Company | Total Debt ($Billion) | Interest Coverage Ratio |

| Transocean | 10.36 | -0.56 |

| Seadrill | 14.14 | 9.54 |

| Ensco | 5.96 | 6.29 |

| Noble | 4.74 | 9.03 |

| Diamond Offshore | 2.24 | 11.19 |

One large threat to the dividend sustainability of offshore drillers is large debt loads and rising interest rates. Not only is the Federal Reserve expected to start raising interest rates by mid-2015, but energy companies may soon find themselves in a credit crunch.

This is because crashing oil prices have resulted in soaring interest rates for energy junk bonds as investors fear overleveraged energy firms will be forced to default. Deutsche Bank estimates that the market is currently pricing in a 30% default rate on $90 billion in junk bonds sold over the last few years, mainly to shale oil and gas explorations companies.

In fact if oil were to remain at $65 for three years, JPMorgan estimates that as many as 40% of these junk bonds could default.

While none of these offshore drillers' bonds are in imminent danger of default, spreading fear among energy bond investors could wind up affecting their ability to service their debts in the future.

According to Larry McDonald, head of U.S strategy at Newedge USA's macro group, such fears could very well result in a credit crisis for the energy industry. With large debt needing to be rolled over and growing fear among debt investors, companies like Transocean, whose operating income already fails to cover its interest payments, might find new loans much harder to come by and only at much steeper interest rates.

That might not only threaten its dividend, but also force the company to potentially sell assets at fire sale prices to service debts.

Please note that while I accept these dire predictions as possible worst-case scenarios, I don't think that some of these analysts' predictions are likely to come to pass.

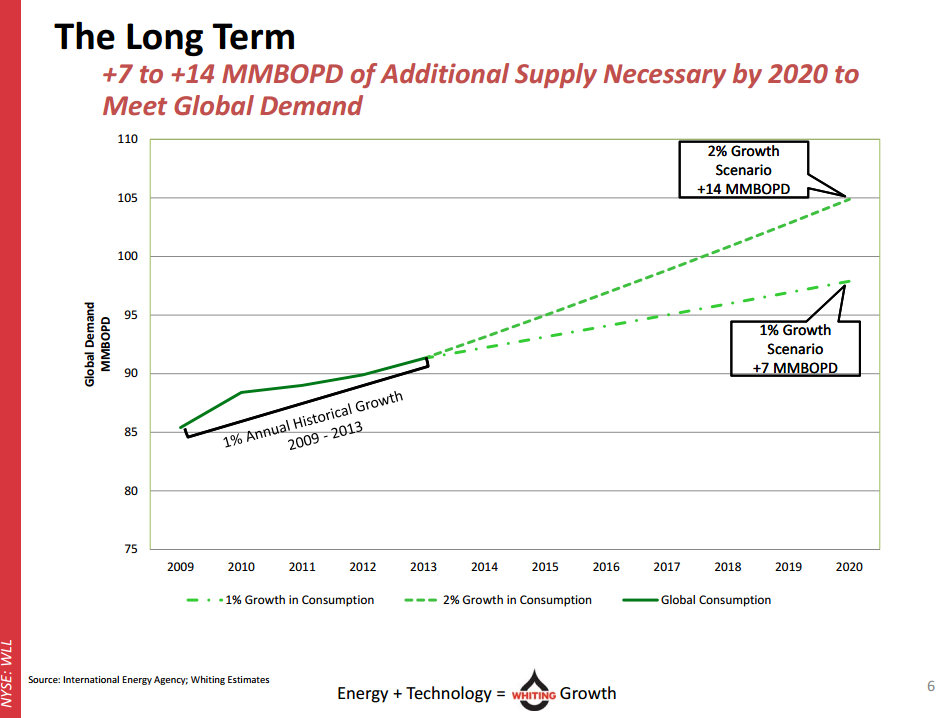

For example, certain claims that oil prices will remain at $65 for the next five years is largely predicated on the assumption that Chinese economic growth (and thus oil demand) will all but stop growing due to overinvestment in that nation's industrial base and the need for China to digest its new assets. While true that China's economic growth has slowed in recent months, I doubt its economy is about to slip into a recession. While oil demand from China and other developing nations like India may slow over the next year, global demand for oil is still likely to rise over time -- as the below image illustrates -- and lead to higher long-term oil prices than many oil bears are now predicting.

Source: Whiting Petroleum Investor presentation.

Contract cancellations due to long-term low oil prices

Both of the above risks represent scenarios predicated upon oil prices potentially falling further and remaining low for the next couple of years. While I don't believe this will be the case, there are some experts who do.

For example, Andy Xie, the former chief economist for Morgan Stanley and the IMF, believes that oil might decline as low as $43 per barrel and average $65 per barrel through 2019. Such opinions are potentially supported by comments from Ali al-Naimi, Saudi Arabia's oil minister, who recently told the Middle East Economic Survey that Saudi Arabia would not budge from its current position of maintaining production, even if oil prices declined to $20. In fact Mr. al-Naimi even said that his government thinks that oil may never hit $100 per barrel again and that the kingdom was considering actually raising production to offset his government's recent plunging revenue.

With such oil price declines, coupled with the prospect of prices remaining low for several years, not even the existing contracts offshore drillers have are safe.

For example, on Nov. 21, Statoil, (STO 3.00%) Norway's largest oil company, cancelled its fifth offshore drilling contract, which cost the company $350 million in cancellation fees, due to declining economics of deepwater drilling.

Since then oil prices have declined another 20% -- increasing the risk that other companies may soon join Statoil in cancelling existing drilling contracts. Even if they don't, the fact is that offshore drilling, especially the ultra-deepwater variety, is one of the more expensive ways to obtain oil. Reuters estimates that drilling in the North Sea, where Statoil is dominant, has a breakeven oil price of $46 per barrel to $53 per barrel, while worldwide deepwater offshore drilling requires $54 per barrel to $60 per barrel.

With major oil companies announcing major spending cuts over the next year, there is a chance that even new, state-of-the-art rigs, might not be able to find work if the price of crude falls any lower and remains at those levels over a prolonged period of time. That worst-case scenario could prove disastrous for heavily indebted Transocean and Seadrill, who have several new (and very expensive) rigs scheduled to be delivered over the next few years. For example, Seadrill has 18 rigs scheduled to be delivered over the next three years at a remaining cost of over $5 billion.

These companies face the prospect of having to pay billions of dollars to take delivery of new rigs when deepwater offshore drilling may not be economically viable.

Bottom line: Markets can remain irrational longer than you can remain solvent (or sane)

While shares of offshore oil drillers are now trading at very appealing valuations and offering potentially mouth-watering yields, it's important for current and potential investors to be aware of the risks and scenarios that may befall the industry. Rising interest costs, slashed dividends, contract cancellations, and continued falling day rates are all possible. Buying at today's low prices and sky-high yields may very well prove to be greatly profitable if you have the courage to ride out a potentially long decline in the industry cycle. However, be aware of your risk tolerances and allocate your position sizes accordingly as part of a diversified income portfolio.

And if you are considering using cheap margin to supercharge your potential gains, remember the words of famed economist John Maynard Keynes: "Markets can remain irrational longer than you can remain solvent."