I'm not going to lie. As a shareholder of Linn Energy (LINE +0.00%), I was really hoping the company wouldn't need to cut its distribution this year. Based on its hedging position, it looked like its financial obligations for the year would be tight, but could be done without a cut. I guess I was just the King of Wishful Thinking, though, because recently, the company decided to cut its distribution by 56% for both it and its holding company LinnCo (NASDAQ: LNCO).

Yeah, it hurt, but like a disappointed kid who hears the words "we can't afford it," I can begrudgingly accept the decision because it is best for the long-term health of the company. Let's take a look at why this move makes sense even though some investors, like myself, will accept the decision kicking and screaming.

Linn's distribution cut may hurt some investors way more than others

One thing many people will say to Linn Energy investors is "Hey, even with the distribution cut, the company still yields greater than 10.8%. What's there to cry about?" This is a common mistake many people make when looking at dividend stocks. Everyone who buys a stock that pays a dividend -- or distribution in the case of an MLP -- has their own cost-based yield. This yield is the current dividend divided by the price at which an investor bought shares in a company, which can change over time if those dividends increase, or if they are reinvested to buy new shares.

In the case of Linn, even though today's yield with the distribution cut is 10.8%, an investor who bought shares as recently as six months ago, when shares were more than $30, would have a much more paltry yield of 3.8%. So yeah, for us investors in Linn, the distribution cut may be a much bigger hit than what today's yield might suggest. If there is anything you take away from this article, it should be that you should know the cost-based yield of your investments so you can make better decisions.

I'll get over you (fat distribution checks), I know I will

As we all waive goodbye to those sizable distribution checks, it's slightly reassuring to know the moves Linn Energy is making are to set the company up for two things:

- To be well positioned to grow the distribution when oil and gas prices rebound.

- To prepare the company for a much longer period of lower oil prices than many energy investors care to think about.

With the dividend cut announcement, Linn also announced it would be spending only $730 million on capital expenditures -- less than half of the $1.55 billion it spent in 2014. While a small part of this reduction in capital spending is related to the sale of its more capital-intense Granite Wash assets, it also focuses much more on maintaining production at existing oil wells and drilling new gas wells in some of its lowest-decline regions instead of expanding oil production. The combination of the distribution cut and lower capital expenditures mean Linn's financial obligations will be about $1.36 billion less than last year.

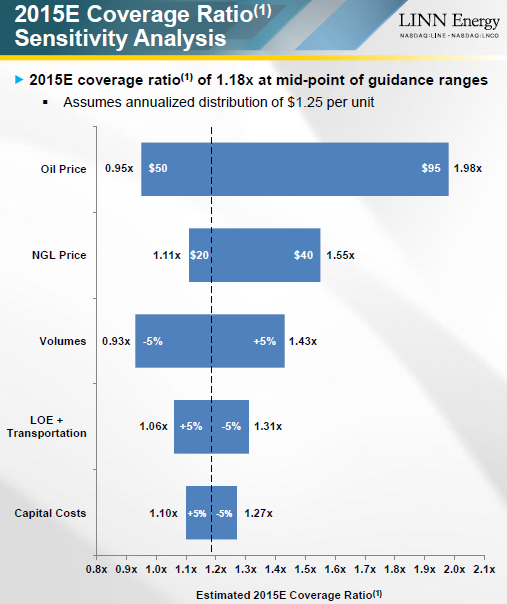

Based on this guidance and its current hedging position, Linn's management anticipates that its distribution coverage ratio will be about 1.18 times for 2015, and it should be able to stay close to a coverage ratio of 1 even if the average realized price for its unhedged oil position for the year is around $50.

Source: Linn Energy Investor Presentation.

Also, with 100% of its anticipated natural gas production now hedged all the way out to the end of 2017, there is one less variable investors need to fret about since that essentially locks in gas prices -- and may suggest that management anticipates a weaker natural gas environment in the coming years.

What a Fool believes

As much as this distribution cut may kill the cost-based yield for those invested in Linn, it shows that management is willing to act in anticipation of rougher times ahead rather than trying to push through and potentially get itself in trouble with too many financial obligations. I may not like the decision right now, but it looks like Linn is giving shareholders a dose of medicine we will all need to get through this dip in oil prices, which we may thank it for later.