Home Depot (HD +0.72%) shares climbed a wall of worry in 2014. Through weak consumer spending, a soft housing market, and then a massive credit card data breach, the stock still managed to jump 30% and finish the year as the third best performer in the Dow Jones index.

But the rally might not be done yet. Here are a few reasons why I think Home Depot shares could keep rising in 2015.

Online business

Revenue growth at Home Depot stores has been impressive lately, with comparable store sales up 6% in the third quarter. Notably, those sales gains weren't tied to just higher prices: customer traffic, average spending per customer, and sales per square foot all logged solid gains through the first three quarters of the year.

But what many investors might not realize is the sheer scale of Home Depot's bet on e-commerce as fuel for more gains down the line. Online orders improved 40% in the third quarter, lapping a 50% pop in the prior year. Here's how CEO Frank Blake described the online investment in last quarter's conference call.

We recently opened our first of three new direct fulfillment centers. Each facility will have capacity to hold as many as 100,000 [products] for direct ship to customers. We already have the convenience of 2,000 locations throughout the country for buying online and returning or picking up in store. These facilities will now expand our capabilities to ship most orders the same day they are received.

Attacking the online market, Home Depot expects to broaden its delivery channel to reach 90% of the U.S. population within 48 hours with two more fulfillment centers set to open in 2015.

Market expansion

Meanwhile, there's still plenty of room for growth in the market for home improvement spending. Sure, the housing market could turn in another soft year in 2015. But private residential fixed investment (spending on homes) as a percent of GDP was just 3.2% in the third quarter, which is well below the long-term average of nearly 5%.

Source: Federal Reserve Economic Data

On an absolute basis, spending on that category has grown to almost $600 billion from the housing crisis bottom of $350 billion. But it is still far below the peak $900 billion. That should give investors confidence that Home Depot's main market has room to continue recovering.

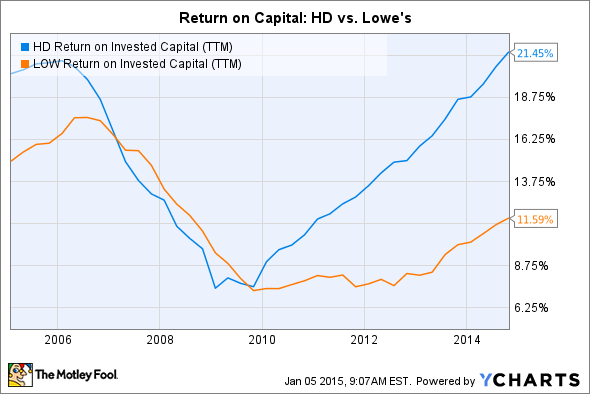

Financial efficiency

Finally, Home Depot's financial power should make major gains this year. Return on invested capital has tripled since bottoming out in 2009 -- reaching 21% in the third quarter.

Those gains look even better in the context of its competition. Smaller rival Lowe's, for example, has an ROIC only of about half Home Depot's.

HD Return on Invested Capital (TTM) data by YCharts

That's just the start though, as Blake and his team expect to hit an ROIC of 27% by the end of this year. That financial strength will give management plenty of ammunition to plow billions of dollars into share repurchases, which totaled over $7 billion in 2014 and gave a big boost to per share earnings growth.

Investors can also look forward to a fast-growing quarterly dividend as a result. The payout jumped higher by 21% last year to a $0.47 per share. And since Home Depot executives have a policy of allocating 50% of earnings to dividend payments, you can count on that dividend to increase at the same heady pace as profit growth.