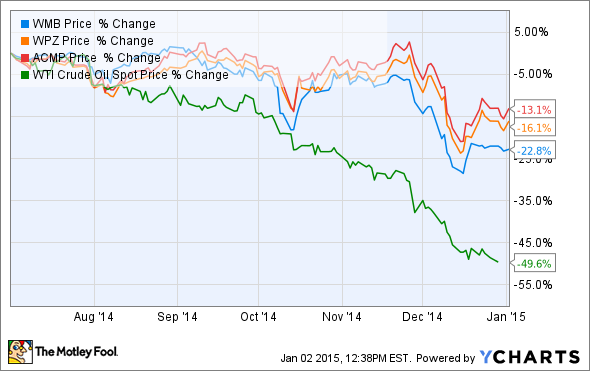

The worst oil-price crash since the financial crisis has taken a toll on nearly all energy stocks -- even those with limited direct exposure to oil prices such as Williams Companies (WMB -0.21%), and its MLPs, Williams Partners (NYSE: WPZ) and Access Midstream Partners (NYSE: ACMP).

While there are short- to medium-term risks that could cause these pipeline providers to crash, there are also three long-term reasons that I continue to believe that Williams Companies and Access Midstream, which will soon be merged with Williams Partners, remain some of the best income growth opportunities available today.

Natural gas production is undergoing a super cycle because of low-cost production and efficiency gains

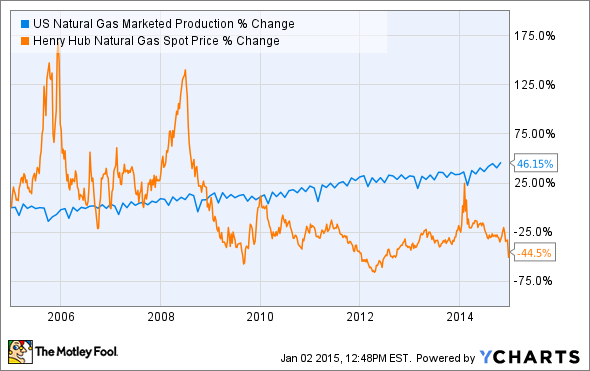

My long-term bullish case for Williams Companies and Access Midstream Partners is predicated on the belief that natural gas production will continue to boom as it has for years. It has done during the last decade, despite the crash in natural gas prices.

U.S. Natural Gas Marketed Production data by YCharts.

This seemingly contradictory miracle has been made possible in part by extremely low-cost production from the hyper-prolific Marcellus and Utica shale formations, as well as improved fracking techniques that allow drilling rigs to produce far more gas than in the past. In fact, the amount of gas production per rig in these formations during the last eight years has increased by approximately sixteenfold and fortyfold, respectively.

Source: EIA Drilling Productivity Report.

This increased productivity is partially why the EIA projects U.S. gas production to continue to boom through 2040.

Williams is betting huge on electrical generation switching from coal to natural gas

Source: Williams Companies Investor presentation.

As this image shows, Williams Companies is planning to invest $4.5 billion into its Transco pipeline system, which currently links gas production from Texas to key markets in the Southeast, such as Florida, as well as along the entire Eastern Seaboard all the way to New York City. The current system consists of 10,200 miles of pipeline and 56 compressor stations with a daily capacity of 10.2 billion cubic feet per day of gas.

To put that in perspective, this single pipeline system currently carries 14% of all U.S. gas production. The $4.5 billion that Williams is planning on spending to expand this pipeline system represents just 15% of its $30 billion current and potential backlog of growth projects that it plans to construct between 2014 and 2019.

Additional key projects include the Transco Appalachian Connector, which will link the Transco system with gas-gathering systems in the Marcellus and Utica formations. This project is expected to be fully operational in late 2018, and have a capacity of 2 billion cubic feet/day of gas. Management has already seen strong interest in long-term fixed-rate contracts from gas producers in the region.

Another key Marcellus/Utica investment is the Atlantic Sunrise pipeline system, which will connect the Northern regions of the Marcellus and Utica region with Williams' existing pipeline systems. The $2 billion project already has 1.7 billion cubic feet/day of gas commitments locked up under 15-year contracts, and is scheduled to be complete by mid-2017.

What's the reason for Williams' optimism that the eastern U.S. will need all this gas? Simply put, the EIA estimates that the majority of new power plants over the next quarter century will use cleaner, cheaper natural gas as their source of fuel.

Source: EIA 2014 Annual Energy Outlook

However, Williams Companies' growth prospects aren't just limited to natural gas for power generation purposes. It's also diversifying into other profitable growth areas.

Growth opportunities in Canadian propylene, and exports to Asia

Williams Companies is currently considering cashing in on the distressed Canadian propane market by constructing a large propane dehydrogenation plant in Alberta that would produce 1.1 billion pounds of valuable propylene from cheap propane. This could then be sold to local industries that use propylene to make various plastics and foams, or sent to West Coast export terminals for export to Asia. Williams is already investing heavily in the Pacific Northwest in terms of additional gas pipelines that would serve West Coast export facilities specializing in everything from liquefied natural gas, or LNG, to methanol and fertilizer.

Source: Williams Companies Investor presentation.

Bottom line: Williams Companies' and Access Midstream's long-term prospects remain bright

While there are several short-term risks to Williams Companies and Access Midstream, including the potential for project cancellations and a credit crisis in the energy sector, I remain bullish on these long-term income growth investments. Williams's size and scale allows it to tap cheap credit markets and invest in a massive portfolio of diversified current and potential growth projects. This has led management to guide for 10%-12% distribution growth, and 15% dividend growth, through 2017 for Access Midstream and Williams Companies, respectively.

With a quarter century gas super cycle as a growth catalyst, I think it's possible for Williams and Access Midstream to not only achieve those income growth targets, but perhaps to continue growing their payouts at similar rates for many years to come.