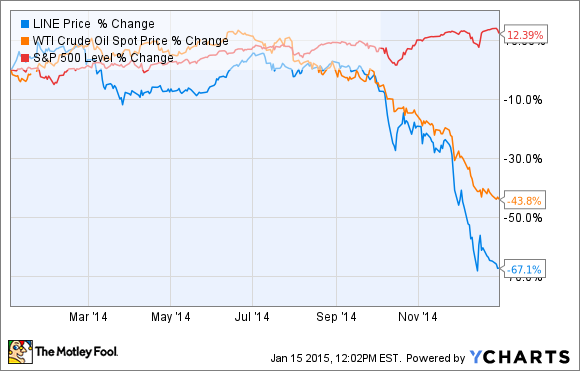

When you are an oil and gas producer like Linn Energy (LINEQ), you live by the price of oil, and you die by the price of oil. In 2014, unfortunately, it was a lot more of the latter.

With the price of domestic crude falling close to half of what is was at the beginning of the year, shares of Linn and its holding company LinnCo (NASDAQ: LNCO) were bound to take a pounding. However, the even bigger reason that Linn took the haircut that it did was more related to what investors were predicting it would do -- cut its distribution.

A little too much to handle

Thanks to a pretty decent oil hedging policy at Linn, it was able to secure very favorable contracts for the oil and gas it plans to sell in both 2015 and 2016, as seen in the chart below.

Source: LINN Energy Investor Presentation.

Even with 100% of its natural gas sales and 60% of its oil sales hedged, that 40% or so of unhedged oil left enough uncertainty that Linn was at risk of not being able to cover its hefty distribution payments. Since it is a master limited partnership and its cash situation was already tight because of interest payments, investors were very nervous that the distribution would be cut to keep its distribution coverage ratio intact.

A critic of the company might say that the company should have locked in more hedges and futures contracts for its oil production since it runs such a tight budget, but there were very few people making those critiques back in January when the price of oil was north of $110 and Linn was selling its oil at essentially a $20 discount to market price.

What now?

Well, just as 2015 started, Linn's management did exactly what investors were pricing in with that massive plunge. In anticipation of a rough oil price for at least the year to come and potentially longer, management cut the distribution by more than half. In fact, the cut was so deep that the anticipated budget this year should have a distribution coverage ratio of 1.18, which gives the company a little wiggle room in the event that oil prices for the year stay below its forecast price of $60 for all of 2015.

Source: Linn Energy Investor Presentation.

Another clever move that the company made with its much smaller 2015 capital expenditure budget and its slashed dividend is it entered into a $500 million joint venture agreement with The Blackstone Group (BX). Blackstone will cover all of the drilling expenses on some of Linn's acreage in exchange for an 85% working interest in the well until it reaches a certain rate of return, at which point 95% of the working interest in the well will be handed back to Linn. This will help to significantly reduce the drilling risk on some of Linn's undeveloped acreage without having to completely abandon the position for already producing assets.

What a Fool believes

Nobody seems to know what will happen to the price of oil in the near term, and the moves that Linn has made so far in 2015 are a clear sign that it doesn't, either. But, it wants to be ready for just about anything.

The better than $100 price of oil for close to three years lulled many American producers to sleep, thinking that oil prices would remain high in perpetuity. Hindsight tells us that was really dumb. Hopefully, this swift kick in the pants from oil prices will force companies like Linn to take even more conservative hedging policies in the future, because we never know when an event like this may happen again.