Growth stocks can lead to significant gains for investors who pick them well, but they often carry significant risk. The market usually prices years of growth into a stock, and if the company slips, the downside can be huge.

We asked three Motley Fool contributors which growth stocks they think are currently too risky to buy, and you may be surprised to find some of the most beloved companies in the world among them.

Travis Hoium (Amazon): Over the last decade, Amazon.com (AMZN 0.30%) has become a household name with the high growth of its online retail business. Over that same time, the stock has soared. But net income has consistently eluded the company, and the market is demanding bottom-line improvement for the stock to keep moving higher.

AMZN Revenue (TTM) data by YCharts.

There are a number of reasons Amazon and its long-term ability to generate profit is in question. First, online retail has finally become a focus of retail giants like Walmart and Target, who are now offering better selection, lower prices, and free shipping, just like Amazon. They also have physical locations to augment their online presence, which could be an advantage for shipping times, inventory, and more.

Another reason to be worried about long-term growth: cash flow. Fellow Fool, Timothy Green, recently highlighted how in the last few years, Amazon has been using capital leases to hide capital expenditures. If included, the company would actually be cash flow negative.

Amazon is a high-risk stock to avoid, because the company will need to see material profits at some point to sustain its nearly $150 billion market cap. At the end of the day, with competition growing, I seriously doubt Amazon will have the ability to produce the profits that many investors are holding out for. When that realization sinks in, so will the stock.

Anders Bylund (Facebook): The leading social network has over a billion active users across the globe, is monetizing this audience to the tune of $3.2 billion in trailing revenue, and is increasing its bottom-line profits even faster. As a result, Facebook (META 0.21%) stock has seen a fantastic 34% rise over the last year and has tripled since hitting lows in July of 2013.

This is all great news for Facebook shareholders, and I wish them all the luck in the world. Unfortunately, they'll need it.

You may "like" Facebook's app, but that doesn't make it a buy in your portfolio.

I can think of no market more prone to drastic sea changes than the social media industry. Here today, gone tomorrow -- it happens quickly and often. Do you remember MySpace and Friendster? How about Orkut or Bebo? All of these were fantastically successful social networks in their chosen niches. In the case of MySpace, it was the online hangout spot 10 years ago.

Today, they are largely forgotten. MySpace is now Justin Timberlake's playground for next-generation music publishing. The other three are dead and gone.

The first sign of impending doom is when the younger generation turns to the next big thing. Facebook wised up early and bought Instagram for a cool $1 billion in 2012, and the photo-sharing service is already shaping up to be Facebook's replacement. But one of the big draws of Instagram is that it isn't nearly as festooned in advertising as Facebook has become. Facebook may live to fight another day when its platform loses popularity, but the business model will be much different and less profitable.

The risk of systemic failure is real, it's huge, and it's keeping me far away from Facebook stock.

Alex Planes (Tesla): It's a good thing that the "motley" part of our brand encourages differing opinions, because my choice of Tesla Motors (TSLA 2.35%) completes our trifecta of active Fool recommendations. I agree with both Travis and Joe's choices, but I think Tesla deserves a special place in the pantheon of unrealistic investor expectations.

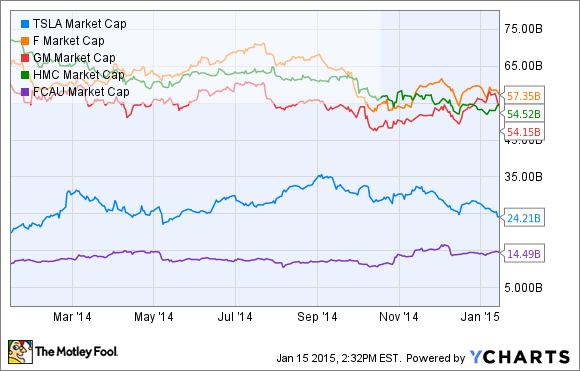

Let's start with Tesla's valuation in comparison to its peers. Bulls will do everything they can to blow past this concern, pointing out that growth stocks demand higher multiples. But the reality of the situation is that Tesla -- which has yet to report any GAAP profitability or positive free cash flow on a trailing 12-month basis -- currently boasts almost half the market cap of much larger automakers Ford, General Motors, and Honda. Tesla is worth roughly $10 billion more than Fiat Chrysler.

TSLA Market Cap data by YCharts

Tesla remains tight-lipped on its sales figures, but what we do know is that the company aimed to sell 35,000 vehicles last year. For its peer group, that might be a good year from a handful of dealerships -- GM sold 9.9 million vehicles around the world in 2014, while Ford sold 2.5 million in the U.S. alone. Fiat Chrysler sold 193,000 vehicles in the U.S. just for the month of December, or roughly five and a half times Tesla's expected global sales for the entire year. And the kicker: All but one of these major automakers made more in profit over the past four reported quarters than Tesla has earned in total revenue.

TSLA Net Income (TTM) data by YCharts.

Simply put, buying into Tesla stock today expecting big growth tomorrow is to buy into the belief that a company with a tiny fraction of competitors' sales will essentially become the largest automaker in the world. That's the only scenario in which calling Tesla a "growth" stock at its present valuation makes any sense. Since that won't happen any time soon, we can either expect the market to remain frothingly irrational about Tesla for years, or we can expect its shares to drop to a more sensible price.