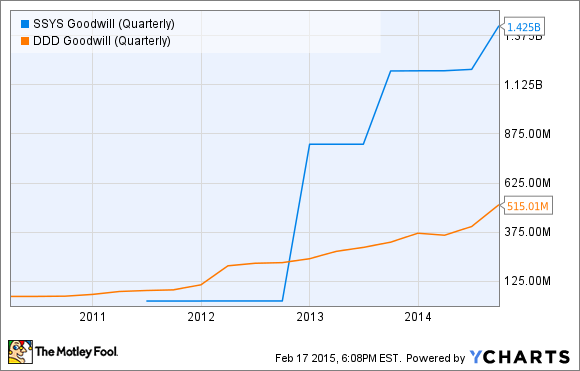

Although 3D Systems (DDD -2.11%) has gained a reputation of being a serial acquirer that's taken a "shotgun" approach to its market opportunity, it has amassed significantly less goodwill on its balance sheet than Stratasys (SSYS -2.89%), which has taken a more focused approach to its acquisition strategy, albeit on a much larger scale:

SSYS Goodwill (Quarterly) data by YCharts.

With Stratasys now expecting to take a significant goodwill impairment charge of $100 million to $110 million against its fourth-quarter earnings due to the recent underperformance of its MakerBot unit, it raises the question of whether Stratasys' balance sheet is at greater risk of future impairment charges than 3D Systems'.

Goodwill impairment 101

Whenever a company makes an acquisition, the premium it pays for a business over its verifiable value is carried on the balance sheet as goodwill. Each year, a company that's acquired goodwill must test it for impairment, and if that goodwill asset is determined to be worth less than the value it's being carried for on the balance sheet, it must take a non-cash impairment charge against its earnings.

Although goodwill doesn't necessarily affect the cash position of a company, it suggests that management may have made a misjudgment around an acquisition in terms of the price it paid or the acquired company's full potential. In other words, goodwill impairments can raise questions about management's ability to execute and create long-term value for shareholders with acquisitions.

Considering that both 3D Systems and Stratasys have used acquisitions as a tool to bolster their respective businesses in recent years, during a period when 3D printing stocks were trading at historically rich valuations, both companies could be at risk of future goodwill impairment. Figuring out which company is more at risk may boil down to the quality of its acquisitions relative to the price it paid, and management's ability to extract long-term value from the asset.

Different strokes

Having made about 50 acquisitions in the last three years, 3D Systems' jack-of-all-trades approach to its market opportunity holds the potential to help it establish itself as a leading 3D printing company for decades to come. However, from an operational perspective, buying, integrating, and maximizing value from multiple acquisitions isn't necessarily a walk in the park. Considering that 3D Systems recently created an executive vice president of mergers and acquisitions role that its former CFO filled, management appears to have also realized this.

Beyond the operational challenges that acquiring many businesses may bring, it's also hard to imagine that 3D Systems hasn't purchased at least one business that won't pan out as management expected and will force the company to take a goodwill impairment charge. However, compared to Stratasys, 3D Systems' risk of goodwill impairment could be significantly lower, considering its goodwill is spread among more acquisitions.

Historically, Stratasys has focused on making a handful of "quality over quantity" acquisitions that either complement or extend its expertise in some way, often targeting well-established leaders in their respective fields. Consequently, Stratasys' balance sheet suggests that its quality-over-quantity approach comes at a premium to 3D Systems' approach, and relies more heavily on the success of the handful of acquisitions it's made in recent years.

3D Systems' more diversified approach to acquisitions, on the other hand, may help it mitigate the magnitude of future impairment charges should an acquisition or two underperform management's expectations.

Where the two intersect

The reality of the situation is that 3D Systems and Stratasys are both at risk of future goodwill impairment charges, but Stratasys is putting significantly more weight behind each of its acquisitions than 3D Systems is. At the same time, 3D Systems may face challenges integrating all of its acquisitions in a manner that realizes their full potential -- which, if unsuccessfully met, may lead to more frequent, but likely smaller, impairment charges.

What it comes down to is that how management executes on a longer-term basis may help determine which company is "riskier" in terms of its goodwill position. Because 3D Systems and Stratasys have both experienced their share of execution issues over the past year, investors should home in on which management team can more effectively iron out the kinks of its operation and focus on driving long-term value for the business and shareholders alike.