For the second quarter in a row, staffing specialist Robert Half International (RHI +4.45%) reported a good set of results -- only for the market to sell off the stock. Guessing how and why the market reacts to earnings reports is a thankless task, and investors are probably better occupied by focusing on what the numbers mean for the developing trends in the business. With that in mind, let's take a look at the tale of Robert Half's second quarter.

Headline numbers

Despite the market's negative reaction -- the stock is down around 6% on the day after results, as I write -- the headline numbers and third-quarter guidance were pretty much in line with company estimates and analyst consensus.

- Second-quarter revenue of $1.272 billion compared against guidance of $1.245 billion to $1.295 billion.

- Second-quarter non-GAAP EPS of $0.67 compared against guidance of $0.63 to $0.68, and analyst estimates of $0.66

And the guidance:

- Third-quarter revenue guidance of $1.295 billion to $1.345 billion compared to analyst estimates of $1.33 billion

- Third-quarter non-GAAP EPS guidance of $0.70 to $0.75 compared to analyst estimates of $0.72

As you can see in the figures above, second-quarter revenue came in slightly ahead of the midpoint of internal guidance, and EPS was toward the high-end of the guidance range. The midpoint of the third-quarter revenue guidance is slightly below analyst expectations, but it's a difference of $10 million in a company expected to generate $1,330 million.

Similarly, the midpoint of third-quarter EPS guidance is slightly above analyst estimates, but not by a significant amount. In short, there's nothing in the headline numbers to panic about.

Permanent versus temporary

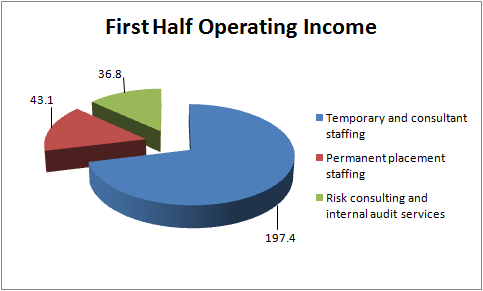

As you can see in the chart below, Robert Half generated more than 71% of its operating income from temporary and consultant staffing in the first six months.

SOURCE: ROBERT HALF INTERNATIONAL PRESENTATIONS. ALL DATA IN MILLIONS OF U.S. DOLLARS.

However, it would be a mistake to assume that following its temporary and consultant staffing operations is the sole objective in analyzing its prospects. On the contrary, the mix of revenue tells you a lot about where the company is headed. For example, in typical business cycles, temporary staffing picks up first in a recovery, only to be followed by growth in permanent hiring as companies start to feel more confident about spending plans.

With this in mind, here is a look at revenue growth rates across temporary and permanent staffing for Robert Half. The chart clearly shows that U.S. Permanent hiring is growing faster than temporary hiring, but it might be expected to be relatively higher at this stage in the business cycle.

Meanwhile, the international figures -- where temporary is currently growing faster than permanent -- reflects the sluggish nature of the recovery in Europe, in particular.

SOURCE: ROBERT HALF INTERNATIONAL PRESENTATIONS.

Moreover, CEO Max Messmer had some positive commentary on growth prospects with U.S. permanent hiring. Speaking on the earnings call, he outlined that the company would be investing in expanding its permanent placement business:

The market continues strong and firm. We have made headcount investments, clearly that's a factor in our growth but as we've talked about a few quarters now in a row, full time demand for staff the labor markets in the US are clearly improving and you see that first and foremost, which typical in our cycle in Perm placement ful-ltime hiring.

Margins

However, Messmer also outlined that margins are likely to be held back initially as the company plans to invest in additional hires in order to chase growth in areas like permanent staffing and technology, in particular.

But we're also going to do it on a pretty broad basis and therefore the operating leverage you might otherwise see we're going to reinvest in headcount because we're bullish as we speak, and therefore on a year-over-year basis you're not going to see a lot of operating leverage at the SG&A line.

In other words, don't expect the increases in revenue to leverage into significantly increased margins.

The takeaway

All told, it was a pretty good quarter for Robert Half International. Provided the economy continues to grow, then you can expect staffing companies to do well. As always with cyclical companies, it's the cycle that matters.

In the case of Robert Half, management continues to be positive, and is investing in order to chase growth. This is an action that will hold back near-term margin expansion; but the company clearly believes that economic growth prospects remain on track.