Image: Jason Industries.

Small companies often go through growing pains, and for Jason Industries (JASN +0.00%), managing a business that involves a number of different areas can be particularly challenging when times get tough. Coming into Friday's third-quarter financial report, Jason Industries had already seen its stock come under pressure, as investors were nervous about the general macroeconomic environment as well as the company's ability to capitalize on its best prospects. Jason Industries' results confirmed some of the fears that investors had, with mixed performance on the top and bottom lines and a less optimistic view of the future. Let's look more closely at what Jason Industries said this quarter and whether it can bounce back from its recent struggles.

Jason Industries sees red

Jason Industries' third-quarter results reflected the difficulties that the company has faced. Revenue rose 6% to $171.2 million, slightly exceeding what most investors had expected to see. Yet on the bottom line, Jason Industries reported an adjusted net loss of $500,000, and that resulted in adjusted per-share loss figures of $0.02, falling short of the $0.01 per share profit that marked the consensus forecast among investors.

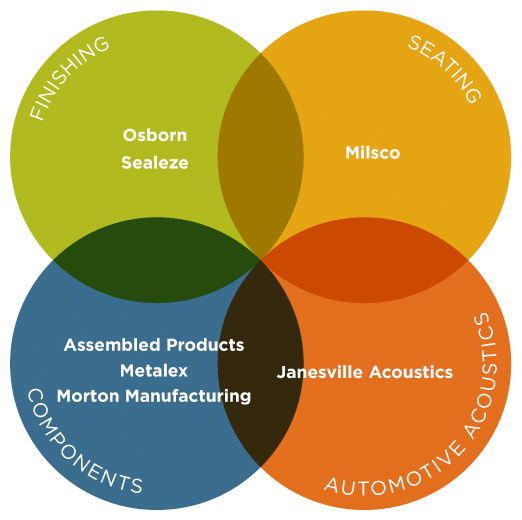

The company's various business divisions had much different performances during the third quarter. In the Finishing segment, revenue jumped 16%, due largely to the acquisition of DRONCO, and adjusted operating income climbed 26% year over year. Yet the company reported softening global industrial demand and delayed customer projects in holding down organic sales growth in the segment. For Acoustics, sales fell 4%, with Jason Industries citing unplanned automotive assembly plant shutdowns during the quarter even though lower raw material prices and improvements in operational efficiency helped lift segment operating profits.

Elsewhere, the Seating segment saw a healthy 15% rise in sales, with a major shift of motorcycle seating products into the third quarter of the year. The company's efforts at developing new business relationships paid off in the Seating area as well, but segment operating income fell on higher costs from boosting capacity and changing product mix. Finally, the Components business saw operating profit soar on a 1% rise in sales, with lower steel prices and a favorable mix of higher margin metals components contributing to the solid performance.

CEO David Westgate emphasized organic sales growth for Jason Industries, even though he tempered his praise by identifying the need to keep improving. "While I am pleased with our gains in the market," Westgate said, "we experienced operational inefficiencies in Seating while trying to efficiently manage production with the growth." Similar comments about Jason Industries' other segments show the company's determination to execute on its opportunities as well as possible.

How can Jason Industries get back into the black?

Unfortunately, Westgate also noted some concerns, especially in the Finishing and Acoustics areas. "While we see areas of strength from gains we are making in the market," Westgate said, "there were signs of slowing end-markets during the quarter. ... We expect ongoing uneven demand in these businesses and we are closely monitoring these end markets."

In response, Jason Industries cut its guidance for the full fiscal year. The company now thinks that revenue will come in between $702 million and $712 million for 2015, down from its previous range of $708 million to $723 million. Similarly, Jason Industries cut its adjusted EBITDA projections by $6 million to $7 million to a new range of $81 million to $84 million.

Jason Industries stock plunged after the announcement, opening down 30% but recovering somewhat from those losses later in the session. Nevertheless, the company's problems don't look likely to go away anytime soon, and Jason Industries will have to fight hard to keep looking for greater profitability through cost-cutting measures and productivity gains well into the future.