The worst oil crash in decades has been taking its toll on the midstream MLP industry, threatening even the potential dividend growth of the industry's blue chips. Yet Sunoco Logistics Partners (NYSE: SXL) continues to rapidly expand both its business and payout. Find out three things Sunoco Logistics investors need to know about the future of its distribution in 2016 and beyond.

Record year to date results

| Metric | Nine-Month 2015 Results | Nine-Month 2014 Results | YoY Change |

|---|---|---|---|

| Gross Profit | $1.027 billion | $905 billion | 14% |

| Adjusted EBITDA | $836 million | $734 million | 14% |

| Distributable cash flow (DCF) | $634 million | $573 million | 11% |

| Quarterly distribution | $1.315 | $1.096 | 20% |

| Distribution coverage ratio (DCR) | 1.20 | 1.57 | (24%) |

Data source: Sunoco Logistics Partners earnings release.

This table clearly shows Sunoco Logistics Partners' business model strength. Despite energy prices declining dramatically in 2015 Sunoco Logistics was able to expand both its gross profits, and its Adjusted EBITDA. For MLPs these two metrics are the most useful for determining operational health.

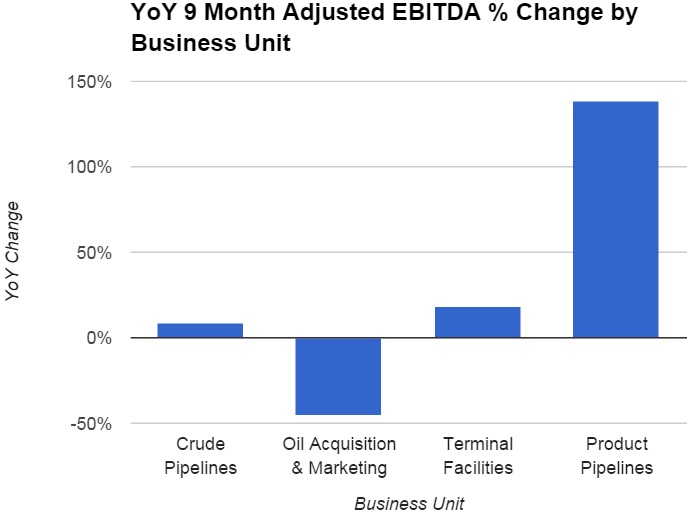

Sunoco Logistics' only commodity sensitive business unit is its oil acquisition and marketing division, which not surprisingly has been hammered by falling oil prices.

Source: Sunoco Logistics Partners Q3 earnings presentation, Author's chart

However, thanks to four large long-term contracted, fixed-fee midstream projects coming online in 2015, the MLP was able to deliver year-to-date fee-based adjusted EBITDA growth of around 40%, allowing for a large increase in DCF.

Superb distribution profile, but don't believe analyst growth estimates

MLP investors need to focus on three aspects of an investment's payout: yield, sustainability, and realistic long-term growth prospects.

Sunoco Logistics Partners' 6.2% yield is more than three times that of the S&P 500, and is backed by a strong coverage ratio that means investors probably don't need to worry about a distribution cut anytime soon. As far as long-term payout growth, analysts expect the next five years to bring 25.5% CAGR distribution growth. A level which I think is outrageously unrealistic.

Sources: Sunoco Logistics Partners investor presentation, earnings release.

It's true that Sunoco Logistics Partners has an impressive track record of very fast distribution growth. However, current low oil prices are causing its oil marketing business to act as a massive drag on adjusted EBITDA. Since DCF equals adjusted EBITDA minus maintenance capital expenditures, this means that as long as crude stays cheap, DCF growth is likely to be much slower than in the past.

Sunoco Logistics Partners' DCR is also likely to decline a bit in Q4 since management is guiding for a 5% quarter over quarter (22% year-over-year) payout increase which is faster than its DCF has been expanding in recent quarters. The MLP hasn't provided any 2016 payout growth guidance but as the DCR declines it's safe to assume that Sunoco Logistics Partners' can't continue sustainably expanding its distribution as quickly as it has in the past.

Future growth plans means some (slower) payout growth still likely

Source: Sunoco Logistics Partners investor presentation.

Sunoco Logistics Partners' exceptional DCF growth has occurred because of 12 major organic growth projects that have come online over the past few years. With a backlog of just eight additional projects through 2017, two of which have yet to be fully contracted for, there are just two ways that the MLP could realistically maintain its hyper-growth payout streak.

The first is rather unlikely: a quick and sustained recovery in oil prices that causes demand for oil pipelines, and its oil marketing profits to soar. The other is heavy drop down support from general partners Energy Transfer Partners (NYSE: ETP), and Energy Transfer Equity (ETE -2.21%).

While Sunoco Logistics may obtain some additional assets as part of Energy Transfer's enormous midstream empire, there are two reasons why I don't think investors should expect too much help in the next few years.

Source: Energy Transfer Equity investor presentation.

The first reason is that Energy Transfer Equity is in the process of completing a $38 billion buyout of Williams Companies, which will probably take up most of its focus in 2016. Though Williams has a $30 billion backlog of growth projects, other Energy Transfer MLPs need those assets a lot more.

After all, Sunoco Logistics Partners' existing project backlog is still likely to result in moderate distribution growth. In addition, its payout is far more sustainable right now than other MLPs in the Energy Transfer family. For example Energy Transfer Partners just reported abysmal quarterly results in which falling energy prices caused DCF per unit to plunge 62% year over year.

Bottom line: Here's what to focus on in 2016

Sunoco Logistics Partners' toll booth business model means that its distribution is likely to remain an attractive, and sustainable long-term income generator for dividend lovers. However, given the realities of the current energy markets investors probably need to expect payout growth to slow in 2016.

Instead next year Sunoco Logistics Partners investors should focus on: whether or not management is able to locate additional projects to grow its backlog, the soundness of its balance sheet so it can fund existing growth initiatives, and that the coverage ratio remains firmly above one.