The headline numbers from Cisco Systems'(CSCO +0.38%) third-quarter results, reported May 18, were good on a superficial basis, but let's take a closer look at the underlying themes and trends in order to better see what's going on. In truth, it's hard to argue that the earnings weren't a net positive, but there are some underlying concerns from the report.

The raw numbers

Starting with the headline numbers:

- Adjusted revenue growth of 3% in the third quarter came in at the high end of guidance for 1% to 4%.

- Non-GAAP EPS of $0.57 was above the guidance range of $0.54 to $0.56.

- Non-GAAP gross margin of 65.2% was significantly ahead of guidance for 62.5% to 63.5%.

- Non-GAAP operating margin of 30% was ahead of guidance for 28.5% to 29.5%.

Clearly, revenue growth was good, but margin growth was even better, leading to EPS ahead of expectations -- a good quarter, especially in the circumstances of a moderate global economy.

The details behind Cisco's third quarter

The best way to think about Cisco's earnings is to look at four separate item: (1) core products (I'm defining these as switching and routing), (2) non-core (collaboration, data center, wireless, security, service provider, and other products), (3) services (which tends to lag product revenue growth), and (4) deferred revenue growth. The fourth is important because Cisco is selling more software on a subscription basis, therefore shifting some upfront revenue toward a stream of revenue that's recognized over time.

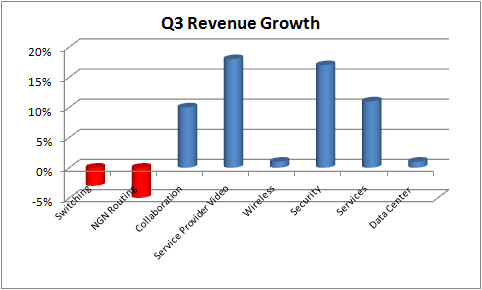

Frankly, switching and routing revenue were disappointing. Switching revenue declined 3%. Going into the fiscal year, Cisco's management expected switching revenue would pass an "inflection point" in the second half thanks to next-generation data center switching offsetting any weakness in historical data center switching.

The good news is that, according CEO Charles Robbins on the earnings call, data center switching is playing out as "we had indicated," but because of an uncertain environment, enterprises are not refreshing their campus networks.

Similarly, NGN routing (Next Generation Network routing) revenue declined 5%, with Robbins saying the following on the earnings call:

Clearly there is a macro issue that we are dealing with. We also saw again as you heard from some of our peers, we saw some increased caution in the service provider space. We saw slow movement in the core of those networks.

So, if it wasn't a good quarter for Cisco's core business, where did the guidance-beating numbers come from?

Cisco's non-core and services to the rescue

Starting with services revenue (up 11%), any way you look at it, Cisco had a good quarter. The headline number is somewhat flattering -- Cisco had an extra week in the quarter -- but as CFO Kelly Kramer explained, when service revenue growth is normalized, growth was still up 4% compared to 3% in the second quarter and 1% in the first -- a nice trend.

However, the real story relates to the strength of non-core revenue growth. As you can see below, revenue growth was particularly strong in non-core activities -- helping offset declines in core revenue growth.

Data source: Cisco Systems, Inc. presentations.

Ultimately, total revenue grew by around $350 million, or 3%, with around 90% of the growth coming from services. For those trying to work out where the remainder came from, it's due to non-core product revenue offsetting core product declines.

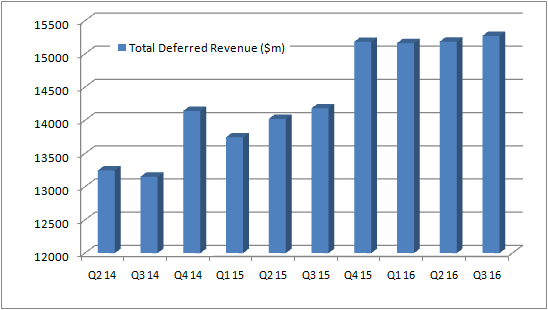

Deferred revenue growth

A look at deferred revenue shows 8% year-over-year growth, but on a sequential basis, it was relatively flat. This is definitely something to look out for in future quarters, because as you can see in the chart below, Cisco will come up against some tougher comparisons from the fourth quarter onward.

Data source: CIsco Systems, Inc. presentations.

Looking ahead

It was a good quarter from Cisco -- it's hard to argue with margins and earnings ahead of expectations -- but investors will want to see a return to growth in its core businesses in future quarters. Similarly, Cisco is coming under pressure to keep growing services revenue, particularly when core product revenue is declining and deferred revenue growth could slow in the coming quarters.