Image source: Getty Images.

To say that Social Security is critical to providing a financial foundation for our nation's retired workforce would be an understatement.

As of the April 2016 snapshot from the Social Security Administration, approximately 60.4 million people were receiving benefits, with two-thirds of those being retired workers. Furthermore, when Gallup questioned seniors about their reliance on the program in Oct. 2015, 59% responded that Social Security benefits were a "major" source of their income, with another 31% chiming in that Social Security income was "minor." Regardless of how we angle the data, some nine in 10 seniors count on Social Security to help meet their expenses during retirement.

Because Social Security plays such an important role in the lives of seniors, how the SSA adjusts its payouts to reflect inflation is an important factor that beneficiaries and pre-retirees closely monitor. The more closely benefits increase with the national rate of inflation, presumably the more likely seniors are to be able to afford their expenses during their golden years. However, as you'll see, the inflation measure the SSA uses may not be working out as planned for senior citizens receiving a Social Security check.

Here's how the SSA calculates cost-of-living adjustments

Let's begin with the basics of how the SSA calculates whether Social Security benefits will rise, and by how much, on a year-to-year basis.

Image source: Pixabay.

The metric used by the SSA is the Consumer Price Index for Urban Wage Workers and Clerical Workers, or CPI-W. The SSA uses the prior years' third-quarter average for the CPI-W as the baseline and then examines how much, to the nearest tenth of a percent, the CPI-W has changed on a year-over-year basis. If the CPI-W has increased, beneficiaries can expect a "raise" during the following year, although you won't find out whether you're getting a higher payment until October. If the CPI-W falls, benefits remain flat on a year-over-year basis. The CPI-W takes into account expenses such as housing, medical costs, transportation, education and communication, apparel, food and beverages, as well as other goods and services.

Last year, the CPI-W fell from an average of 234.24 in the third quarter of 2014 to 233.28 in the third quarter of 2015, largely on account of falling prices at the pump, thus dooming seniors to no cost-of-living adjustment (COLA) in 2016. This marked the third year since 2009 that seniors would receive no COLA. It's tough to tell what could happen in 2017, but we have seen a modest increase in the CPI-W in 2016 from 2015 through the first four months of the year, implying that a "raise" could be due to seniors next year. We'll know more by the time October rolls around.

Seniors are potentially getting hosed by the CPI-W

The way COLA is calculated appears pretty straightforward, but seniors could be getting the short end of the stick despite representing the majority of Social Security beneficiaries. The reason is simple: The CPI-W takes into account the spending habits of the workforce, not retirees. Retirees' expenses are often much different than those of workers, meaning seniors could wind up losing buying power by having their benefits tied to the CPI-W.

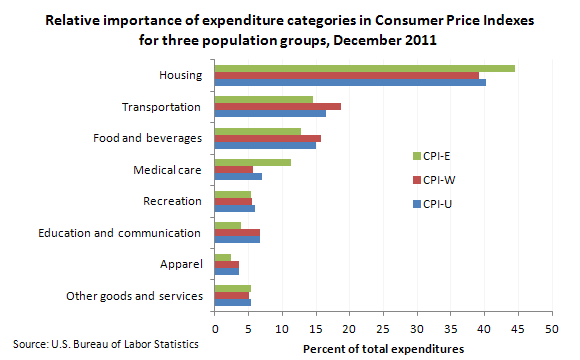

A separate measure created to track inflation is the Consumer Price Index for the Elderly, or CPI-E. Designed to only include Americans ages 62 and up, it examines essentially the same gambit of expenses that the CPI-W does, only it produces markedly different results. As you can see below, this Dec. 2011 Bureau of Labor Statistics snapshot of the CPI-W and CPI-E (along with the CPI-U, a Consumer Price Index for All Urban Consumers) demonstrates the marked differences between the two measures of inflation.

Image source: Bureau of Labor Statistics.

The chart above clearly shows that what workers spend their money on is not necessarily the same for seniors. Some 44.5% of spending for seniors is on housing, with medical care comprising 11.3% of their expenses. This last figure shouldn't come as a shock since the elderly often account for the majority of medical expenditures. Comparatively, only 39.2% of expenses for workers goes toward housing, and less than half (relative to seniors), 5.6%, is spent on medical care. Instead, the CPI-W shows us that workers tend to spend more on transportation, food and beverages, education and communication, and apparel.

What this suggests is that seniors are being underrepresented in terms of COLA when it comes to medical care and housing. This is a potentially serious problem since the rate of medical inflation is far outpacing wage growth and Social Security's COLA, and it could put seniors who rely on Social Security in a pickle come retirement.

The CPI-E isn't flawless, either

According to Alan Grayson (D-Fla.), a representative in Florida's ninth congressional district, seniors have missed out on $388 billion in cumulative COLA increases since 1982, all because the SSA uses the CPI-W, not the CPI-E. However, even the CPI-E has its drawbacks.

Image source: Getty Images.

For example, the CPI-E does indeed focus on the expenses of persons ages 62 and up, and the number of elderly persons in the U.S. is expected to nearly double between 2012 and 2050 to 83.7 million, based on U.S. Census estimates. But the CPI-W takes into account the vastness of the workforce (which included roughly 156 million people in 2014), meaning there are considerably more heads being taken into account. In theory, the CPI-W is a better measure of inflation since it's including a much larger percentage of the population.

Perhaps the bigger problem is that the CPI-E isn't factoring in Medicare Part A expenses, and this is where a good chunk of seniors' costs could be coming from. Part A is the hospital insurance component of Medicare that covers inpatient stays, costly surgeries, and some forms of long-term skilled nursing care. Without these big costs being factored in, even with the CPI-E seniors may not get the COLA they need to cover their rising medical costs.

If the annual COLA debate has demonstrated anything, it's that Americans need to have alternative income channels available to them during their golden years. For you, this means contributing to your company's 401(k) and matching your employer's contribution (if one is offered), opening and maxing out your annual Roth or traditional IRA contribution, and having a withdrawal plan in place before you retire so you can minimize the taxes you'll pay in retirement.

It's really anyone's guess whether the CPI-W vs. CPI-E debate will gather steam, but I don't foresee any changes to the COLA calculation in the near term.