How to make money from corporate bonds

Investing in corporate bonds is generally part of a strategy to protect your capital and earn a profit from the interest paid as part of a diversified portfolio of stocks and bonds. You can also make money by investing in bonds trading at a discount to face value (also called par value).

This can occur for a couple of reasons. One reason is a change in the interest rate environment. If interest rates rise, investors can earn more with new issues, so existing bonds will be discounted to compete with new issues.

A bond may also be discounted if a company is at risk of not meeting its debt obligations or may be forced to issue stock to pay off convertible bonds. In these instances, bondholders are often willing to sell below face value -- how much the bond investments cost at issuance -- to reduce the risk of higher possible losses.

There's certainly more risk with bonds in such situations since these companies could default on their debts, resulting in losses for their bondholders.

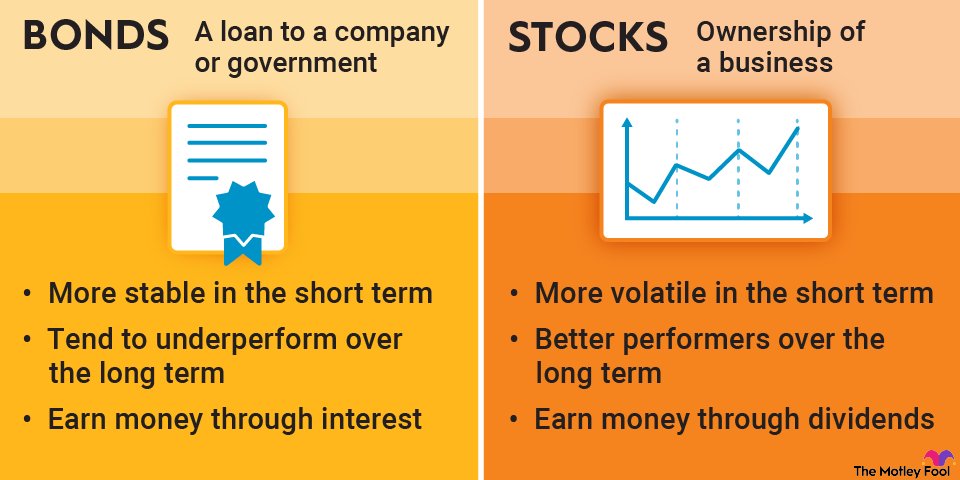

Corporate bonds vs. stocks

Stocks represent direct ownership in a business, while bonds are loans with a predetermined rate of return. This is why, even for a strong and profitable company, the value of its bonds will hold stable even if the stock price changes substantially. You usually know exactly what you're getting with a bond.

A company's stock price, however, can fluctuate substantially and is often based on projections of what people think the company could earn in the future. As a result, stock prices can be volatile, while corporate bonds tend to hold their value. You trade the potential upside of stocks for the predictability of bonds.

Pros and cons of corporate bonds

As noted, the biggest benefit of corporate bonds is stability. Even the best companies' stocks can crash with the market, and this volatility can lead to big losses if you need to sell at a specific time. But bonds tend to hold up across every economic environment as long as the issuing company remains in good shape.

The drawback is that this stability comes at the expense of lower long-term returns. Corporate bonds are ideal stores of value for wealth you'll depend on in the next five years or less. Over longer periods, bonds don't match the wealth-building power of stock ownership.