On Aug. 14, 1935, President Franklin D. Roosevelt signed the Social Security Act into law, intending to provide financial security during the Great Depression. More than four years later, in January 1940, the first monthly Social Security checks were sent out. Since then, the program has grown tremendously to be one of America's largest and most important.

In the 90 years that Social Security has been in place, it has benefited hundreds of millions of retirees. In fact, the program will make over $1.6 trillion in payments to around 72 million beneficiaries, including those receiving retirement benefits, disability benefits, and survivor benefits.

Image source: Getty Images.

A lot has changed with Social Security over the past 90 years. If you're a current recipient, you can attest to how much continues to change -- including eligibility, benefit calculations, and full retirement ages. But arguably the most important change happens annually with the cost-of-living adjustment (COLA).

The annual COLA was put in place in 1972 to help retirees deal with inflation while receiving fixed monthly benefits. The official COLA percentage will be announced on Oct. 15, but retiree advocacy group The Senior Citizens League (TSCL) has routinely put out projections to help retirees plan ahead.

In its latest estimate released this month, TSCL has the upcoming COLA at 2.7%. Although the projection shouldn't be taken as a guarantee, it's worth taking a deeper dive into how the COLA works and what a 2.7% adjustment could mean for retirees.

How the annual COLA is determined

To determine the yearly COLA, the Social Security Administration (SSA) looks at a specific measure of inflation called the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). It's published monthly by the Bureau of Labor Statistics (BLS) and takes into account the price of goods and services like food (groceries and restaurants), transportation (vehicles, gas, and public transportation), housing (rent and utilities), and healthcare (services, prescriptions, and insurance premiums).

The SSA uses a three-step process to come up with the specific percentage to set as the COLA:

- Calculate the CPI-W average for the third quarter (July, August, and September) of the current year.

- Calculate the same average for the previous year.

- Set the percentage increase as the COLA for the upcoming year (rounding it up to the nearest 0.1%).

For example, the third-quarter CPI-W average in 2024 was 308.729, and the average in 2023 was 301.236. That 2.43% increase is how we ended up with the 2.5% COLA for 2025.

If the CPI-W decreases or stays the same, there is no COLA, and benefits remain unchanged. It's not common, but it has happened (in 2010, 2011, and 2016).

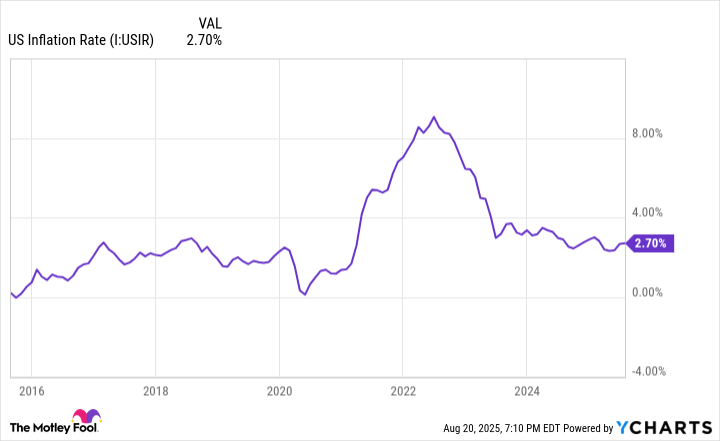

US Inflation Rate data by YCharts.

Complaints about the COLA

A benefits increase sounds like a good thing for Social Security, and for the most part, it is. However, a major (and valid) complaint has been that the COLA isn't typically enough to truly offset the effects of inflation.

According to TSCL, Social Security recipients have lost around 30% of their purchasing power since 2000. This means every $100 in benefits received in 2000 would only buy $70 worth of goods and services today. From 2010 to 2024, TSCL says that Social Security benefits lost 20% of their purchasing power; that's far from ideal.

If TSCL's 2.7% COLA estimate turns out to be true, the average monthly benefit would increase from $2,007 (July's average) to $2,061. A $54 monthly increase is better than no increase, but retirees have likely seen their monthly expenses increase by more than that.

There aren't any concrete plans in place to change how the SSA calculates the annual COLA. In the meantime, it's best for retirees to assume that benefits alone may not fully keep up with inflation, and make efforts to adjust their spending accordingly.