Source: Jordan DiPietro

Social Security touches nearly every American's financial life, with tens of millions of recipients getting benefits and many more being eligible for future benefits in case of disability or when they retire. That makes it worthwhile to learn about every strategy that can potentially give you larger benefits from Social Security.

Yet when people start to take advantage of a smart strategy, lawmakers often clamp down on what they perceive as abuse of the system. That happened with a Social Security strategy that took advantage of the Social Security Administration's formerly generous rules allowing you to withdraw your Social Security application. Although the SSA still allows recipients to withdraw their applications, the much stricter rules covering its use has eliminated the old strategy.

So what should you do instead? Later, we'll discuss alternatives you can use to boost your Social Security. First, though, let's take a closer look at how withdrawing your application could give you the best of both worlds with your Social Security.

The biggest challenge in maximizing Social Security

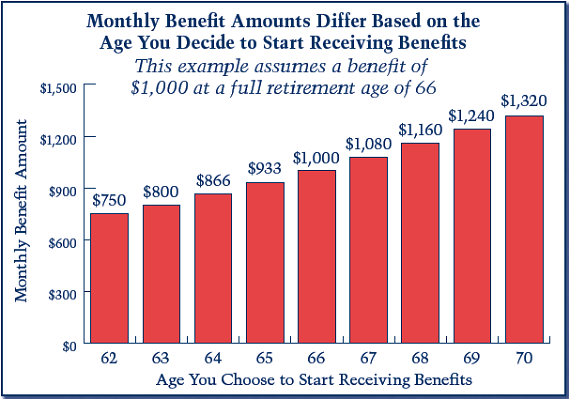

The hardest decision about Social Security for many is when to start taking their benefits. If you start at age 62, you'll maximize the number of payments you'll receive. But those payments will be 25% smaller than if you'd waited until age 66, and 43% smaller than if started at age 70.

Source: SSA

As a result, deciding when to take Social Security involves gambling on how long you and any family members entitled to benefits on your work record will live. Those with shorter-than-average life expectancies have an incentive to claim earlier, while long-lived retirees have a big incentive to wait. Yet obviously, there's a lot of guesswork involved in that decision.

Source: Jorge Barrios via Wikimedia Commons

Turning back the clock on your Social Security decision

What many retirees realized was that it would be nice to be able to go back and change your mind after a few years of retirement. The old rules for withdrawing your application allowed you essentially to do exactly that.

Here's how it worked: All you had to do was file your request with the SSA to undo your original election to take benefits. Then, when you later refiled for benefits, the SSA ignored your initial application and paid an amount calculated to reflect your age at the later date.

The one trade-off was that you had to pay back any benefits you'd already received. For those waiting several years to withdraw their applications, that involved a big chunk of cash. Yet you didn't have to pay interest or penalties on that money, and you were entitled to keep any income you'd earned by investing that money. You could also get compensated if you had had to include any of your Social Security benefits as taxable income and paid income taxes on it.

Source: iamsummersblog.com

Why the SSA killed this budding strategy

At first, this strategy didn't cause many problems because so few people knew about it. But as the strategy gained attention, the SSA identified the potential costs of allowing the situation to continue. Studies by well-known retirement think-tanks like Boston College's Center for Retirement Research noted the "free loan" aspect of the rule, and critics pointed to the potential manipulation that the rule allowed and the cost to the Treasury of giving recipients this much flexibility in taking back their decision on benefits.

In response, the SSA issued new rules that limited application withdrawals to the first 12 months after you initially filed. You could also use the method only once in your lifetime. The SSA argued that 85% to 90% of those who withdrew their applications did so within the first year anyway, but the net effect was to crush the longer-term use of the strategy.

Source: SSA

What you can do instead

Fortunately, there are some other Social Security strategies that many retirees can use to boost their benefits. The file and suspend strategy allows you to file for benefits but then choose not to receive them, allowing a spouse to claim spousal benefits on your work record but still letting your own benefit amount grow. The file as a spouse first strategy, meanwhile, is the mirror-image of file and suspend, letting you claim spousal benefits once you reach retirement age while waiting to take your own larger retirement benefits until they've grow as much as they can.

Many policymakers see these strategies as also having potential for abuse. So far, though, the SSA hasn't clamped down on them, and proposed legislation to limit or eliminate them hasn't made much progress.

It's always unfortunate when a lucrative Social Security strategy disappears. But by staying aware of other promising strategies, you can take advantage of every opportunity you have to get more from Social Security.