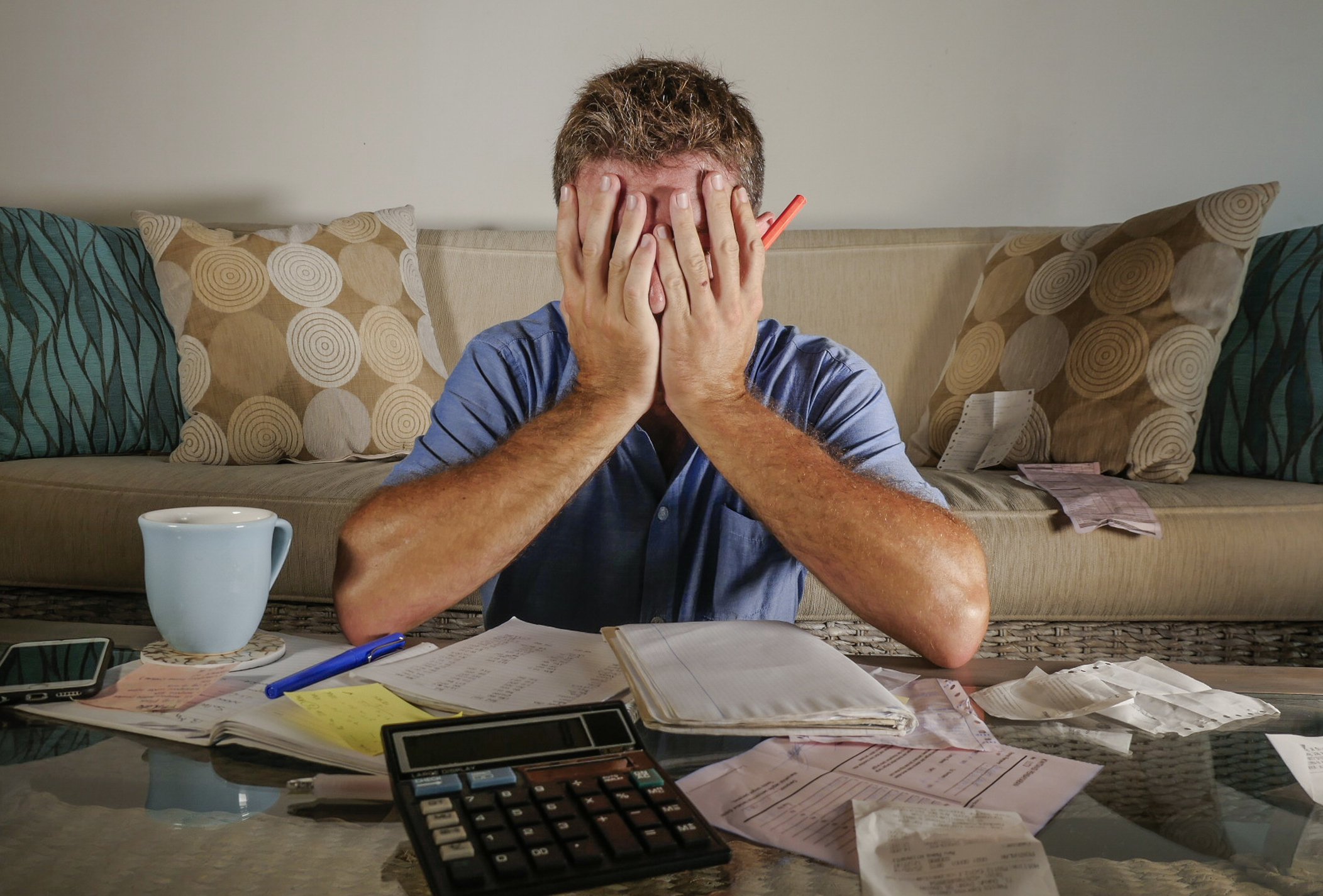

Often, financial habits develop by default, which can end up being very damaging. Unfortunately, you may not even realize you're making the wrong choices with your money just because you've done things a certain way for so long.

To avoid falling into harmful ruts, the start of a new year can be a great time to take stock and see what behavioral patterns are worth changing up. In fact, there are 20 bad money habits you should think about leaving behind for good in 2020.

Our credit card expert uses this card, and it could earn you $1,148 (seriously)

As long as you pay them off each month, credit cards are a no-brainer for savvy Americans. They protect against fraud far better than debit cards, help raise your credit score, and can put hundreds (or thousands!) of dollars in rewards back in your pocket each year.

But with so many cards out there, you need to choose wisely. This top-rated card offers the ability to pay 0% interest on purchases until late 2021, has some of the most generous cash back rewards we’ve ever seen (up to 5%!), and somehow still sports a $0 annual fee.

That’s why our expert – who has reviewed hundreds of cards – signed up for this one personally. Click here to get free access to our expert’s top pick.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.