Necessary in the production of electric vehicles, copper is expected to grow increasingly in demand as auto manufacturers divert their attention from traditional combustion engines. Many investors, consequently, are turning their focus to copper-oriented stocks like Freeport-McMoRan (FCX +0.04%), the world's largest publicly traded copper producer. But it's not solely the production of copper that helps the company to keep the lights on -- it's also involved in the production of gold and molybdenum.

Since the start of 2018, shares of the company are down nearly 10% while the S&P 500 has creeped 2% higher. Despite the stock's poor performance, the Street has remained bullish throughout the year. For example, in May alone, Freeport-McMoRan received two upgrades -- to buy and sector outperform -- from analysts. Does this mean that this miner deserves a place in your portfolio? Let's dig in a little deeper to find out.

Image source: Getty Images.

The bull case

For a mining company, replenishing its depleted assets is critical to its long-term success. Whereas some companies achieve this through acquisitions, others opt to concentrate on projects that they already have in their portfolios. Keenly focused on the future, Freeport-McMoRan, for example, is pursuing organic growth on several fronts. For one, the company is in the midst of expanding operations at Grasberg, one of the world's largest gold and copper deposits, by way of the Block Cave project, which is expected to begin mineral production in the first half of 2019. Looking farther down the line, management anticipates the Lone Star Oxide Development Project, located in Arizona, will begin copper production by the end of 2020.

Image source: Getty Images.

With copper reserves of about 4.4 billion pounds, Lone Star is estimated to have a mine life of 20 years, during which it would have annual copper production of about 200 million pounds.

Pursuing growth projects is undoubtedly important, but it means little if the company jeopardizes its financial health in doing so. For those familiar with Freeport-McMoRan's history, the subject of debt surely arouses unfortunate memories of the company's failed attempt to prosper in the oil and gas industry. Recognizing its misstep, however, management divested the related assets and, subsequently, has excelled at improving the company's financial position. Whereas the company's net debt-to-adjusted-EBITDA ratio was 4.6 at the end of 2015, management has consistently extinguished debt since then, resulting in the company arriving at a ratio of 1.1 at the end of Q1 2018. So successful was the deleveraging that management elected to reinstate the cash dividend, which had been suspended since 2015.

The bear case

One significant area of concern for Freeport-McMoRan is the state of the Grasberg mine, the subject of an ongoing dispute between the company, Rio Tinto, and the Indonesian government, which seeks 51% ownership of the asset. Recently, some progress appeared to have been made toward resolving the dispute, as Rio Tinto announced that it would be willing to sell its stake in the mine to the Indonesian government. However, no agreement has been finalized.

Grasberg plays a dominant role in Freeport-McMoRan's operations. According to management's estimates, for example, Grasberg will account for 30% of the company's copper sales and 100% of gold sales in 2018. In addition to the uncertainty regarding the resolution of the ongoing dispute, there's no guarantee that the Indonesian government won't require the company -- as it did last year -- to pay higher export duties and royalties, thus compromising Freeport-McMoRan's margin on mineral sales from the mine.

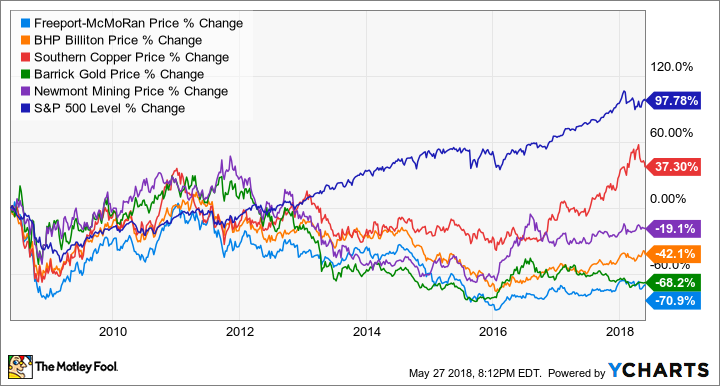

Besides the risks associated with Grasberg, shareholders must be cognizant of the general underperformance of mining stocks compared to the market writ large.

Over the past 10 years, the S&P 500 has not only outperformed copper-oriented stocks like Freeport-McMoRan, and Southern Copper, but it has also outperformed gold stocks like Barrick Gold and Newmont Mining.

Peeking at the price tag

There appear to be valid arguments for both buying and avoiding shares of Freeport-McMoRan, so let's turn to the stock's valuation. Trading at 1.39 times sales, the stock may seem expensive compared to its five-year average price-to-sales ratio of 1.22, according to Morningstar. The stock, however, seems more attractive in terms of cash flow. Whereas its five-year average price-to-cash-from-operations ratio is 4.87, it currently trades at 4.73 times cash flow.

Considering Freeport-McMoRan in terms of sales and cash flow, it appears that the market is fairly valuing the stock -- definitely no bargain opportunity here.

Penny for some thoughts...

In light of the prominent role that copper will play as the auto industry turns toward electric vehicles, Freeport-McMoRan certainly warrants close consideration. Though the company has one of the world's largest deposits of copper and gold in its portfolio, in addition to several compelling projects on the horizon, and management has done yeoman's service in reducing the company's reliance on leverage, the risks associated with an investment seem to outweigh the potential rewards.

Moreover, since the performance of mining stocks is so often inferior to the market, it seems like investors would be better served investing in a simple S&P 500 index fund than taking a chance on Freeport-McMoRan.