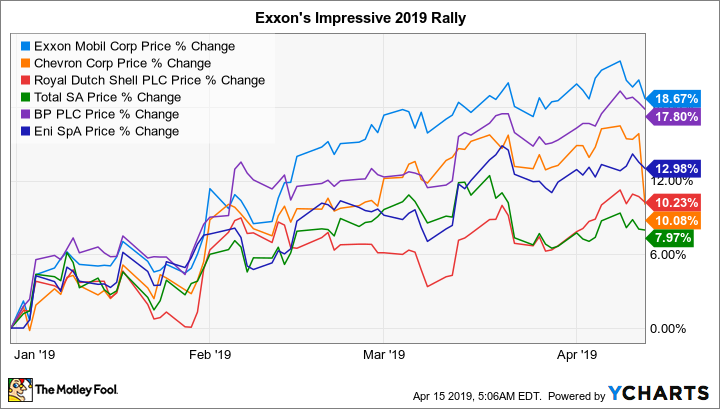

The shares of international energy giant ExxonMobil (XOM +0.94%) are up around 18% so far in 2019. That's better than any of its major peers. Investors have clearly started to see something in the integrated oil and natural gas company's performance that they like. But, after such a nice run, have you missed out on the opportunity at Exxon? The quick answer is no, but here's the deep dive on why ExxonMobil is still a buy.

It's still cheap

Despite Exxon's big price run so far in 2019, it is still trading near a 30-year low when it comes to price to tangible book value. But the roughly 4% yield, while down from recent levels, is still higher than it's been since the mid-1990s. Investors are clearly reconsidering Exxon today, placing a higher value on its shares. However, the stock remains cheap relative to its history.

Image source: Getty Images

Exxon's price to tangible book value is at the top end of its peer group. Historically, though, it's been afforded a notable premium to the peer group. Part of that comes from the boring consistency of Exxon's business and its tendency to deliver better returns on capital. For example, it has increased its dividend every year for 36 consecutive years -- a feat unmatched by its major peers.

It also has one of the strongest balance sheets in the industry. Long-term debt makes up just 9% of the company's capital structure. That gives Exxon a lot of room to add debt during tough oil markets to fund its capital spending plans and support the dividend. Some of the oil giant's peers prefer to use higher levels of debt offset by higher levels of cash. And while they are, overall, equally as strong financially, that model led many peers to halt dividend increases following the deep oil price decline that started in mid-2014. Exxon's approach is more conservative and, if history is a guide, more robust to the ups and downs of the often volatile oil market.

What's going on today

There are some pretty good reasons to be fond of Exxon in terms of valuation and business approach. But what's changed this year that has led to such an impressive rally? The answer is that Exxon appears to be turning an important corner operationally.

Exxon's stock remains cheap because it was hit hard by falling production levels in recent years and by a drop in its return on capital employed (ROCE) metric, a measure of how well the company uses its shareholders' cash. Both numbers are starting to move higher again.

For example, its ROCE fell sharply along with its peers following the oil price collapse in mid-2014. Historically toward the high end of the peer group, Exxon has dropped to just the middle of the pack. However, it has been investing in new assets that it expects to provide industry-leading returns, and it has been divesting older assets that have lower returns. The company isn't simply looking to move its best projects forward, it's actively looking to have the best projects in the industry. The company's return on capital employed numbers are moving up off the lows, but the goal is to get them up to the mid-teens level. That should move the metric back toward the head of the industry again.

XOM Return on Capital Employed (TTM) data by YCharts

Production is a bit trickier. The company's oil production fell 1% in 2016 year over year, and 1.6% year over year in 2017. Production declined again last year, this time by 2.5% year over year. That's the wrong direction, and it looks like the declines are getting progressively worse. There are two important facts here. First, Exxon isn't interested in growing production for the sake of growing production. It only wants to focus on the most profitable production (the industry-leading investments, noted above). Second, there was a notable shift in the trend in the back half of 2018.

Production increased 3.8% between the second and third quarters. And then it increased by 5.9% between the third and fourth quarters. This improvement was on the strength of the company's rapidly expanding U.S. onshore drilling effort. But that's just one of several major projects that Exxon has in the works. It also has big offshore drilling and natural gas plans on which it continues to move forward. U.S. onshore drilling is easier to ramp up, so its other projects may take a couple of years to really start adding to production. But they are on the way and, based on the company's rock-solid balance sheet, there's no reason to expect that Exxon can't deliver on its plans.

These are the improvements that investors are starting to recognize and reward with an improving stock price. They help to explain why Exxon's stock has been outperforming its peers so far in 2019. But don't forget the still-low historical valuation at Exxon. Yes, its stock is up -- but it hardly looks expensive.

Act now or you could miss it

Exxon is certainly not as good a deal as it was at the end of 2018. But if you take a longer-term perspective, the oil giant remains a good value relative to its historical valuation and yield levels. As it continues to execute on its turnaround effort, investors are likely to continue to reward the stock for management's success along the path to improved results. If you act now, you can still jump aboard this recovering and conservatively run energy giant.