Investors using the Robinhood platform generally love strong near-term gains. So many of their favorite stocks are those that have delivered in a period of days or weeks. But that doesn't mean the most popular stocks on Robinhood are short-term winners only. In fact, several of these stocks actually make better long-term investments. Over a longer time period, investors truly can benefit from the companies' innovations, sales, and profits.

Right now, I'm thinking about three particular stocks that have performed well in recent times. But I'm expecting each of them to deliver more to investors over a period of years. Why? They are growing -- and a lot more is on the horizon. Buying them today may result in a big investment win down the road.

Image source: Getty Images.

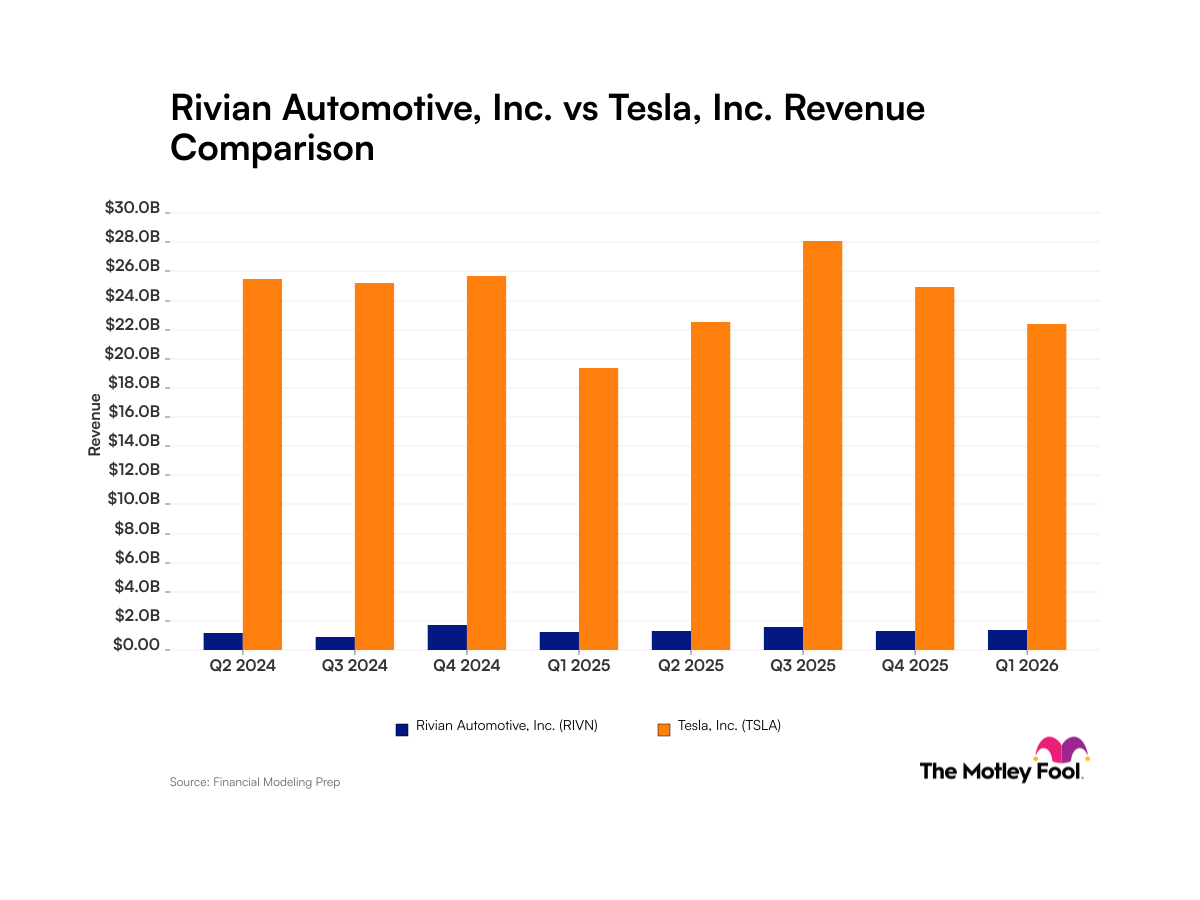

1. Tesla

Tesla (TSLA 3.23%) shares soared 743% last year. This year, gains are modest with only a 10% increase. But that's OK. Catalysts are on the horizon for this leader in the electric vehicle (EV) market. And those catalysts are vehicle deliveries and financial results.

Tesla's off to a good start. The automaker delivered a half a million vehicles last year. This year, deliveries have increased from quarter to quarter. And Tesla has already surpassed last year's total. The company has delivered more than 626,000 vehicles in the first three quarters. Tesla recently reported third-quarter deliveries ahead of the full earnings report.

In the second quarter, the EV giant reported more than $1 billion in GAAP net income for the first time ever. Importantly, the company widened operating margin to 11% from 5.4% in the year-earlier period.

All this in the context of a global chip shortage. CEO Elon Musk calls chip supply "the governing factor on our output." This problem could weigh on Tesla's production schedule. But I see it as a temporary headwind. Demand for Tesla's cars remains strong even as other automakers have joined the EV market. For example, Tesla says European demand is "well above" supply.

Tesla's profit and revenue growth is just getting started.

TSLA Net Income (Annual) data by YCharts

So, I think the share price story is in its early days too.

2. Amazon

I like Amazon (AMZN +0.86%) because it's a leader in two major (and growing) areas: e-commerce and cloud computing.

Let's start with e-commerce. The company's Prime subscription service offers free same-day or one-day delivery on millions of items. And Amazon will deliver groceries for free in two hours in some locations. Amazon continually innovates to streamline the shopping experience. The latest? Now you can order a gift for someone even if you don't have the person's mailing address. Amazon will contact the recipient by email or text message to arrange delivery.

The global e-commerce market is forecast to grow at a nearly 15% compound annual growth rate through 2027, according to Grand View Research. And a giant such as Amazon is likely to benefit.

Now, let's talk about Amazon Web Services (AWS), the company's cloud computing business. AWS was growing before the pandemic -- but the health crisis gave it an additional lift. Many companies realized they no longer wanted to manage their own infrastructure, Amazon said.

AWS contributed more than $4.2 billion in operating income in the most recent quarter -- that's more than half of Amazon's total operating income. Amazon's net income and revenue have been climbing for the past few years. I expect growth in online shopping and AWS to keep that trend going.

AMZN Net Income (Annual) data by YCharts

3. Moderna

Coronavirus vaccine leader Moderna (MRNA 1.85%) soared 268% in the first nine months of the year. But the shares have dropped 21% since the start of October on concern potential COVID-19 treatments will hurt vaccine sales. I see this as a buying opportunity.

First, I don't expect vaccine sales to drop off a cliff. Treatments and treatment candidates so far haven't been 100% efficacious. And that means it's still possible to fall severely ill -- and end up hospitalized. About 55% of Americans got a flu shot last season. So, I would expect at least the same population to continue with coronavirus vaccines as well.

Second, Moderna is working on booster candidates to target specific COVID-19 variants, a next-generation vaccine candidate, and a potential combined flu/coronavirus vaccine. These eventual products may generate significant revenue in the future. Experts predict the coronavirus won't disappear when the pandemic is over. It still will be around. And we'll need protection.

And third, Moderna may depend entirely on COVID-19 vaccine sales now. But that won't be the situation forever. The company has 37 programs in the pipeline. And the most advanced is set to enter phase 3 trials this year. It's a vaccine candidate against a common virus called cytomegalovirus (CMV). Moderna predicts between $2 billion and $5 billion in peak annual sales of this potential product.

Moderna shares may be suffering right now. But that, too, won't last forever. The coronavirus program and the rest of the pipeline offer plenty of catalysts to spur gains over time.