Snowflake (SNOW +1.36%) stock has been on a terrific run in the past three months, gaining a remarkable 47% in such a short period of time owing to the broader recovery in tech stocks, which were under pressure amid tariff and other geopolitical concerns.

Importantly, Snowflake's recent rally is quite deserving since the company's growth profile has been improving thanks to its artificial intelligence (AI)-focused data cloud tools. Customers have traditionally used Snowflake's data cloud to securely store and consolidate data into a single platform, and then use that data for generating analytical insights or building applications.

AI has opened up a new growth opportunity for Snowflake. The AI-specific business model that Snowflake has adopted could help it clock outstanding growth in the long run.

Image source: Getty Images.

Snowflake's AI products are giving it a two-pronged boost

Snowflake's push into AI began last year, when the company unveiled its Cortex platform that gave customers access to popular large language models (LLMs) so that they can build and deploy custom applications. Since then, the company has been aggressively adding new AI tools and features to help customers build AI agents and conversational assistants, and access both data with natural language prompts.

NYSE: SNOW

Key Data Points

It is worth noting that Snowflake already had a solid customer base before it started rolling out AI tools. It had just under 9,500 customers at the end of fiscal 2024 (ended Jan. 31, 2024). The company, therefore, had a large number of customers to whom it could cross-sell its AI solutions. The good part is that Snowflake seems to be succeeding on that front.

This is evident from the 124% net revenue retention rate that the company reported in the first quarter of fiscal 2026 (ended April 30, 2025). Snowflake calculates this metric by dividing its product revenue from customers at the end of a quarter by the product revenue from that same customer cohort in the year-ago period. So, a reading of more than 100% is an indication that its existing customers are using more services from the company or have extended the usage of their current offerings.

Apart from the cross-selling opportunity, Snowflake's AI products are allowing it to bring more customers into its fold. This is evident from the 19% year-over-year growth in Snowflake's customer base in the previous quarter to almost 11,600. The company says 5,200 of its customers are using its AI and machine learning (ML) solutions.

As Snowflake continues to launch more AI features through its product development moves or by way of acquisitions, it should be able to convert a bigger chunk of its $342 billion projected end-market opportunity by 2028 into revenue. Moreover, the company's ability to win more business from existing customers should lead to an improvement in its earnings power.

The company's growth is likely to accelerate

Snowflake's product revenue in the previous quarter was up by 26% year over year. However, its remaining performance obligations (RPO) increased at a much faster pace of 34% to $6.7 billion.

RPO is the total value of a company's unfulfilled contracts at the end of a quarter, and the faster growth in this metric as compared to the actual top-line growth means that Snowflake is getting more contracts than it is fulfilling.

As a result, don't be surprised to see an acceleration in the company's revenue growth going forward, and that should translate into an uptick in its bottom-line growth.

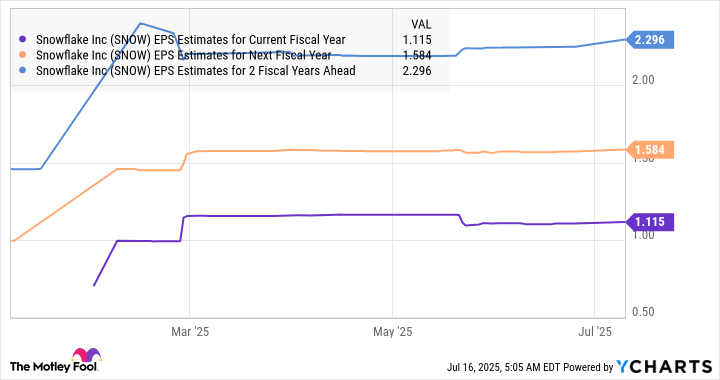

SNOW EPS Estimates for Current Fiscal Year data by YCharts

It won't be surprising to see Snowflake stock being rewarded with more upside on the market because of its improved earnings power, which is why growth-oriented investors can still consider buying it. Its massive addressable market could pave the way for years of terrific growth.