Earnings season is upon us! Last week, Taiwan Semiconductor Manufacturing (TSM 1.24%) reported financial and operating results for the second quarter of 2024. Let's explore the Q2 report from TSMC (as the company is known for short).

From there, I'll dive into some broader industry trends to help explain why the company's latest quarterly result was so impressive, and more importantly, how it is set up for even further growth in the long run.

TSMC just posted a monster quarter all around, and...

TSMC is a major supplier for leading chip companies such as Nvidia, Advanced Micro Devices, and Broadcom. Moreover, the company's reach extends beyond traditional semiconductor businesses since it has also forged strong relationships with tech giants Apple and Amazon.

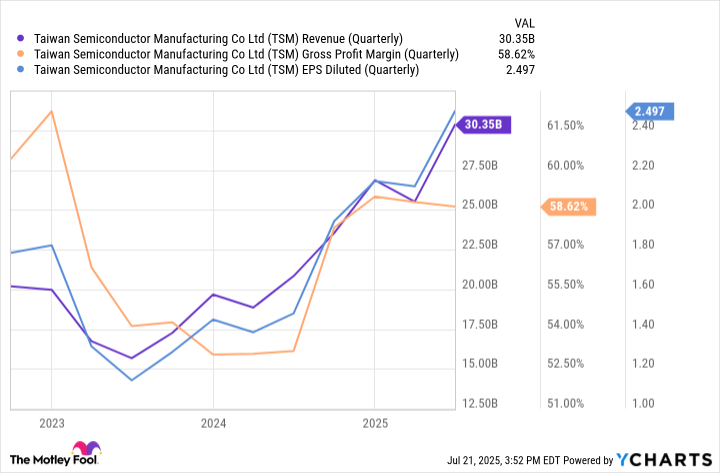

During the second quarter, the company generated more than $30 billion in sales, thanks in large part to continued robust demand for the company's 5nm and 3nm chip nodes.

TSM Revenue (Quarterly) data by YCharts; EPS = earnings per share.

While the company's revenue grew 44% year over year, steadily improving gross margins and a disciplined cost structure fueled even more acceleration for its bottom line. During the second quarter, earnings per share (EPS) were roughly $2.50 -- representing nearly 61% growth year over year.

Image source: Getty Images.

... forecasts suggest much more growth is in store

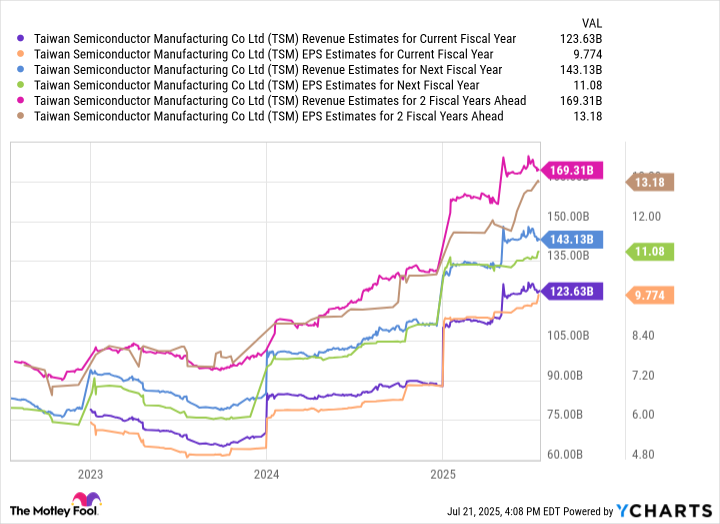

In 2025 alone, cloud hyperscalers Microsoft, Alphabet, and Amazon, in combination with social media empire Meta Platforms, are expected to collectively have up to $330 billion in capital expenditures (capex). Taking this one step further, management consulting firm McKinsey & Company forecasts that investments in AI infrastructure -- which include data center buildouts and chips -- are expected to reach $6.7 trillion by next decade.

With TSMC producing more than 40% revenue growth with an estimated 60% of the global chip foundry market, it appears well-positioned to capitalize on these secular tailwinds and acquire even more market share over the next several years.

TSM Revenue Estimates for Current Fiscal Year; data by YCharts.

What does TSMC's earnings report tell us about AI demand?

To me, the simplest explanation of the blowout earnings report is that AI demand is not only strong, but it's also accelerating. While growth will fluctuate from quarter to quarter, I don't really see TSMC as a cyclical semiconductor stock at this point.

Rather, the capex and infrastructure trends referenced above underscore how crucial AI growth is to the global economy at this point. The chipmaker's leading foundry services across edge devices, high-performance computing (HPC), and AI accelerators are at the center of this secular evolution.

Is Taiwan Semiconductor stock a buy right now?

Despite the company's jaw-dropping growth and robust outlook, TSMC trades at a forward price-to-earnings multiple (P/E) of just 24. Not only is this much lower than historical levels, but it is also a meaningful discount to many other leading chip stocks, too.

While skeptics may cite the cyclicality of the chip market or potential geopolitical tensions with China as part of the bear narrative, I think TSMC's current financial profile and its future trajectory speak for themselves regardless of these risks.

NYSE: TSM

Key Data Points

In my eyes, the disconnect between the company's valuation and its underlying business fundamentals could suggest that investors may not fully understand or appreciate the importance of its role in the broader chip ecosystem.

I see TSMC stock as a no-brainer right now, and I think the company's price action suggests it is undervalued. Investors with a long-run time horizon might want to consider scooping up shares and holding on tight as the infrastructure chapter of the AI story continues to be written. Taiwan Semiconductor Manufacturing is uniquely positioned to ride these tailwinds and sustain high levels of revenue and profit growth for years to come.